Italy's Bond Market Grows Worried Over Salvini's Leadership Bid

Italy's Bond Market Grows Worried Over Salvini's Leadership Bid

(Bloomberg) -- The bond market used to like the idea of Matteo Salvini as Italy’s leader. Now it’s becoming worried.

As League party leader Salvini attempts to force fresh elections, investors fear victory would embolden a new government to ramp up spending and clash with the European Union again over budget deficit limits. With the nation’s bonds having seen the biggest one-week selloff since the current coalition was formed in May last year, more turmoil is expected and could lead its borrowing costs to return to levels that could rattle global markets.

With the League topping opinion polls, Salvini has pledged that a government led by him would cut income tax for most Italians, start a large program of public works, and stop the introduction of an automatic VAT increase in 2020. The political risk comes at a time when the economy has almost ground to a halt, suggesting that Italy’s debt burden will continue to rise.

“It’s going to be a hot Italian summer for bond markets,” said Andrea Iannelli, a London-based investment director at Fidelity International, which has an underweight position in Italian bonds. “The plan that the League has is not strictly conservative from a fiscal point of view.”

Italian lawmakers have summoned Prime Minister Giuseppe Conte to appear before the senate on Aug. 20, from which Salvini is pushing for a quick confidence vote that would lead to a snap ballot. The way forward will ultimately be decided by President Sergio Mattarella, who can seek to form an alternate ruling coalition in parliament, or call a general election.

Read More:

|

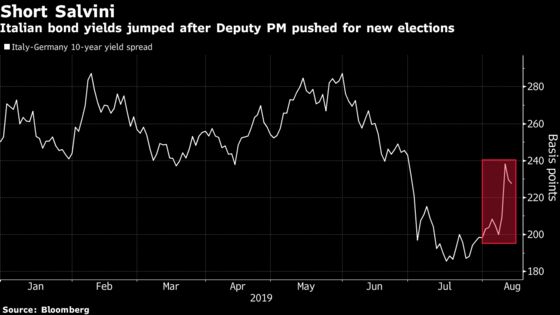

Italian 10-year yields jumped 26 basis points last week to touch 1.83%, the highest level in over a month. The premium investors need to pay over those on their German peers, a key gauge of risk sentiment in the country, hit a six-week high of 238 basis points. The flushing out of long positions may widen it further in the short term to 250 basis points, according to ING Groep NV.

Levels in “lo spread” above 300 made the front pages in Italy last year, and that is probably the “pain threshold” now, according to Fidelity’s Iannelli. The spread could climb to between 275 basis points and 300 basis points if Salvini seeks to form a government with other parties on the right such as the Brothers of Italy, according to AllianceBernstein.

“The most likely outcome is a coalition with center-right, but the probability of an outright League win or a coalition with the harder-right has definitely increased in recent weeks,” said John Taylor, a money manager at AllianceBernstein. “We’re in for a period of more volatility.”

Budget Buster

The League would get about 38% of the vote if elections were held now, according to pollster Noto Sondaggi. Salvini proposes simplifying income tax by lowering the rate to 15%, while stopping the VAT increase would cost the Treasury around 23 billion euros ($25.7 billion) or 1.3% of GDP. The nation is already the euro-area’s second-most indebted, after Greece, and Brussels threatened sanctions against Rome last year for a wider budget deficit.

The debt risk in the bloc’s third-biggest economy is weighing on the euro and helping boost demand for havens such as the Swiss franc and German bonds. Italy’s benchmark stock index has slid to hit a two-month low this week, while the cost of insuring the nation against default has surged to the highest this year.

QE Help

One boon for Italian bondholders though is the prospect of a fresh program of quantitative easing from the European Central Bank -- potentially starting in September. While the ECB is up against limits in countries such as Germany, it still has room to buy debt from Italy.

For Danske Bank AS, Italy also retains the appeal of being one of the few nations in the euro area that doesn’t have most of its debt market offering negative returns. For Axa Investment Managers, low summer volumes mean it’s too early to see which direction the market will go.

“Now is probably not the right time to make decisions,” said Alessandro Tentori, chief investment officer at Axa Investment Managers, adding he wasn’t sure if Salvini’s reform agenda would be better or worse for markets than the existing government’s plans.

The prospect of the League governing without its current coalition partner, the anti-establishment Five Star Movement, had previously been seen as positive for the nation’s financial markets given their constant sparring and conflicting priorities over tax cuts. But over the last few months, Salvini has sounded the most forceful over ramping up spending on infrastructure.

Italy won’t be able to contain the budget deficit below 2% -- seen as a potential line in the sand for the European Commission in the last dispute -- if it’s going to deliver promised investments and tax cuts, Salvini has said. To avoid disciplinary action by the Commission, Rome agreed to keep this year’s shortfall at 2.04%, with talks about the 2020 budget due to start next month.

“The prospect of a more assertive, and more powerful, Salvini raises the prospect of protracted tensions with the EU,” said ING strategists including Antoine Bouvet. “The build-up to the Italian election would coincide with the build-up to Brexit. If we get that, we see the 10-year Italy-Germany spread testing 300 basis points.”

To contact the reporter on this story: John Ainger in London at jainger@bloomberg.net

To contact the editors responsible for this story: Ven Ram at vram1@bloomberg.net, Neil Chatterjee, Alessandro Speciale

©2019 Bloomberg L.P.