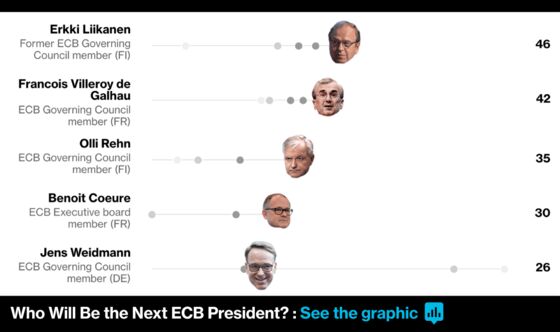

Enigma of Weidmann Looms Over Race to Succeed Draghi at ECB

European leaders wondering if Weidmann should replace Draghi at ECB have two competing views of Bundesbank chief to choose from.

(Bloomberg) -- Go inside the global economy with Stephanie Flanders in her new podcast, Stephanomics. Subscribe via Pocket Cast or iTunes.

European leaders wondering whether Jens Weidmann should replace Mario Draghi at the European Central Bank have two competing views of the Bundesbank chief to choose from.

One perspective, shared by some of his ECB colleagues, is that the German has been a thorn in the side of the current president for too long to shake off an aura of fundamentalism. Another, hinted at by Weidmann himself, is that of a pragmatist who can bend to the requirements of his office.

The Bundesbanker has made a corresponding journey from being the chief opponent of Draghi’s monetary expansion to a more restrained and mercurial role in ECB policy. The test Weidmann faces is whether that shift has come too late for him to be credible leading an institution that could plausibly be required to firefight another existential crisis.

“We’ve watched in the last two years how his communication has changed -- how it has gotten more compatible with the situation in more southern member states,” said Ricardo Garcia, UBS Global Wealth Management’s chief euro-zone economist. “We think Weidmann’s cards aren’t that bad.”

His chances of succeeding Draghi will hinge on a carve-up of senior European Union positions that the bloc’s leaders are planning after the European Parliament elections in late May. That negotiation will focus firstly on nationality, though leaders know they need to choose someone suitable for the job too.

During Weidmann’s time on the Governing Council, he’s been a more strident opponent than the other frontrunners to the major policies that defined the Draghi era. Here are some of the quandaries he could face if he gets the presidency.

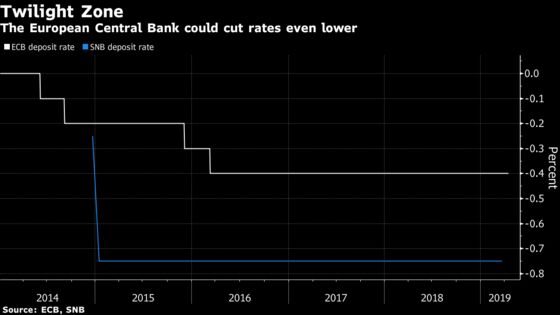

Negative Rates

A deterioration of the economy could force the ECB into another round of easing. Policy makers, including Draghi, say they still have tools at their disposal, and one response would be to cut interest rates still further. The ECB’s deposit rate is now at minus 0.4 percent, but Switzerland has shown that minus 0.75 percent is doable.

Although renowned for his hawkish views, Weidmann has previously spoken in favor of using negative rates. He said in 2014 -- the year the ECB took its deposit rate below zero -- that they could revive the interbank market and spur lending to companies.

“I’m not sure he’s quite as much as a hawk as portrayed,” said Stewart Robertson, European economist at Aviva. “He is a Bundesbank-type person, but I think everyone who has taken on the role as governor of the ECB has tried to do so looking at the euro zone as a whole.”

Quantitative Easing

Further asset purchases could help boost inflation if the ECB’s recently announced long-term loans prove insufficient. Weidmann was slow to acknowledge the legitimacy of quantitative easing before it was implemented in 2015. Since then, however, he has argued the program has certain safeguards -- such as weighting each country’s share according to the size of its economy -- that make it less prone to it being turned into a tool for debt mutualisation.

The problem for Weidmann is that if he wanted to reactivate QE, he might need to override the sovereign-bond safeguards he argued for because the ECB has already bought so much government debt.

Outright Monetary Transactions

Weidmann’s most persistent opposition to Draghi was on the president’s Outright Monetary Transactions bond-buying plan, a tool whose unveiling in 2012 helped stem the region’s sovereign-debt crisis despite never having been deployed. The Bundesbank chief even testified in court on his reservations.

But a new debt crisis, perhaps centered on Italy, could put pressure on officials to activate the program. It would first require a country to ask for help and subscribe to reforms.

“If Weidmann gets the role and possibly has to use the OMT program, that’ll be difficult for him,” said Marc Bruetsch, chief economist at insurer Swiss Life. Meanwhile, “if he, as an opponent of the OMT program comes to the ECB and scraps OMT, then Draghi’s promise to do ‘whatever it takes’ is also essentially off the table.”

Helicopter Money

While the ECB’s crusade against feeble inflation in recent years has led it to enact a series of never-before-tested measures, the institution’s fight against deflation hasn’t yet reached the point of considering cash distributions to the public. That idea was once proposed by the Nobel prize-winning economist Milton Friedman.

“Were they to have to do something radical like helicopter money, that’s where the choice of the president would play an important role,” said Andrew Bosomworth, a money manager at Pimco. “Under some people this would be harder to implement than under others.”

Tightening

The ECB has committed to keeping rates on hold at rock bottom for the rest of this year, given a slowdown in global momentum and concerns about trade disputes and Brexit. There could always be an upside surprise, forcing the ECB to begin unwinding its extraordinary stimulus. That might be the easiest policy for Weidmann to implement, given his history.

“The signs are that from now on or from shortly onward, it will get better,” Holger Schmieding, chief economist at Berenberg, told Bloomberg Surveillance.

--With assistance from Carolynn Look and Jan Dahinten.

To contact the reporters on this story: Craig Stirling in Frankfurt at cstirling1@bloomberg.net;Catherine Bosley in Zurich at cbosley1@bloomberg.net

To contact the editors responsible for this story: Fergal O'Brien at fobrien@bloomberg.net, Jana Randow

©2019 Bloomberg L.P.