Italy’s Age-Old Problems No Longer Scare Bond Investors

Italy’s Age-Old Problems No Longer Scare European Bond Investors

(Bloomberg) -- Even as Italy heads for a period of volatile politics, budget disputes and possible credit downgrades, investors are sticking with the nation’s debt.

That’s because the fiscal and monetary firepower of the European Union and European Central Bank is shielding Italy’s bond market from the uncertainty ahead, according to BlueBay Asset Management LLP, AllianceBernstein and Axa Investment Managers.

“Our confidence in the country is growing,” said Alessandro Tentori, chief investment officer at Axa. He’s looking to increase his exposure to Italian bonds, even if Matteo Salvini’s anti-migrant League Party wins the Sept. 20-21 regional elections in the left-wing bastion of Tuscany, threatening the stability of the government in Rome.

“It would mark an epic moment, but I think it would be more an opportunity to add risk at better price,” Tentori said.

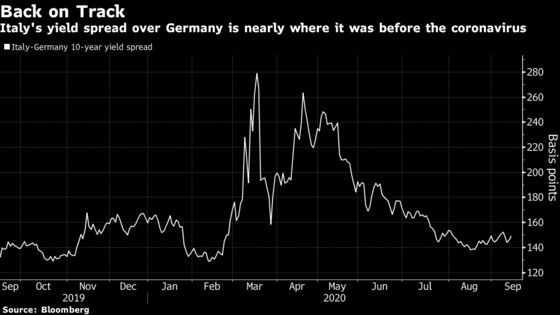

Italian bonds have rallied since the ECB turbocharged its quantitative easing policy with a pandemic bond buying program. The yield on the nation’s benchmark debt on Monday was roughly a third of its peak level in March, when concern over the economic fallout of a nationwide lockdown was at its height. Sovereign 10-year bonds were little changed on Tuesday, their yield at 1.03%.

The EU’s 750-billion-euro ($890 billion) rescue fund added fuel to that rally, with observers seeing the deal as a step toward fiscal unity.

Investors in Italy have had to weather several political upheavals in recent years, including flare-ups of euroskeptic sentiment. One of the nation’s newest political parties wants to pull it out of the EU and ditch the euro as part of a bid for greater sovereignty.

The country was among the hardest hit by the last decade’s sovereign debt crisis, and has seen tepid growth for much of the past 20 years. Even before the pandemic, the economy had one of the highest debt levels on the continent and in February, the European Commission warned that risks to Italy’s ability to refinance its debt in the medium to long term were “high”.

“The recovery fund is maybe the last chance for the country to close the gap with the rest of Europe and to relaunch the Italian economy,” former Italian Prime Minister Enrico Letta said in an interview last month. “We never had such a dimension of investment in the country in the last 40 years maybe.”

The Risks

Letta, who headed a three-party tie-up in 2013-2014, warned that political instability resulting from the regional elections could coincide with a flare-up in Covid cases, strengthening the far-right’s hopes for power.

Alongside these challenges are a growing debt-load and rating reviews by Moody’s Investor Service and S&P Global Ratings, the former ranking Italy just a notch above junk status.

And the country must draft its budget against a predicted economic slump exceeding 10% this year. Two years ago, a drawn-out dispute with the European Union over fiscal plans sent borrowing costs spiraling to levels unseen since the sovereign debt crisis.

| Read More: |

|---|

|

Still Bullish

Investors are staying the course with Italian bonds. While BlueBay Asset Management has cut its holdings, it still has an overweight position. AllianceBernstein money manager John Taylor is willing to “look through that higher debt-to-GDP level” over the next six to 12 months to increase holdings in Italian debt.

That bullishness is reflected in the nation’s 10-year yield spread over Germany, a key gauge for risk in the country, which has narrowed to around 150 basis points. The gap has more than halved since hitting a peak in March this year, during the height of the coronavirus crisis.

“The ECB is buying more bonds than Italy is issuing and this supportive technical should ensure spreads remain contained,” said Mark Dowding, BlueBay’s chief investment officer. “In this context we remain overweight.”

©2020 Bloomberg L.P.