Caribbean Tax Havens Fret They’re at Risk from Global Crackdown

Caribbean Financial Sector at Risk From G-20 Corporate Tax Plan

(Bloomberg) -- Sign up for the New Economy Daily newsletter, follow us @economics and subscribe to our podcast.

The Caribbean will take years to recover from the global pandemic that wiped out tourism, its prime economic engine. Now a new storm threatens its offshore financial sector.

As some of the world’s largest economies mull plans to adopt a global minimum corporate tax, few places may suffer as much as the palm-fringed tax havens in the Caribbean.

With scant natural resources or big industry, much of the region’s economy depends on luring international business with rock-bottom rates. Anguilla, the Cayman Islands, Bahamas, Bermuda, the British Virgin Islands, and Turks and Caicos charge no corporate income tax. Places like Puerto Rico, and Barbados have rates low enough to make them attractive.

Companies have some discretion over where they declare profits, especially from patents, brands and other intangible assets, and can slash their tax bills by moving revenues to subsidiaries in tax havens. The Group of 20 nations, or G-20, wants to crack down on this.

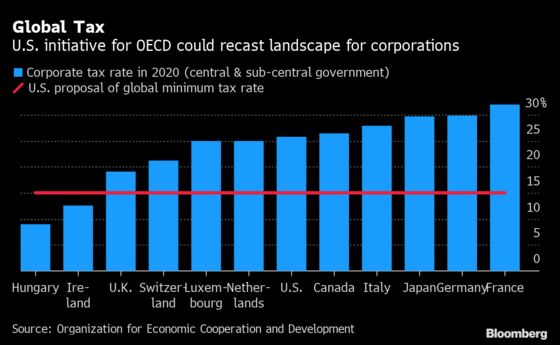

Details are still being hammered out, but negotiators are considering requiring corporations pay a 15% tax regardless of where they’re incorporated. So a German company paying 0% in Bermuda would still owe an additional 15% back home.

That would undermine the incentive for global companies to set up shop on storm-prone islands in the Caribbean, said Bruce Zagaris, an international tax lawyer in Washington, and a member of the Caribbean Policy Consortium.

The economic impact to the region “will be very substantial,” he said, “especially when they are coming out of the pandemic and their main sector, tourism, has been battered.”

The International Monetary Fund says the economy of the Caribbean won’t return to pre-Covid levels until 2025 -- later than most regions -- due to the “much slower than anticipated” recovery of travel and tourism.

Microsoft, Shell

Many of the loopholes that made the Caribbean synonymous with tax shelters have been shut in recent years. Even so, oil giant Royal Dutch Shell Plc. booked $21.5 billion in revenue through Bahamas in 2019, and $848 million in profit, on which it paid no tax, according to the company’s annual report. And in May, the Irish Times reported that a Dublin-based subsidiary of Microsoft Corp. used its Bermuda “tax residence” to book $314 billion in tax-free profit.

Microsoft said in reply to written questions that its organizational and tax structure “reflects our complex global business” and that it is “fully compliant with all local laws and regulations in the countries where we operate.”

The global tax plan still requires approval by the G-20 and members of the Organisation for Economic Co-operation and Development, another international forum of countries. And it may leave some jurisdictions relatively unscathed.

Cayman Islands

The Cayman Islands is home to some 100,000 corporations, and the financial sector that supports them represents about half the economy.

But the bulk of those corporations are considered regulated financial services -- including banks, investment vehicles and hedge funds -- that may be exempt under the global tax deal, though the details of exemptions are still being negotiated.

A global minimum tax “will not significantly impact Cayman’s leadership position,” said Jude Scott, the CEO of Cayman Finance, the association of financial service providers.

Even if the Caymans is unaffected by the G-20 plans, Zagaris says they and other zero-tax jurisdictions remain under intense scrutiny from global policy makers “who are trying to put them all out of business.”

Puerto Rico

Puerto Rico -- a U.S. territory of 3.3 million people -- has a notoriously feeble electrical grid and has been battered by hurricanes and earthquakes. Yet, thanks to its low corporate tax rates, it’s favored by pharmaceutical and aerospace companies. Manufacturing represents about 50% of the island’s economy and 35% of local-government revenue.

Puerto Rico’s Secretary of Economic Development Manuel Cidre said a global minimum tax “would obviously be detrimental to Puerto Rico and other jurisdictions,” but it wouldn’t end competition for investment.

Cidre said the island would likely raise its rates to match the global minimum and then use the additional revenue to provide corporations other kinds of breaks.

“It wouldn’t surprise me if Puerto Rico and other jurisdictions created incentives that target labor, energy, or other areas that would be enough to compensate for what was lost,” he said.

Some see the tax plan as a threat to national sovereignty. Caribbean Community General Secretary Irwin LaRocque told local television that wealthy nations shouldn’t be imposing their tax policy on the Caribbean.

Low taxes, he said, are one of the few ways the Caribbean can attract foreign investment -- crucial after the region loaded up on debt to confront the pandemic. Thirteen Caribbean nations now have debt-to-GDP ratios of more than 60%, and Barbados, Belize, Dominica and Suriname all have debt ratios that exceed 100%, according to the Caribbean Development Bank.

“We cannot grow ourselves out of our debt trap that we are in,” LaRocque said. “You need to have foreign investment coming in. Without foreign investment we’re not going to make it.”

©2021 Bloomberg L.P.