Argentina to Lead Emerging-Market Rebound in 2019, Says Templeton Bond Head

Argentina to Lead Emerging-Market Rebound in 2019, Says Templeton Bond Head

(Bloomberg) -- An emerging-market money manager known for making contrarian bets says Argentina, home to the world’s worst-performing currency this year, looks primed to lead a developing-nation rebound in early 2019.

Franklin Templeton’s Michael Hasenstab, who oversees the $35 billion Templeton Global Bond Fund, also ranked Brazil and India among the top three opportunities. He sees Brazil’s newly elected leader Jair Bolsonaro as well as India’s Narendra Modi as dramatic upgrades from their predecessors.

Politics also drives his taste for Argentina, where he expects President Mauricio Macri to win re-election next year and continue to pursue policies aimed at limiting inflation, curbing the budget deficit, stabilizing the currency and stoking economic growth. While Macri has faced his share of tests recently amid a market selloff, high inflation and an economic contraction, his approval rating is holding up fairly well while his political adversary, former President Cristina Fernandez de Kirchner, has been indicted on corruption allegations.

“He remains quite popular considering the country is going into a recession,” Hasenstab said in an interview. “I think that says a lot. It’s because people were so exhausted and frustrated and impoverished by the past regime that they still want change.”

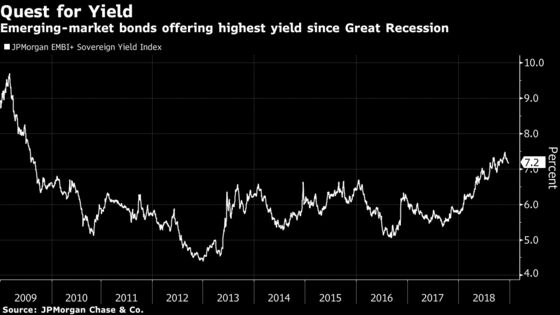

The money manager’s optimism toward some of the developing world’s weakest links comes during a year in which equities slid into a bear market, every emerging-market currency fell against the dollar and sovereign yields soared to a nine-year high. Hasenstab has a reputation for making big bets on distressed countries. The strategy paid off handsomely when he scooped up Irish bonds during the European debt crisis, yet backfired in war-torn Ukraine a few years later.

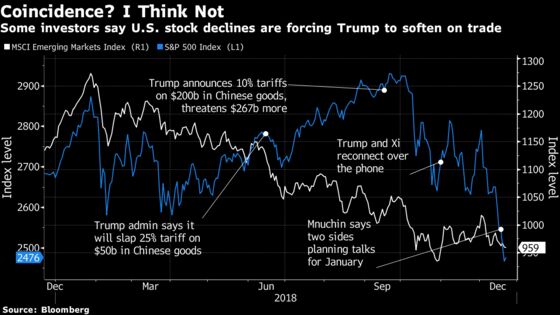

Hasenstab said investors overreacted this year to Fed tightening, which is already priced in to assets. Meantime, it’s quite possible the U.S. and China could reach a trade truce in 2019, helping fuel a rally in developing-nation assets next year.

"The base case is you see a lot of fanfare and if it follows the Mexico-Canada example then it gets resolved within a year or so," Hasenstab said. "Eventually we’ll get a resolution."

Here’s what else he had to say about the outlook in 2019:

On Fed support for EM

- “EM assets are set up for some decent appreciation given they’ve priced in a lot of these adjustments. A more dovish Fed is only more positive for EM. Given what’s already being priced into EM, they look to have pretty good value in the first part of the year.”

On Treasury yields

- “We’re set up for a move towards 4 percent, if not higher. The variable will be how financial markets absorb the rise in interest rates. It’s unlikely that the next 50 to 75 basis points, if it can happen in a reasonably managed fashion, that both the real sector and financial markets can absorb those adjustments.”

On the trade war

- “It’s clear that the equity market has been a report card that Donald Trump has looked at. It could have some influence. It’s also clear that there’s no quick fix to the trade discussions with China. It will take some time. If we look at Mexico’s case, it was resolved under the radar. There was a reasonably expedient resolution to updated Nafta.”

On euro risks

- “The risks in Europe are underappreciated. People have become too complacent about the euro. The difference now versus 2011 is in 2011 there was a political consensus for countries to come together and coordinate a bailout for Greece to keep this project alive. We don’t see the same voter preferences or political will to do something like that. We continue to have a fairly large short euro position.”

On where to avoid in EM

- “We don’t have any investments in Turkey at this point. The difference there is Argentina came under a speculative attack and they took all the right measures and got the endorsement of the IMF and significant financial resources and swap lines from China. They’re without question on a path to regain stability because all the aggressive policy measures they took. We don’t see those same policy measures or broad international support in Turkey.”

- “I don’t think there’s value at this point in Venezuela. It’s well beyond a financial crisis. It’s a humanitarian crisis. It’s our lowest ranked ESG country. We expect things to get even worse. I don’t think there’s any alignment of financial as well as social interests. The base case is Nicolas Maduro’s government stays in power, although ultimately there will have to be some change.”

To contact the reporter on this story: Ben Bartenstein in New York at bbartenstei3@bloomberg.net

To contact the editors responsible for this story: Rita Nazareth at rnazareth@bloomberg.net, Brendan Walsh

©2018 Bloomberg L.P.