Fannie-Freddie Overseer Puts Squeeze on $50 Billion Bond Market

Fannie-Freddie Overseer Puts Squeeze on $50 Billion Bond Market

(Bloomberg) -- A bond market once thought to be key to the futures of Fannie Mae and Freddie Mac -- and the roughly $5 trillion of home loans they backstop -- could instead find itself on the scrap heap due to their own regulator.

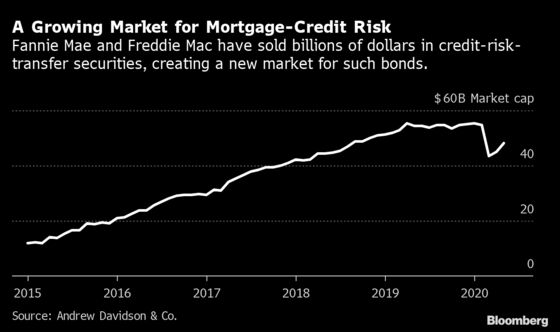

In the past several years, so-called credit-risk-transfer securities have been a primary way for government-controlled Fannie and Freddie to offload the risk of borrowers defaulting on their mortgages to private investors. The market value of such assets, known as CRT, has grown to about $50 billion, with mutual funds, hedge funds and real-estate investment trusts among investors snatching up the bonds.

Some former government officials and housing-finance executives have even loftier ambitions and believe the swelling CRT market can largely eliminate the likelihood that U.S. taxpayers would ever again bail out Fannie and Freddie, as they did during the 2008 crisis.

But a new rule proposal by the Federal Housing Finance Agency, which regulates the mortgage giants, would drastically cut Fannie and Freddie’s incentive to continue selling the bonds. The move would likely shrink the market significantly, in effect leading the companies to keep as much risk as they did when the housing market collapsed more than a decade ago, according to the proposal’s detractors

“We think it might kill CRT, and that this might be their intent,” said Michael Bright, chief executive officer of the Structured Finance Association, whose members include investors in the risk-transfer securities.

‘Likely Demise’

The FHFA’s treatment of the assets “has been taken by many housing-finance policy specialists as an attempt to deliberately render the program uneconomic and thus ensure its likely demise,” former Freddie CEO Donald Layton wrote in a blog post published Monday.

Layton released a separate white paper this week in which he wrote that FHFA Director Mark Calabria has expressed skepticism in private conversations over the effectiveness of CRT. Calabria, according to Layton, has sometimes compared the securities to credit default swaps, assets that didn’t provide the protection that investors expected during the 2008 meltdown and contributed significantly to the global credit crunch.

The regulation that’s generating the debate over CRT is a plan FHFA released in May to boost capital standards for Fannie and Freddie by tens of billions of dollars. The objective is to ensure they have adequate cushions to absorb losses, thus paving the way to follow through on the Trump administration’s goal of releasing the companies from federal control. But the proposal, which could be finalized this year, would also severely curtail the capital relief that Fannie and Freddie receive for issuing CRT securities.

”The proposed rule continues to provide significant capital relief for CRT while ensuring that regulatory capital is appropriate for the exposures retained” by Fannie and Freddie, FHFA spokesman Raphael Williams said in an email. Williams said the agency will seek input to better assess how the proposal may impact the companies’ future business.

Fannie and Freddie don’t make mortgages themselves. Instead, they buy loans from lenders, wrap them into securities and guarantee the payment of principal and interest to bond investors. That process has helped make the 30-year fixed-rate mortgage a fixture in the U.S. But it also leaves Fannie and Freddie exposed to losses if borrowers stop making their payments.

To lessen the risk, Freddie and Fannie in 2013 began to sell credit-risk-transfer securities. CRT are a kind of bond whose performance depends on that of a pool of Fannie or Freddie mortgages. Money that investors use to buy CRT is put into a trust, and the investors get paid principal and interest unless too many mortgages sour.

Former President Barack Obama’s Treasury Department, members of Congress and the FHFA under past Director Mel Watt all encouraged the issuance of CRT, since they believed the securities could transfer default risk to private investors and away from taxpayers.

The secondary market for CRT is still relatively small, and at the beginning of the coronavirus pandemic, it nearly froze, with some investors reporting that they were having trouble even getting prices for some bonds. But by June, it had mostly recovered amid unprecedented government stimulus from the Federal Reserve and other agencies.

Freddie’s Offering

On Monday, Freddie announced the issuance of its first single-family CRT since March, saying that strong investor demand had prompted it to double the size of the offering.

The capital hit that the FHFA rule would impose on such transactions is hard to overstate. In fact as of September 2019, the month that the FHFA used to illustrate its proposal, Fannie and Freddie wouldn’t get any capital relief at all, because the agency said the companies would be bound by a minimum leverage ratio.

Even in other economic climates, when the leverage ratio wasn’t binding, Fannie and Freddie would get about half as much credit under Calabria’s proposal as they would have through an earlier regulation put forth by Watt that was never finalized.

“If the rule as proposed goes through, it would make CRT uneconomic for Fannie Mae and Freddie Mac,” said Andrew Davidson, founder of Andrew Davidson & Co., a mortgage analytics firm.

‘Punitive Approach’

Advocates for the bonds have already started pushing back.

At a House hearing with Treasury Secretary Steven Mnuchin and Fed Chairman Jerome Powell last week, Republican Representative Blaine Luetkemeyer of Missouri said the FHFA’s proposal “seems to have taken a confused and more punitive approach to certain types of CRT.”

Mnuchin and Powell agreed that Fannie and Freddie should receive capital relief for issuing CRT. Mnuchin said the Financial Stability Oversight Council -- a Treasury-led panel whose members include Powell and the heads of other regulators -- was reviewing the FHFA’s proposal. It’s also being examined by the Fed, Powell added.

The FHFA is accepting comments on the capital proposal until the end of August and has said it hopes to finalize the rule this year.

©2020 Bloomberg L.P.