In Warning to May, EU History Shows Late Summits Don’t End Well

In Warning to May, EU History Shows Late Summits Don't End Well

(Bloomberg) -- Theresa May’s strategy to take Brexit talks down to the wire is unlikely to end well – if history is anything to go by.

Over the past decades, leaders and governments counting on 11th-hour concessions from the European Union either ended up capitulating or got much less than they had hoped for. That’s because decisions by EU leaders can only be taken by unanimity following tedious preparatory work by aides, diplomats and ministers. So when the bloc reaches a consensus position, as is the case with Brexit, it’s almost impossible to change it overnight.

There is a lesson for the U.K. premier in all this: be ready to manage defeat, don’t raise expectations too much, and pay more attention to the French. The following recent examples should give her pause.

July 2015: Greek Capitulation

- What Happened: Prime Minister Alexis Tsipras was catapulted into office on a promise to end austerity and negotiate a “substantial haircut” of the country’s public debt. After six months of brinkmanship, he arrived at a crunch summit in Brussels with a resounding mandate to reject the euro-area’s terms for financial assistance. EU governments didn’t budge. Some 17 hours of talks later, in the wee hours of July 13, 2015, Tsipras signed off on a long list of austerity and economic measures, including pension cuts and privatizations.

- Impact: Tsipras’s terms of surrender – for example to refrain from presenting most legislation to the Greek parliament without prior consent of mid-level EU bureaucrats – were humiliating. He wagered that the EU wouldn’t risk allowing the break-up of its currency bloc, but Brussels called his bluff. Greece’s economy and banks are still licking their wounds.

March 2013: Deposit Haircut

- What Happened: When Greece’s 2012 debt restructuring, a recession and a plunge in real estate prices exposed the unsustainable business model of Cypriot banks, EU officials told the government in Nicosia that deposits in its lenders were too big to save. At a dramatic all-nighter in Brussels, Cypriot President Nicos Anastasiades told his peers he couldn’t accept the levy on the savings demanded. “Then I’ll call Panicos to seal the banks,” European Central Bank board member Jörg Asmussen responded, referring to Cypriot central banker Panicos Demetriades. The threat forced Cyprus’s government back to the negotiating table.

- Impact: Cyprus rejected an initial deal offered by EU governments for a 9.9 percent levy on deposits in exchange for a bailout, only to end up with a worse accord at another dramatic meeting a few days later - which wiped out all deposits over 100,000 euros in its second biggest bank and almost half of the deposits over 100,000 in its largest. A different offer doesn’t always mean a better offer.

December 2011: Making Enemies

- What Happened: As the global financial downturn plunged Europe into its worst economic crisis and the future of the euro hung in the balance, then-British Prime Minister David Cameron used a late-night Brussels summit to wield Britain’s big stick. The EU wanted to draw up an emergency treaty with tougher national spending rules to safeguard the single currency, but Cameron demanded it include concessions to protect the U.K.’s financial services industry. When he didn’t get them, he vetoed the whole thing at 2:30 a.m. in the Belgian capital.

- Impact: Relations soured. Cameron won the battle but lost the war. And the EU did just as it wanted to with an intergovernmental treaty, minus the U.K.

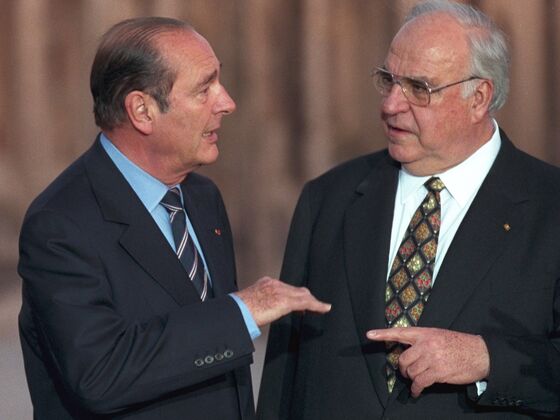

May 1998: Franco-German Clash

- What Happened: A battle between French President Jacques Chirac and German Chancellor Helmut Kohl over the choice of the first European Central Bank chief laid bare political differences at the heart of the euro eight months before it was introduced by 11 nations. Chirac showed the supremacy of politicians over technocrats – and the influence of France over Germany – by insisting Kohl-backed Dutch central banker Wim Duisenberg step down halfway through his eight-year term atop the ECB to make way for a French national. As the Chirac-Kohl standoff dragged on into the night, finance ministers got so bored that French Finance Minister Dominique Strauss Kahn passed around a paper and asked his colleagues to write their predictions for the upcoming World Cup.

- Impact: Chirac’s intransigence challenged the notion of ECB independence promised by the German establishment and put Kohl in a corner from which he emerged at the summit looking like an exhausted boxer. The EU leaders’ deliberations over the matter were “heart-pounding,” the U.K. government spokesman said at the time (British Prime Minister Tony Blair chaired the EU summit because it took place while the U.K. held the bloc’s rotating six-month presidency). Two decades since its inception and 10 years after a Greek-triggered debt crisis almost broke it apart, the euro – now shared by 19 countries – is still underpinned by a fine balance between European political realities and legal necessities.

--With assistance from Nikos Chrysoloras, Ian Wishart, Jonathan Stearns, Viktoria Dendrinou and Gregory Viscusi.

To contact the editor responsible for this story: Caroline Alexander at calexander1@bloomberg.net, Mark Williams

©2019 Bloomberg L.P.

With assistance from Bloomberg