Italy's Outlook Darkens as Politics Skews From Orthodox Thinking

Italy's Outlook Darkens as Politics Skews From Orthodox Thinking

(Bloomberg) -- Dark clouds are looming on Italy’s horizon as the populist government’s budget deficit appears to be on a collision course with the European Union. Increased friction from both sides raises the risk of contagion which has been largely contained to Italian assets.

Markets are trading on fiscal and ratings concerns rather than redenomination fears, and tentative signs of compromise by Italy’s government regarding the trajectory for its deficit path reduces the risk of escalation. That comes as the coalition attempts to square the circle with underlying growth assumptions.

Medium-term debt sustainability concerns with risks of a hefty increase of the debt-to-GDP ratio leaves a slant to using any relief in Italian bond markets to reduce exposure and maintain positive convex hedges.

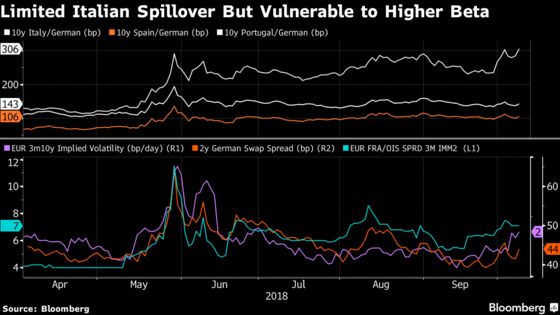

- The limited response of German 2-year swap spreads, a popular hedge against Italian risks, to the 10-year BTP/Bund spread widening to >300bps highlights the low sensitivities of European assets and current idiosyncratic nature of Italy’s issues

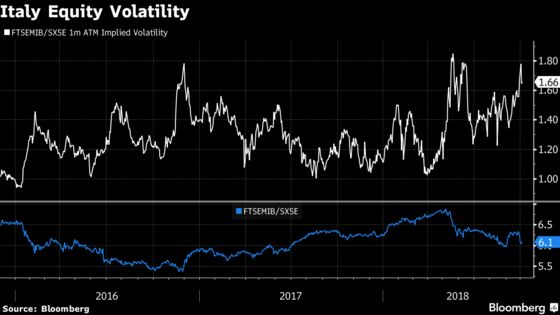

- European equity volatility barely reacted to BTP sell-off outside FTSEMIB, with SX5E ATM 3-month implied vol at 15th-percentile of 10-year range, volatility skew has barely moved and FTSEMIB/SX5E 1-month ATM vol ratio close to record highs

- Another popular hedge against Italian risk is the relative value between high and low coupon BTPs, where high-coupon bonds that trade above par sharply underperform as markets price higher default probabilities (as investors stand to lose more on those higher priced bonds)

- Long low-coupon vs high-coupon BTPs performance has been less pronounced during recent spread widening compared with the pronounced sell-off in May driven by heightened redenomination fears

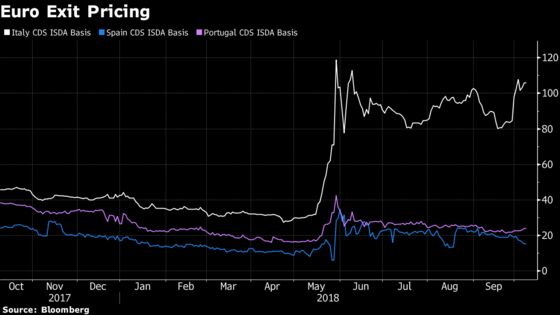

- Sovereign CDS, a much smaller and less liquid market, implies ~7% probability of currency redenomination in the next 5 years, based on the spread between 2014-2003 contracts; while that is close to highs seen in May, this time there is limited spillover in Spain and Portugal equivalents, suggesting low systemic risk

- Price difference between the two CDS contracts shows the extra premium investors are willing to pay against redenomination as the 2014 version offers additional protection against defaulted bonds being converted into a different currency

- NOTE: Tanvir Sandhu is a global interest-rate and derivatives strategist who writes for Bloomberg. The observations he makes are his own and are not intended as investment advice

To contact the reporter on this story: Tanvir Sandhu in London at tsandhu17@bloomberg.net

To contact the editors responsible for this story: Ven Ram at vram1@bloomberg.net, Keith Jenkins

©2018 Bloomberg L.P.