Global Debt Funds Shun Italy on Fears That Euro-Area Is Cracking

EU Rifts Spook Foreign Investors Enough to Question Its Future

(Bloomberg) -- Italian debt is once again the must-watch bellwether for growing tensions within the euro-area.

Global investors have lasered in on the nation’s bonds because, while they feature tempting yields, the government’s relatively weak finances add to the shared risk across the region. UniCredit SpA estimates foreign asset managers and hedge funds’ exposure to Italian government bonds may be around the lowest since December 2018.

It’s a familiar story -- albeit with a new twist. Every now and then, concern that the euro-area will break up drives investors to question whether holding the region’s assets is worth the risk. This time, economies are facing one of the most difficult challenges in living memory as a result of pandemic-induced shutdowns, adding to strains in the bloc that are likely to show up first in Italy’s bonds.

“We’re avoiding Italy at the moment because it’s probably that country where a lot of the political issues play out in the market,” said Bill Campbell, a portfolio manager at Los Angeles-based DoubleLine Capital, which oversaw $136 billion as of March. “Italian government bonds are going to express that risk first and foremost so we are out of that market until we get clarity.”

DoubleLine’s global bond fund is currently underweight on all core and periphery European sovereign bonds. That debt may get a jolt after Moody’s Investors Service publishes its rating decisions on both Italy and Greece on Friday.

ECB Backstop

Investors were already exasperated by the euro-area’s response to the spread of the coronavirus, and the damage it has wreaked on economies in the region, when a German high court gave the European Central Bank three months to fix its 2.7 trillion euro ($2.95 trillion) public sector purchase program that started in 2015.

It spurred concerns that more lawsuits may be filed against the ECB’s other vital programs, which have kept markets relatively buoyant through very turbulent times. German exports fell 11.8% in March, the most since at least 1990.

The policy maker’s bond-buying programs -- worth more than 1 trillion euros this year -- are why Italy’s 10-year bonds are yielding about 2% and not 7.5%, the level they climbed to less than a decade ago when its membership in the currency bloc was in question.

Indeed, the ECB’s support is the main reason Philadelphia-based Brandywine Global Investment Management bought Italian debt. It completed purchases of 10- and 30-year so-called BTPs on Tuesday, according to Jack McIntyre, a portfolio manager.

The company, which oversees $60 billion in assets mostly in bonds, didn’t own any European sovereign notes before the crisis. That’s because they weren’t attractive given the negative yields.

The Rift

The court ruling also highlighted the growing divide in the bloc and a stubborn problem with Europe: That it doesn’t have the combined fiscal infrastructure to match its joint monetary prowess. It’s one reason the euro is at a disadvantage to the U.S. dollar.

Case in point, the region’s leaders have struggled to agree on a joint bond issuance across member states, which would help countries such as Italy, where debt is well above the nation’s economic output. Euro-area finance ministers are holding a video meeting Friday to agree on the terms of emergency credit lines from the euro-area bailout fund.

“We’ve been trying to have a cohesive Europe since the ’60s,” said Jeremy Leach, chief executive officer at Managing Partners Group, which has hedged its exposure to the euro. “But I somehow feel that if they have a referendum in Italy or Spain today, populations might vote to leave.”

He started reducing his holdings of European stocks late last year because he didn’t think they were fairly valued. Leach expects a repricing of euro-denominated bonds as default risk rises and the common currency weakens.

Moody’s Has Its Say

Moody’s hinted last month that it may hold off downgrading Italy’s credit to junk from Baa3, the lowest investment grade. That’s on par with where Fitch Ratings knocked the nation’s credit score down to last week. Italy’s bonds climbed Friday, with yields dropping as much as eight basis points to 1.84%.

But should Moody’s decide to cut the nation’s rating to junk, Italy could start to see its bonds fall out of indexes, losing billions of euros of investment in the process.

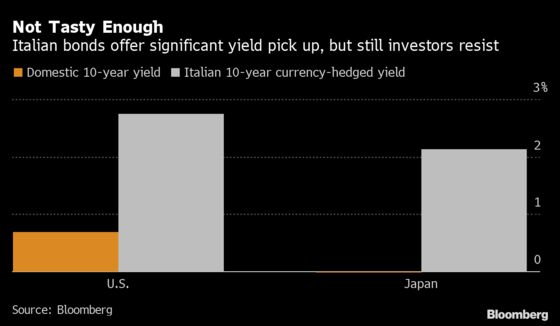

“Italian bond ratings can’t afford to fall,” said Eiichiro Miura, general manager of the fixed-income department at Nissay Asset Management, based in Tokyo. “Japanese investors will be reluctant about taking new exposures at this stage.”

That’s despite Italian 10-year debt currently offering a yield premium of over two percentage points versus domestic Japanese bonds, when adjusted for currency swings.

While the euro-area will probably “muddle through, the tail risk of the euro breaking up has increased,” said Eric Stein, co-director of global income at Eaton Vance Management. “You need a strong political will to keep this project going, and I’m surprised that we haven’t seen more cohesive policy or more integration after the previous crisis.”

©2020 Bloomberg L.P.