Italy’s Salvini Sticks to His Guns After Teasing Markets

EU Escalates Clash With Italy's Populists, Who Risk Budget Fines

(Bloomberg) -- Italian Deputy Premier Matteo Salvini stuck to his guns on the populist government’s spending spree, even as financial investors eager for reassurance saw signs he could eventually buckle under pressure from the European Union.

Salvini, who leads the anti-migration League, opened the door to tweaking the 2019 budget and “a polite dialogue” with the European Commission, the bloc’s executive arm, which took a first step towards imposing fines on Italy for violating fiscal rules. He insisted, however, that he won’t back down on the core points of the budget which include expensive promises on pension reform, welfare benefits, and tax cuts.

Italian bonds extended gains following the Brussels verdict, which the market had priced in, with possible fines still likely to be months away. Italian 10-year yields were on course for their biggest drop this month, falling as much as 15 basis points to 3.46 percent. The spread over those on their German peers was at 317 basis points as of 1:27 p.m. London time.

Markets have been hanging on Salvini’s every word as many see him as the real power in the coalition with the anti-establishment Five Star Movement. The League leader has challenged investors to widen the spread with German bunds to 400 basis points, and has overtaken Five Star in opinion polls ahead of next May’s European Parliament elections.

As the clash with Brussels hinges on who will give ground first, Salvini’s allusion to possible tweaks was interpreted by traders as flagging a potential capitulation.

“It is actually the piece of news we have been waiting for the last couple of weeks. Namely, that the Italian government are starting to give in,” said Arne Lohmann Rasmussen, head of fixed-income research at Danske Bank A/S. “It might be a small step for Salvini, but a rather big step for the BTP market. It may even be a sign that the threat of an excessive deficit procedure is having an effect.”

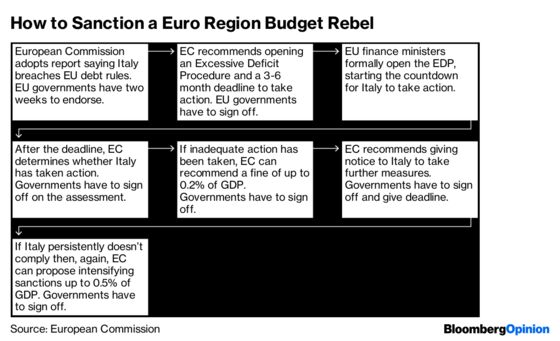

The commission said in its annual review of euro-area nations’ spending plans that Italy’s budget is in “particularly serious non-compliance” of EU limits. In a separate report on the country’s debt, the commission said Italy was not respecting the bloc’s rules on borrowing, which could lead to a so-called excessive deficit procedure involving possible fines.

While the EU has started such procedures for other countries in the past, it has never done so on the basis of excessive debt. It has also never actually fined any country.

Bonds initially rallied Wednesday morning on a report in newspaper La Stampa that Salvini may be open to spending revisions to avoid punishment. A League official denied the report and Salvini later clarified that the government will stick to the budget’s “guiding principles” on a lower retirement age, welfare benefits and tax cuts “but if people want to put more on investments in the budget, I’m open to dialogue with everyone.”

Salvini joked on receiving news of the EU’s review that “I had been waiting for a letter from Santa Claus.” He said he wants Europe to “respect the Italian people,” adding: “No one will ever manage to convince me that the Fornero law is right and should not be changed” -- a reference to pension reform.

Internal Tensions

The Brussels verdict ratchets up pressure on a coalition government already buffeted by financial markets and plagued by tensions between Five Star and the League. The two allies however share a determination to start fulfilling election promises.

Deputy premiers Luigi Di Maio of Five Star and Salvini have steadfastly stuck to targets for a 2.4 percent budget deficit and 1.5 percent economic growth next year that have irked the commission. In the latest dispute between the allies however, League lawmakers in the lower house voted with the opposition on an anti-corruption proposal late Tuesday, a defeat for the ruling coalition.

Italy’s first chance to negotiate after today’s move will be on Nov. 24 when Premier Giuseppe Conte has dinner with commission head Jean-Claude Juncker in Brussels, ahead of an EU summit on Brexit the following day.

But Italy has a tough task ahead given uncompromising stands from several EU partners who are particularly worried about the country’s debt mountain, the biggest in the bloc.

Huge Debt

“To deal with a debt of 130 percent of GDP, which is the task of any Italian government, is something much more difficult than if you act in a situation that is completely different,” German Finance Minister Olaf Scholz told Bloomberg Television on Tuesday. “The rules are not just the invention of someone, they have reasons and these reasons are part of the reality anyone has to deal with.”

Italy risks a procedure which could lead to disciplinary action, including freezing of certain funds and financial sanctions. There are, however, a lot of steps before fines would come into play. EU governments get several opportunities to weigh in and Italy could be given as much as six months more to comply once the process starts.

To contact the reporters on this story: John Follain in Rome at jfollain2@bloomberg.net;Viktoria Dendrinou in Brussels at vdendrinou@bloomberg.net;John Ainger in London at jainger@bloomberg.net

To contact the editors responsible for this story: Ben Sills at bsills@bloomberg.net, Alessandra Migliaccio, Richard Bravo

©2018 Bloomberg L.P.