U.K. Election Prospect Has Market Players Scratching Their Heads

Here’s What Market Strategists Are Saying About U.K. Election

(Bloomberg) -- Prime Minister Boris Johnson may be trying to break the logjam over the departure from the European Union with a general election, but for the market players the vote is another cause of uncertainty.

On Tuesday after the market closed, Johnson won crucial votes in the House of Commons for the general election on Dec. 12, which now needs to be approved by the House of Lords. The benchmark FTSE 100 Index and the mid-cap FTSE 250 Index were little changed in early London trading. They fell yesterday after it became clear the opposition Labour Party backed an election.

Here’s what investors and strategists are saying about the implications for U.K. stocks:

Karen Ward, JPMorgan Asset Management

“With the U.K. population returning to the polls in a bid to resolve the Brexit impasse, uncertainties about the result argue against significant positioning in sterling assets in either direction.

“Sterling assets may react negatively to any signs that Boris Johnson is struggling to compete with the Brexit Party, which could push him to return to his no-deal rhetoric. We continue to believe that a no-deal Brexit would coincide with sterling in the region of 1.10 against the U.S. dollar.

“It is also entirely possible, however, that the U.K. population is as divided as it was three years ago and as a result no party will obtain a majority. While this might appear to be the worst-case scenario for resolving the impasse, it is possible that it would force a cross-party solution to Brexit and ultimately a softer Brexit outcome. After all, if a more comprehensive free-trade agreement was not negotiated over the period of transition, Johnson’s deal could still see significant disruption to U.K. trade. Significant positioning in sterling assets in either direction looks unwise.”

Rene Defossez, Natixis

“Snap elections in December would not be the end of the Brexit saga. To a large extent, these elections will be a disguised second referendum, because the main topic will be Brexit.

“There is a huge risk of a hung parliament, as suggested by the recent polls. In that case, the political situation would become even more chaotic. To put it bluntly, all the Brexit scenarios remain on the table. This is the reason why markets’ reaction to the news has been very cautious.”

Luke Newman, Janus Henderson

“I’d be very surprised if the election wasn’t a lot closer than the polls are betraying at the moment. That means for U.K. banks, utilities, defense companies and housebuilders, possibly we see some more pressure over the next six weeks. And if Boris wins his majority, of course you could see some relief in the sterling and those sectors in the end.

“We do have some short positions within utilities and banks—with the latter being a longer-term short position for the fund. In light of the election, we need to balance the probability of a Corbyn government. Yes, we’ve incrementally shorted some utility companies over the last week or so.”

Paul Mumford, Cavendish Asset Management

“Whatever the outcome, it should be good for U.K. equities. However, if sterling recovers strongly the emphasis would be more on shares in domestic companies and importers.

“Whichever party wins it will surely lead to higher government spending and remove a major uncertainty from the system as the current minority government would find it impossible to rule effectively.

“Companies would be able to plan ahead knowing that the country would be in for a period of stable government. If there is no overall majority, the country would be no worse off than at present.”

David Holohan, Mediolanum

“While an election is a necessary next step in order to try and break the current parliament logjam, there is no guarantee that that the parliamentary arithmetic will be improved by such an action. The political parties remain split between supporters of remaining in the EU and those in favor of Brexit, which limits the likelihood of the election providing a clear direction for investors.

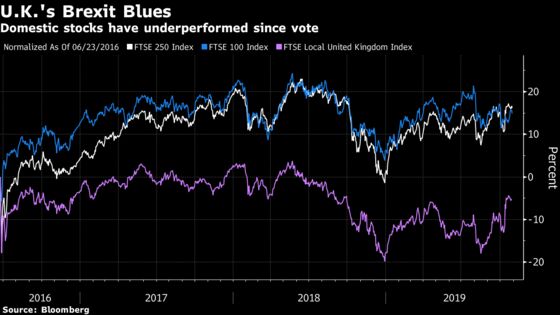

“Given this scenario, U.K. asset performance is likely going to continue to be dominated by the strength or weakness of sterling, with strength supporting FSTE 250 stocks and weakness supporting the FTSE 100. Provided a hard Brexit remains off the table, U.K. assets are likely to become more favored by investors.”

| Read more: |

|---|

| Pound Needs More Than Election Date to Sustain October’s Rally |

| Pound’s Best-Case Election Winner May Not Be Johnson, RBC Says |

| Labour Coalition Would Be Positive For Sterling, Says ING |

Jim Wood-Smith, Hawksmoor Investment Management

“The market’s hope is that this unholy mess will possibly result in a Boris Johnson majority. On the other hand, if the election serves only to muddy further the muddiest of waters, then the possibility of no deal at the end of January is right back on the table.

“Quite bizarrely, it was possible to argue that the best thing for the market was for the election not to happen and for the Withdrawal Act to proceed and be passed by Parliament. That would at least have given clarity on the way ahead. The light at the end of the tunnel has become considerably dimmer. The pro-domestic and pro-sterling trade is probably still the right one, but it would be extraordinarily brave to bet too much on it.”

Andrew Coury, strategist, Liberum Capital Ltd.

“While fears of nationalization under Corbyn’s rule have remained subdued with lingering Brexit angst, a renewed Labour leadership campaign could weigh heavily on U.K. utilities.

Domestically focused companies should rally significantly if the election results in a Brexit under a re-elected Johnson government, he said. Housebuilders, leisure, consumer, real-estate and bank shares would rebound substantially, he said.

--With assistance from Michael Msika.

To contact the reporters on this story: Sam Unsted in London at sunsted@bloomberg.net;Joe Easton in London at jeaston7@bloomberg.net;Ksenia Galouchko in London at kgalouchko1@bloomberg.net

To contact the editors responsible for this story: Celeste Perri at cperri@bloomberg.net, Phil Serafino, Beth Mellor

©2019 Bloomberg L.P.