Europe’s Rapidly Souring Economy, Politics Do the Euro No Favors

Europe’s Rapidly Souring Economy, Politics Do the Euro No Favors

(Bloomberg) -- As Europe’s economic outlook darkens, more funds are turning against the euro.

Manulife Asset Management, which oversees $364 billion globally, is shorting the currency in one of its funds on worsening economic data, growing political fault lines and the European Central Bank looking increasingly likely to engage in more easing. The risk in holding European assets means M&G Investments portfolio manager Wolfgang Bauer is short the euro as a hedge.

“We are short the euro against the dollar in our fund,” said Grant Peterkin, a senior managing director at Manulife’s Absolute Return Rates Fund. “This is purely because we feel that data, especially in core Europe, has deteriorated pretty rapidly. That’s coupled with a central bank turning a little more dovish on expectations that data might continue to worsen over the next three to six months.”

Peterkin has joined peers at Janus Henderson Group Plc and Allianz Global Investors to be positioned for weakness in the euro. The ECB, which until recently was expected to start lifting interest rates from record-low levels, is now discussing the need for new long-term loans for banks. Data released Friday showed euro-area factories suffered their biggest drop in orders in almost six years in February.

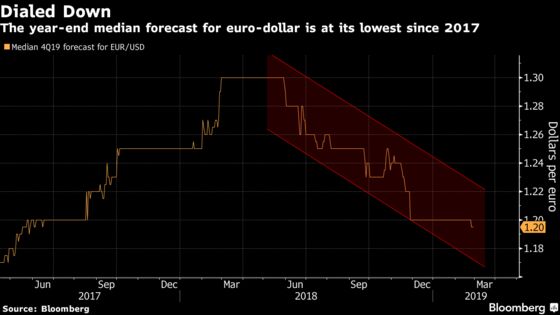

The common currency has slipped 0.9 percent so far this year to around $1.14. While the median forecast of strategists in a Bloomberg survey shows a recovery to $1.20 by the end of the year, that is the lowest consensus since August 2017. ABN Amro has slashed its second-quarter prediction to $1.10 from $1.19, while Rabobank, may lower its 12-month forecast of $1.15.

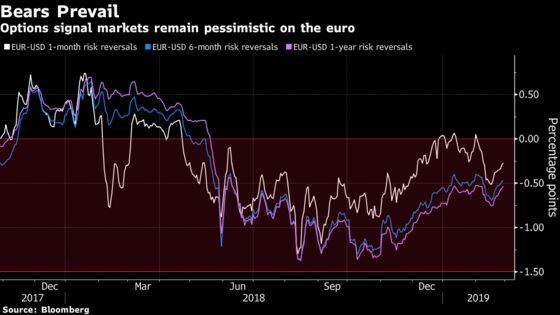

Slowing growth on both sides of the Atlantic is curbing volatility in the pair, while options traders have become more bearish on the euro. Risk-reversals, a gauge of sentiment and positioning, have mostly dropped this year. One-month contracts are around 30 basis points in favor of euro puts, from around neutral at the end of 2018 and January.

Market pricing also reflects growing doubts on policy normalization by the ECB. Contracts based on the Euro Overnight Index Average see the first ECB rate increase in April 2020, compared with December 2019 at end of June.

“Last year it was dollar strength, this year it’s about euro weakness,” said Jane Foley, head of currency strategy at Rabobank. Talk of more ECB easing “is very different to the expectations that existed at the end of last year.”

Hedging Europe

Any move by the ECB to lift rates would be “more like a one and done rather than a strong reversal” in policy, said Bauer at M&G, which oversees $380 billion. He is not taking any chances and shorting the euro to hedge exposure to Europe in his Absolute Return Bond Fund, which has outperformed 75 percent of peers in the past month according to Bloomberg data.

Politics is a key risk to the currency for Bauer. Spain is headed for its third general election in four years in April, a tenuous government coalition could unravel in Italy, French leader Emmanuel Macron is under pressure from “Yellow Vest” protesters and European parliamentary elections could spur gains for populist parties in May.

“At the moment in politics it is a bit eerily quiet. From this angle I see a little bit more downside risk,” Bauer said.

To contact the reporter on this story: Anooja Debnath in London at adebnath@bloomberg.net

To contact the editors responsible for this story: Ven Ram at vram1@bloomberg.net, Neil Chatterjee

©2019 Bloomberg L.P.