Citigroup Team Goes Down Under for Its U.S. Election Risk Hedges

Citigroup Team Goes Down Under for Its U.S. Election Risk Hedges

(Bloomberg) -- The Australian dollar is the tool of choice to protect core investment positions since Treasuries and the greenback aren’t as effective risk-off hedges as they used to be, according to Citigroup Inc.

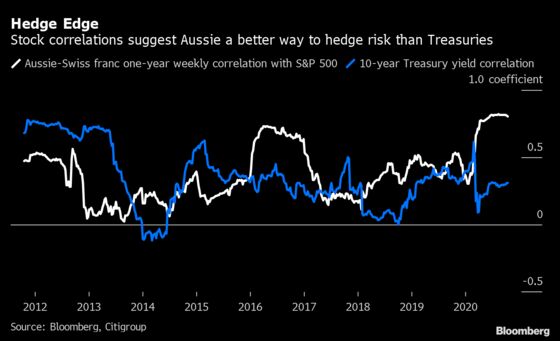

A look at the correlations between benchmark Treasury yields and U.S. stocks suggests Treasuries no longer have the sensitivity to equity selloffs they once did, while haven rallies in the dollar are “less potent,” strategists including Jeremy Hale wrote in a note Thursday. The Australian dollar -- especially against the Swiss franc -- has been much more correlated to stocks, leaving it better placed as an avenue to hedge against equity downside, they said.

“We still like to remain tactically positioned short Aussie-Swiss franc via puts as a hedge against our core positions,” the strategists wrote. “The Aussie is the most liquid outperformer in the FX majors since the equity market bottom, and thus looks vulnerable to risk aversion.”

The S&P 500 has climbed more than 55% since its March low, during which time the Australian dollar has strengthened almost 13% against its Swiss counterpart. The Aussie is seen as sensitive to global economic growth while the franc is a traditional haven.

The chance of a reversal in polls currently showing a strong lead for Democratic nominee Joe Biden, a possible “plateau” in economic data and a reluctance of Congress to pass fresh U.S. stimulus before the end of the year are all threats to risk assets, according to Citigroup.

©2020 Bloomberg L.P.