Israeli Economy Shrinks Most in at Least 45 Years After Lockdown

Israeli Economy Shrinks Most in at Least 45 Years After Lockdown

(Bloomberg) --

Israel’s economy contracted the most since at least 1975 as a result of the Covid-19 pandemic and a near-total lockdown imposed by the government to bring the outbreak under control.

Gross domestic product shrank a seasonally adjusted, annualized 28.7% in the second quarter, according to the Central Bureau of Statistics, more than quadruple the drop in the previous three months and worse than the median estimate in a Bloomberg survey for a decline of 27.7%.

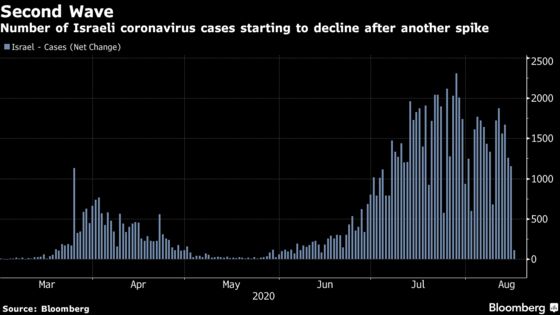

While infections slowed in late April and Israel turned to a gradual reopening of the economy, the country has since suffered a setback in keeping contagion in check. It’s now in the middle of a second virus wave that reached record highs, though new cases have seemed to level off in recent weeks.

In response, the government has turned on the fiscal taps to provide a social safety net and bolster the economy, allowing the budget deficit and debt burden to balloon. Prime Minister Benjamin Netanyahu announced a further 8.5 billion shekels ($2.5 billion) for stimulus and job creation after the latest economic figures were reported on Sunday.

Netanyahu said Israel has fared well relative to grim readings in Europe and elsewhere, a result he attributed to the government’s “responsible policy” of protecting lives and limiting damage to the economy.

“It’s more or less in line with what you see in the world,” said Gil Bufman, chief economist for Bank Leumi Le-Israel. “The threat of closures is quite substantial going ahead because we’ve not beaten the virus yet, we’ve not been able to be as effective as some of the European countries have been.”

The disease’s spread and Israel’s containment measures hurt categories nearly across the board, with private consumption taking the biggest hit, data released on Sunday showed.

- The deterioration follows the poor performance in the first three months of the year, which marked the first quarterly contraction since 2012 and the worst economic showing in at least 25 years

- During most of April, Israeli officials imposed restrictions on movement and businesses during the height of the first wave of cases and only began easing up regulations from late April, with travel still largely closed to foreigners

- Private consumption, an engine of Israel’s economy, led declines with a drop of 43.4%, while imports fell 41.7% and output of the business sector saw a contraction of 33.4%

- Government consumption expenditure rose 25.2%, marking the only gain in GDP components, as the Finance Ministry deployed roughly 200 billion shekels of crisis stimulus to boost the economy

- For 2020, the country’s central bank expects a contraction of 6%, with growth rebounding 7.5% next year

Goldman Sachs Group Inc. economists now expect Israel’s rebound to be “more gradual” than initially thought because of the additional disruptions caused by the pandemic. In a report before Sunday’s data release, they kept this year’s growth forecast at minus 5.5% “as a slower recovery due to the second wave offsets the positive contribution from opening up earlier.”

©2020 Bloomberg L.P.