Sentiment Turning for Unloved British Stocks

Sentiment Turning for Unloved British Stocks

(Bloomberg) --

Now that U.S. President Donald Trump has completed his first official visit to the U.K., investors can start paying attention to the leadership contest heating up in Britain. The next prime minister is likely to be named in the coming weeks, while the final outcome of Brexit has become increasingly hard to anticipate. Although no-deal fears remain a massive overhang for U.K. stocks, the renewed uncertainty might play in favor of large caps.

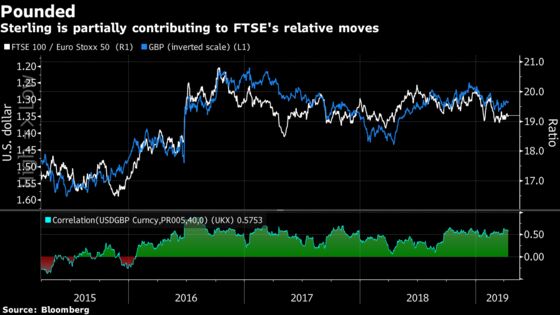

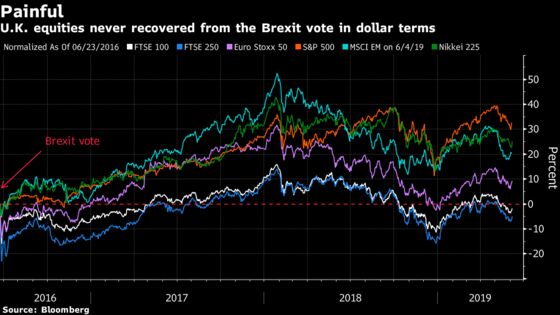

The FTSE 100 has underperformed most European markets this year, extending the lag that set in after the Brexit referendum three years ago. The move is particularly striking given the pound has weakened further, which would ordinarily boost the large-cap index. Barclays strategist Emmanuel Cau yesterday upgraded U.K. stocks to overweight versus euro-area equities provided currency is hedged, saying that Brexit uncertainty provides a cap to the pound for now. Large-caps on the U.K. gauge derive more than 70% of their revenue abroad, more than most European peers.

The FTSE 100 offers high-dividend yield, a bias toward material and energy stocks, and better earnings momentum. U.K. earnings estimates stopped falling back in March, whereas those in the euro zone are still falling, Cau wrote.

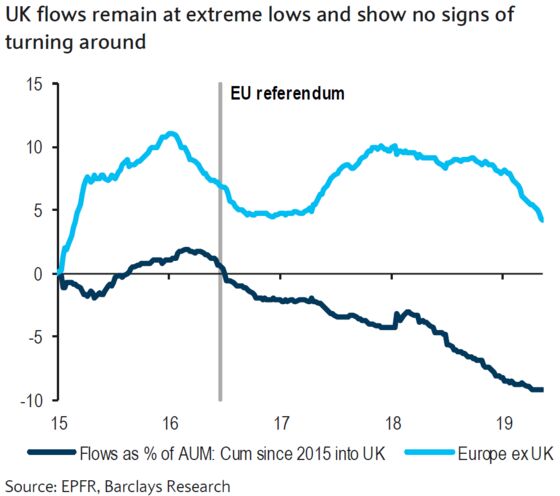

One problem is that British stocks have suffered from a consensus underweight for some time, with positioning standing at an extreme low and continuous outflows since 2016, according to EPFR data. For the tide to turn, they are in dire need of a catalyst.

“U.K. stocks are a huge opportunity for a longer-term investor,” according to Edmund Shing, BNP Paribas Equity Derivative Strategy Global Head. When everyone is pricing the worst, a small bit of good news is enough to trigger a change of behavior toward an asset. The catalyst could come sooner than people think, Shing tells me. It could be the avoidance of a general election, a moderate new leader, or simply the easing of trade tensions, as the FTSE has a high global trade exposure, he says. As for the avoidance of a no-deal Brexit, it would have a positive impact on investment and consumption. That’s for politics and macro.

Then there is micro: M&A could act as a huge boost, Shing says. Industrial buyers, particularly from the U.S., could use the cheap pound to finally trigger mega-mergers in the oil and gas sector or the pharmaceutical industry. The move could be accelerated if the pound starts to rise against the dollar, as industrial and private equity firms would then jump in to buy assets before they become more expensive. This could reignite the interest from investors into U.K. stocks.

Citi strategist Jonathan Stubbs agrees. “The gap between the cost of debt and equity funding is aggressively wide; the financing incentive to buy U.K. shares for activists, corporates and private equity has rarely been more extreme,” he writes in note.

There’s more. Stubbs writes the only time U.K. equities traded on a higher dividend yield relative to gilts in the last 100 years was World War 1. The free cash flows yield of U.K. stocks is above 7%, more than 150 basis points higher than all other regions.

Now, should any interest for the U.K. start to materialize, and the massively-underweight FTSE 100 starts to outperform a heavily overweight index such as the S&P 500, that could accelerate gains for the British gauge, Shing says. Well, the FTSE 100 is at an all-time low against the S&P 500.

In the meantime, FTSE 100 futures and Euro Stoxx 50 contracts are trading little changed ahead of the open.

SECTORS IN FOCUS TODAY:

- Watch carmakers after Fiat Chrysler pulled out of merger talks with Renault and after U.S. President Donald Trump said “not nearly enough” progress had been made in trade talks with Mexico.

- Watch for reaction to ECB’s tone, particularly banks, as traders are now betting on a cut in the next year, only months after a raise had been the consensus. The ECB will face a Europe where labor market slack is being underestimated and where there are mixed feelings about Japanification.

COMMENT:

- “Defensive sectors are some of the best and worst performers on our scorecard, while cyclicals are stuck in the middle, with either sound fundamentals but high valuation, or weaker growth but cheaper valuation,” write Bloomberg Intelligence strategists Laurent Douillet and Tim Craighead in a note. “With equity markets already pricing in looser monetary policy to come, only a resolution of the U.S.-China trade conflict would be likely to reshuffle the sector deadlock.”

COMPANY NEWS AND M&A:

- Fiat Walks Away From Renault Talks, Blaming French State (1)

- Fiat U.S. Sales Chief Sues Company in Whistle-Blower Lawsuit (2)

- Credit Agricole Boosts Profit Targets as Rivals Pare Back Goals

- Amundi Confirms Strategic Ambitions as Part of Crédit Agricole

- Heidelberger Druck Sees FY 2020 Profit on Par With Prior Year

- Remy Cointreau FY Current Op. Profit EU264m; Meets Margin Goal

- Scout24 Holder Singer Raises Stake to 7.49% Via Instruments

- BioMerieux Raises Stake in Hybiome to 67% for ~EU20m

- Boiron to Be Auditioned June 12 by Health Authority: Figaro

- Icade Commits to Sell Crystal Office Building for EU691M

- Deutsche Boerse Says Grenke to Join MDAX

- FTSE 100 to Include JD Sports Fashion, Aveva Group

NOTES FROM THE SELL SIDE:

- RBC cuts Beiersdorf to sector perform from outperform, saying the management team at has “done pretty much everything right” but the attractions of the stock are all baked in to share price.

TECHNICAL OUTLOOK for Stoxx 600 index:

- Resistance at 374.5 (61.8% Fibo); 382.3 (50-DMA)

- Support at 368.4 (200-DMA); 365.5 (50% Fibo)

- RSI: 44.5

TECHNICAL OUTLOOK for Euro Stoxx 50 index:

- Resistance at 3,405 (50-DMA); 3,514 (May high)

- Support at 3,309 (50% Fibo); 3,268 (200-DMA)

- RSI: 46.1

MAIN RESEARCH AND RATING CHANGES:

UPGRADES:

- GPE Groupe Pizzorno raised to buy at Midcap Partners

- ING Groep upgraded to overweight at JPMorgan; PT 12.50 Euros

- Immofinanz upgraded to hold at SocGen; PT 22 Euros

- Mitchells & Butlers upgraded to buy at Berenberg

- Norwegian Air upgraded to neutral at SpareBank; PT 35 Kroner

- Salvatore Ferragamo upgraded to hold at HSBC; PT 19 Euros

- Stobart upgraded to hold at HSBC; PT 1.17 Pounds

DOWNGRADES:

- Beiersdorf downgraded to sector perform at RBC; PT 105 Euros

- EI Group downgraded to hold at Berenberg

- Falck Renewables cut to reduce at Kepler Cheuvreux

- Liberbank downgraded to hold at Santander; PT 46 Cents

- Orange downgraded to equal-weight at Morgan Stanley; PT 17 Euros

INITIATIONS:

- Banco Santander reinstated overweight at Barclays; PT 5 Euros

- Paradox Interactive rated new hold at Berenberg; PT 140 Kronor

- Stobart rated new buy at Jefferies; PT 1.74 Pounds

- THQ Nordic rated new buy at Berenberg; PT 270 Kronor

MARKETS:

- MSCI Asia Pacific up 1%, Nikkei 225 down 0.1%

- S&P 500 up 0.8%, Dow up 0.8%, Nasdaq up 0.6%

- Euro up 0.09% at $1.1231

- Dollar Index down 0.08% at 97.24

- Yen up 0.34% at 108.09

- Brent up 0.1% at $60.7/bbl, WTI little changed at $51.7/bbl

- LME 3m Copper up 0.1% at $5810.5/MT

- Gold spot up 0.2% at $1332.8/oz

- US 10Yr yield down 3bps at 2.11%

MAIN MACRO DATA (all times CET):

- 9:30am: (GE) May Markit Germany Construction PMI, prior 53

- 11am: (EC) 1Q F Employment QoQ, prior 0.3%

- 11am: (EC) 1Q F Employment YoY, prior 1.3%

- 11am: (EC) 1Q Gross Fix Cap QoQ, est. 0.5%, prior 0.6%

- 11am: (EC) 1Q Govt Expend QoQ, est. 0.0%, prior 0.7%

- 11am: (EC) 1Q F GDP SA QoQ, est. 0.4%, prior 0.4%

- 11am: (EC) 1Q F GDP SA YoY, est. 1.2%, prior 1.2%

- 11am: (EC) 1Q Household Cons QoQ, est. 0.6%, prior 0.2%

To contact the reporter on this story: Michael Msika in London at mmsika4@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Namitha Jagadeesh

©2019 Bloomberg L.P.