Fed Should Buy Muni Bonds to Fight the Next Recession

Fed Should Buy Muni Bonds to Fight the Next Recession

(Bloomberg Opinion) -- Almost 10 years after the Great Recession ended, the growing threat of a new economic slowdown raises a troubling question: When the next recession strikes, what can the world’s central banks do? With interest rates low and their balance sheets still loaded with assets bought to fight the 2008 crisis, do they have the tools to respond? This column is one of five looking at that question.

U.S. state governments suffered major damage from the last recession 10 years ago. During the second quarter of 2009, the final months of the downturn, personal income taxes tumbled 27 percent from a year earlier. At the same time, expenses grew as enrollment for Medicaid and state unemployment insurance soared, while crumbling asset prices suddenly left public pension systems with massive shortfalls relative to their liabilities. In statehouses across the country, money was tight, to say the least. California went so far as to issue IOUs.

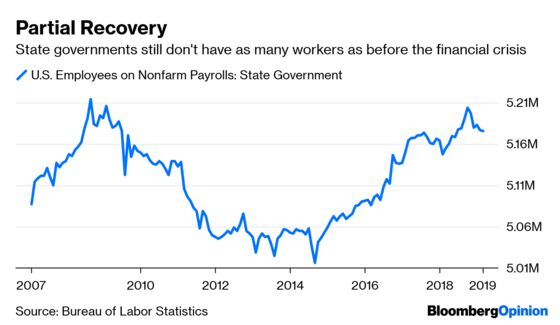

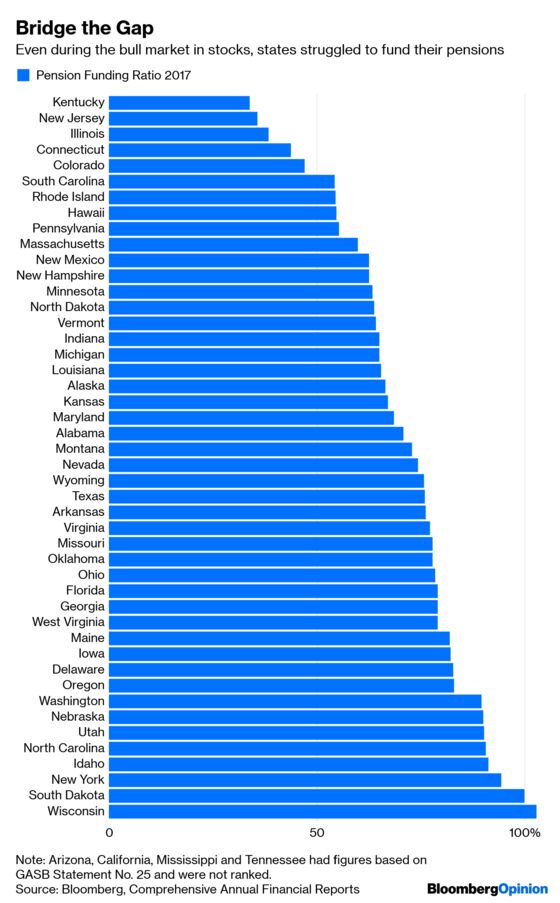

Over the past decade, the slow-but-steady economic expansion has covered up these issues, but hasn’t erased them. State government employment remains below its pre-financial crisis peak. Public pension plans are still largely in a sea of red ink, with an overall shortfall of $1.4 trillion at the state level, and even those with an acceptable level of assets are just one bear market away from the brink. And it’s no secret that the U.S. has fallen terribly behind in funding its roads, bridges, airports and public transit systems. The American Society of Civil Engineers estimates the money needed to get infrastructure into an overall “state of good repair” will fall short by $2 trillion over the next several years.

As the Federal Reserve contemplates what the next recession might look like, and what tools it has available to combat it, the fiscal health of U.S. states is likely to emerge as a significant roadblock to any economic recovery. Unlike the federal government, states can’t rely on running persistent budget deficits during a downturn, nor can they rapidly add workers to their payrolls. That means either sharp cutbacks in public services, higher taxes or shortchanging pensions. None of those options will stimulate growth.

The easy answer would be directing more cash from the federal government to the states. But the 2009 stimulus program already transferred an unprecedented amount of money into state coffers and the results were middling at best. In the current political climate, and with U.S. deficits already running close to $1 trillion, it’s anyone’s guess whether a similar package could come together.

Related:

The Fed Needs to Fight the Next Recession Now

How to Stop Rising Inequality in the Next Recession

The Fed Will Have to Risk More in the Next Recession

That means it might be up to the the Fed to get involved in the $3.8 trillion municipal-bond market to give states a much-needed boost. The central bank can only do so much during a downturn to get companies and individuals to borrow. But by directly backing states, it will immediately allow them to make payroll, start on new infrastructure projects, or both.

First, to get the obvious out of the way: The Federal Reserve Act largely prohibits such a move, only allowing the central bank to purchase munis with maturities up to six months. That means any such plan would still require some political will to amend the law. But if the Fed could gobble up toxic assets in the wake of the financial crisis, it’s hard to see why adding state debt to its balance sheet would be so controversial.

As for a global precedent, officials need only look to the European Central Bank, which owns a portfolio of sovereign bonds, including debt of low-rated Italy, Portugal and Spain. They are to triple-A Germany what Connecticut, Illinois and New Jersey are to states with top grades like Georgia, Maryland and Utah. That’s how 10-year yields in the so-called peripheral European countries are mostly lower than U.S. Treasuries.

Naturally, the risk in having the Fed buy munis is that the central bank’s balance sheet is roughly the size of the entire market, and therefore its purchases could end up distorting new offerings and secondary trading. Demand for tax-exempt debt is already on the rise because of new limits on state and local tax deductions. The scarcity of bonds has gotten so severe that some investors are embroiled in a bitter lawsuit.

For the Fed to be most effective, its bond-buying program should be well-defined and narrow in scope. The most obvious parameter: It could only buy state-level general obligations. This reduces the number of different bonds it owns, while leaving it to elected governors to distribute the benefits to cities and towns.

The more complicated factor is exactly how the Fed would buy these bonds. The strongest form of intervention would be having states place debt directly with the central bank at a low fixed interest rate, giving the states a major influx of cash at a minuscule cost . This option is almost like a federal grant, only they have to pay back the principal when the debt matures. But if the recovery works out as planned, that shouldn’t be a problem.

Alternatively, the Fed could provide a cap on interest rates at new bond sales by pledging to take down any part of an offering that exceeds a pre-determined yield level. This would give muni investors a chance to still purchase some of the securities, though at lower yields than the market might otherwise dictate.

Of course, such lending from the Fed would need to have some limitations, specifically the amount of debt it’s willing to absorb in any given period and how much from each state. But as far as the proceeds, most uses seem like fair game, aside from subsidizing a large corporation or a sports franchise. Bonds for general “deficit financing” will offset the need to either raise taxes, cut workers, delay infrastructure repairs or redirect pension payments.

A similar sort of idea has been proposed before, though not involving the Fed. In 2008, Philadelphia, Atlanta and Phoenix asked the U.S. Treasury for $50 billion on behalf of cities to spend on infrastructure and loans lasting as long as a year to aid cash flow. They were denied.

Say what you will about modern monetary theory, but it’s worth asking why it’s assumed that states in America, which wields the power of the world’s reserve currency, should turn to draconian austerity measures when the going gets rough. After all, no political party at the federal level even pretends to care about budget balance anymore. Governors, on the other hand, must spend within their means and consider trade-offs, whether they’re a Democrat or Republican. To their credit, many have chipped away at long-term problems.

When the next recession comes around, though, they might not have the tools to go at it alone. They’re going to need a lift. The Fed should stand ready to provide that boost.

To provide cheap financing but also encourage timely repayment, these bonds could have a “step up” structure. For instance, a state could issue 10-year securities at par with a 0.5percent coupon for the first three years, a 1percent coupon for the next three, anda 3percent coupon for the last four. The state would have the option to pay off the debt after year three, year six or year 10.

To contact the editor responsible for this story: James Greiff at jgreiff@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2019 Bloomberg L.P.