Europe Agrees on $260 Billion Credit Lines to Stem Fallout

Italy May Be Offered Cheap Cash. Question Is if It Will Take It

(Bloomberg) -- Euro-area finance ministers agreed to allow the region’s bailout fund to extend credit lines to each of the bloc’s governments on concessionary terms, paving the way for countries including Italy to draw cheap liquidity amid an unprecedented spending spree.

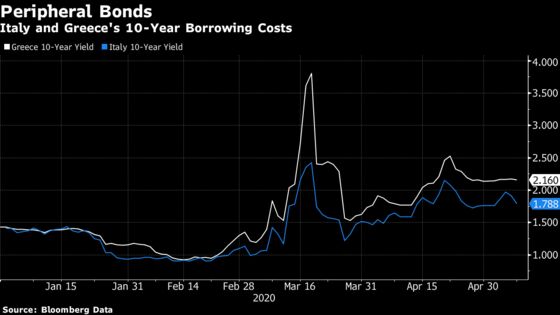

The deal struck at a video conference on Friday forms a key part of the bloc’s response to the crisis brought on by the coronavirus pandemic, that’s put the European Union on track for the steepest recession in its history. Italian bonds rallied, with yields on 10-year notes dropping 8 basis points to 1.84%.

Under the emergency support instrument, euro-area governments will have access to cheap funds worth up to 2% of their 2019 output, without any of the onerous belt-tightening terms that were attached to the loans granted during the sovereign debt crisis. The European Stability Mechanism will be able to lend to countries on terms normally reserved for sovereigns with a pristine credit rating, and with few questions asked.

For Italy, this means it could receive 36 billion euros in ultra cheap loans -- a sum that could conceivably increase should there be a major need.

Backed by Germany’s creditworthiness, the ESM borrows money at negative yields, which it then lends to euro-area member states after charging small service fees. In current terms, the interest rate on such loans could be around 0.1%, ESM Managing Director Klaus Regling said.

With borrowing costs in the euro-area periphery creeping up over the past few months amid a virus-induced economic slump, cash-strapped governments could benefit from billions in much-needed interest savings for the outlays needed to cushion the blow.

Under the ministers’ agreement, the loans countries would be able to receive would have a maximum average maturity of 10 years. Requests can be made until the end of 2022, and the initial availability period for each credit facility will be 12 months, which could be extended twice for 6 months.

The program, which still needs to by signed off by several national parliaments, could be in place by May 15, but toxic politics could squander the potential 240 billion-euro ($260 billion) bonanza.

In Italy, Prime Minister Giuseppe Conte, under pressure from populists both within and outside his fractious coalition, had initially ruled out using the credit lines, given the stigma of the painful bailouts of the last decade. Spain and Greece’s governments have also said they don’t plan to tap them, even though the borrowing costs for Europe’s most indebted state are much higher than the concessional terms it would secure from the ESM.

In an effort to appease the South, the European Commission proposed on Thursday to essentially eliminate all the usual conditions that would come with the loans, such as regular visits by auditors to check up on the beneficiary state’s finances. Italian newspapers played up the lack of strings Friday, with Corriere della Sera running a front-page headline saying: “Europe commits: ESM funds on health without conditions.”

“ESM without conditions for those who ask for it, Brussels paves the way for Italy,” echoed La Repubblica. Conte himself softened his stand on the issue last month. “We are ready to work on this new credit line, so that no conditionalities are introduced,” Conte told senators on April 21.

Recovery Fund

The ESM’s pandemic credit line is part of the EU’s response plan to the deadly pandemic ravaging its economy. The commission is also working on a proposal for a recovery fund jointly financed by the bloc’s member states.

The plan, which will aim to mobilize some 2-trillion euros in investment and financing, according to a draft seen by Bloomberg last month, is even more contentious, with member states arguing about its size as well as on whether the financing to countries hit the most will come in the form of loans or grants.

A bloc of Southern member states led by France demands that the recovery instrument is financed by joint debt issuance and its cash is handed to member states that need it the most in the form of grants. “Otherwise, it would only replicate the logic of already existing instruments,” the French government said in a memo to other member states, referring to the ESM credit lines.

According to the French memo, seen by Bloomberg, the recovery fund must have a size of 150 to 300 billion euros each year between 2021 and 2023. Its resources will come from jointly backed debt, which will be repaid from the EU’s existing joint budget over a period spreading through 2060.

Germany, the Netherlands, Austria and other Northern member states have already rejected the prospect of joint debt issuance, putting the commission in the unenviable position of having to come up with a recovery fund proposal that bridges diametrically opposed positions. The EU executive was originally expected to unveil its proposal on May 6, but this not expected now until the third week of May at the very earliest.

For now, the credit lines are the only solid tool of common financing that may become immediately available to battered economies. “Rejecting this new credit line means doing a disservice to these countries which flank us in the battle,” Conte said last month.

©2020 Bloomberg L.P.