ECB Transformation of Europe Credit Hidden by Market Bounceback

ECB Transformation of Europe Credit Hidden by Market Bounceback

(Bloomberg) -- The European Central Bank’s purchase of almost 180 billion euros ($204 billion) of corporate bonds has upended the region’s credit markets, even if some fast-moving indicators are back to pre-intervention levels.

Metrics such as spreads and the number of negative-yielding bonds have largely returned to levels seen in early 2016, before the ECB announced plans to start buying corporate bonds under a wider stimulus program. Still, dig a little deeper and the program, which winds down at year-end, has fueled a boom in corporate borrowing as well as letting companies lock in years of low-cost financing.

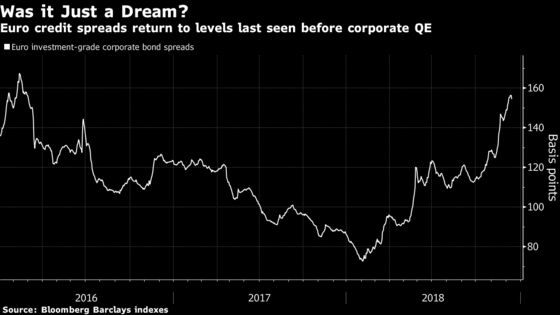

Spreads Unwind

Euro investment-grade spreads have returned to 2016 levels, reversing a slump that followed the ECB’s entrance into the market. The looming withdrawal of ECB support has fueled this year’s jump in risk premiums, along with political concerns such as Brexit and Italy’s election of a populist government.

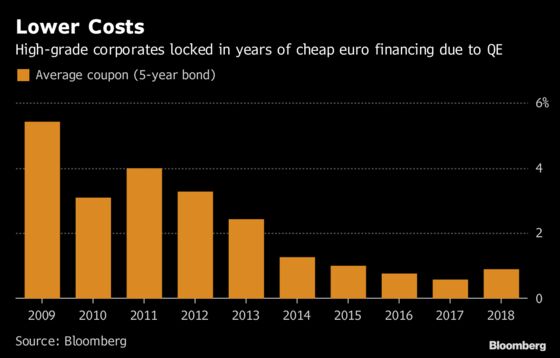

Locked-In Costs

Still, many companies that took advantage of ECB stimulus will reap the benefits for years as they were able to replace costly old debt with low-cost new bonds. The average coupon on a five-year investment-grade euro note sold last year was just 0.6 percent, less than half the level in 2014, according to data compiled by Bloomberg. The figure jumped in 2018 as credit markets tightened.

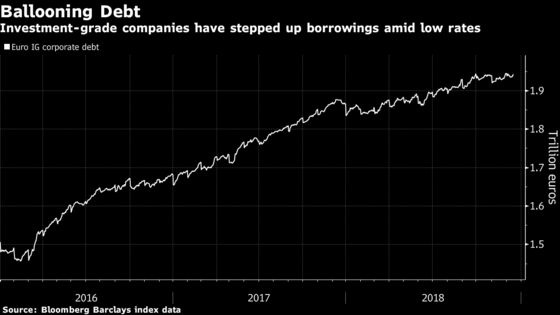

Borrowing Boom

Companies’ eagerness to lock in cheap financing produced one of the biggest changes caused by QE -- a surge in corporate debt. The outstanding pile of euro investment-grade debt has jumped to 1.94 trillion euros, up by more than 400 billion euros since March 9, 2016, the day before the ECB announcement, according to Bloomberg Barclays index data. That’s a possible win for Mario Draghi, as the ECB started buying corporate bonds partly as a way of encouraging companies to borrow and invest.

Tourists Depart

Low investment-grade debt yields sent high-grade investors into junk bonds to boost returns. This trend is now largely unwinding as a rebound in yields lures these tourist investors back to their traditional home. That’s evidenced in the spread between the lowest-rated investment-grade bonds and the highest-rated junk bonds reaching the widest since the summer of 2016 -- when the ECB started buying corporate debt.

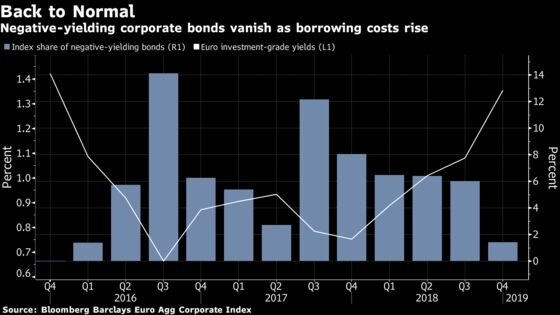

Less Negative

Wider spreads have also reduced the number of negative-yielding corporate bonds, which is back to the lowest since early 2016. The number of bonds that guaranteed losses if held to maturity jumped during the years of ECB stimulus, partly because the central bank was price-insensitive when buying notes.

To contact the reporters on this story: Tasos Vossos in London at tvossos@bloomberg.net;Neil Denslow in London at ndenslow@bloomberg.net

To contact the editors responsible for this story: Hannah Benjamin at hbenjamin1@bloomberg.net, Neil Denslow

©2018 Bloomberg L.P.