Euro Is Only Partly to Blame for Currency Pain in Europe’s East

Euro Is Only Partly to Blame for Currency Pain in Europe’s East

(Bloomberg) -- Terms of Trade is a daily newsletter that untangles a world embroiled in trade wars. Sign up here.

At face value, the euro is to blame for the currency slide across eastern Europe, because the region’s economies are enmeshed with European Union supply chains.

But there’s more to the story.

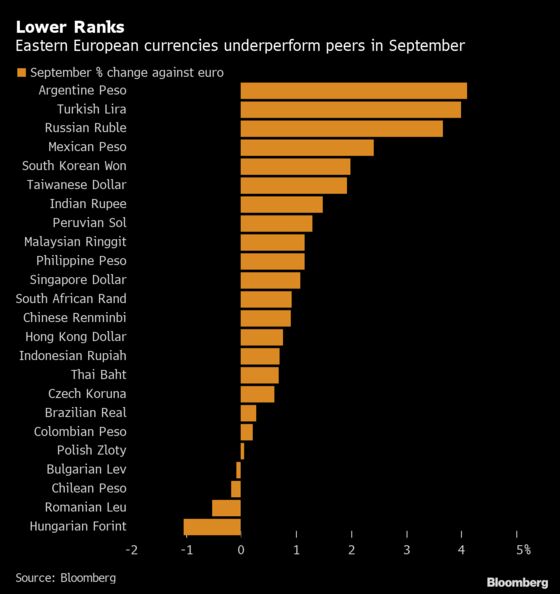

From elections and EU court rulings to government spending and monetary-policy quirks, homegrown headwinds have placed Hungary’s forint, the Polish zloty, the Czech koruna and the Romanian leu among the worst performing emerging-market currencies this month.

It’s an unusual predicament for assets often considered havens, especially given burgeoning consumerism and growing wages in some countries.

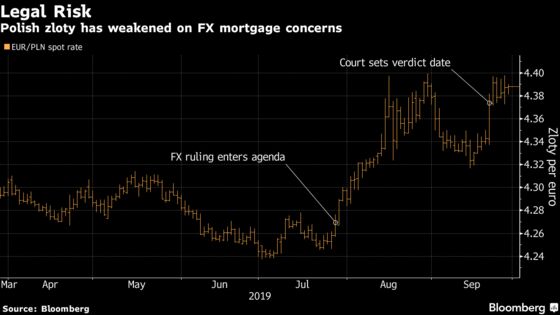

Polish Zloty

The zloty is feeling the heat of a looming European court verdict on foreign-currency loans. A worst-case scenario where banks would be obliged to convert mortgages to zloty at 2008 exchange rates could mean a loss of as much as four times last year’s annual profit for lenders. Accelerating inflation as well as general elections next month may also hurt the appeal of Polish assets.

“The 4.40 support has once again stopped the upward movement for now,” said Raiffeisen Bank analyst Dorota Strauch, who is based in Warsaw. “In anticipation of the ruling, however, it is likely that this level will be breached.”

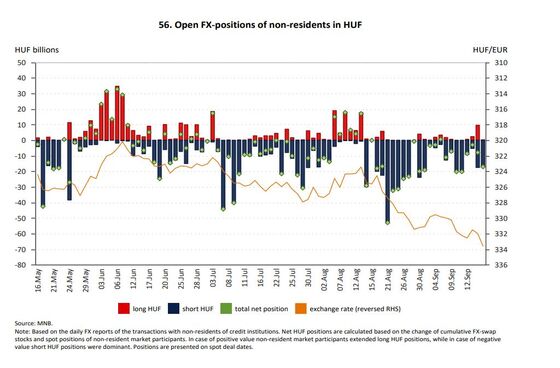

Hungarian Forint

The forint is the worst performer this month, hitting a record low against the euro. A dovish turn from the central bank and a build-up of speculative positioning against the currency have added to its pain. A current-account balance that has turned to a deficit isn’t helping either.

Rising liquidity after the central bank’s decision to relax monetary policy, as well as “the delicate external balance of Hungary and downward squeeze on the euro,” will keep pressure on the forint, according to Citigroup London-based strategists Dumitru Vicol and Luis Costa, who have an underweight call for the currency.

Czech Koruna

Hawkish overtones from rate setters in Prague haven’t lifted the koruna, whose 0.6% gain to 25.79 per euro this month has lagged emerging peers. Investors are still struggling to sell the koruna in an attempt to exit long bets made during the central bank’s currency cap regime.

“For some time the transmission mechanism from the interest rate channel into the exchange rate has been broken, with the overbought koruna not reacting to higher rates,” ING strategist Petr Krpata said in an emailed note from London. The euro-koruna may trend higher in 4Q and test the 26 level, even if policy makers hike rates in November, he said.

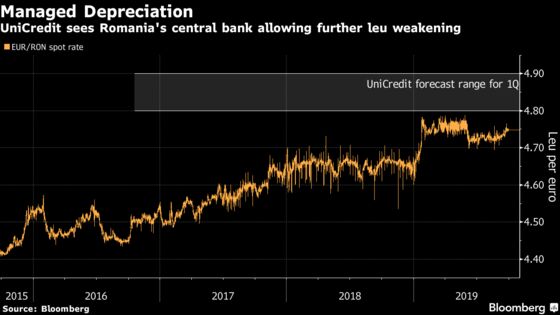

Romanian Leu

The leu has slipped 0.5% this month to 4.7485 per euro, even though it’s the only currency among peers that’s managed by the central bank. A twin deficit, a government crisis and above-target inflation paint an ugly backdrop.

“The leu remains one of the most overvalued currencies in CEE and this step-by-step weakening will not eliminate overvaluation,” said Dan Bucsa, a London-based analyst at UniCredit SpA. He sees the trading range shifting to 4.8-4.9 per euro in the first quarter of 2020.

“The central bank may have to use its reserves to defend the currency next year if appetite for emerging-market assets weakens.

--With assistance from Adrian Krajewski.

To contact the reporter on this story: Marton Eder in Budapest at meder4@bloomberg.net

To contact the editors responsible for this story: Dana El Baltaji at delbaltaji@bloomberg.net, Alex Nicholson, Constantine Courcoulas

©2019 Bloomberg L.P.