Argentina Returns to Capital Controls as Macri Fights to Survive

Capital Controls Return to Argentina as Macri Fights to Survive

(Bloomberg) -- Argentines and investors alike are cautiously assessing the impact of President Mauricio Macri’s decision to impose capital controls on Sunday -- a blunt policy reversal aimed at containing the country’s escalating financial crisis.

Argentina’s Eurobonds fell, while the peso strengthened slightly in the first few hours of trading after the central bank’s announcement. While market analysts appeared skeptical the latest measure would be enough to prevent further capital flight, in Buenos Aires there was little sign of unease among ordinary savers. “Argentina’s financial system is solid,” Central Bank president Guido Sandleris said in a press conference on Monday evening.

A day earlier the bank had ordered exporters to repatriate foreign currency from the sale of their goods within five days, among other measures. Corporations now require the authorization of the bank to buy dollars in the foreign-exchange market, except in cases of international trade. Individual Argentines, meanwhile, are limited to dollar purchases of no more than $10,000 a month.

The move represents a bitter irony for the pro-market president, who set about dismantling capital controls as soon as he took office in 2015. Amid rising public panic and the looming specter of default, Macri is trying to stanch the hemorrhaging of dollars from the country by ripping up his orthodox economic playbook, reintroducing the kind of interventionist policies he once excoriated.

With presidential elections eight weeks away, Macri trails former cabinet chief Alberto Fernandez by a seemingly insurmountable distance. While the latest measures are unlikely to turn the tide, they may help Macri become the first non-Peronist president to finish his constitutional term in recent Argentine history. The knee-jerk reaction by investors was to dump more of the nation’s assets, as seen in a plunge in euro-denominated bonds due 2022.

“There’s a phenomenal crisis of confidence in the economy, and the government is trying to patch up the effects of this crisis with the controls,” Fausto Spotorno, economist and director of the Orlando Ferreres & Asociados consultancy in Buenos Aires, said. “We still don’t know if these patches will work.”

In a note published later on Sunday, the International Monetary Fund described the move as “capital flow management” and stated that it would “continue to stand with Argentina during these challenging times.” Last week the Macri administration announced plans to renegotiate payments on $44 billion it has borrowed from the IMF.

Speaking on local TV late on Sunday evening, Economy Minister Hernan Lacunza said that though the measures might be uncomfortable they would avoid worse outcomes. “Argentina is like a boat stuck in circles, always returning to the same port. This isn’t the port we dreamed of,” he said. “Now the challenge is to dock the boat on the pier on the 10 December.” That date is when Macri’s mandate ends.

Macri’s vice-presidential candidate Miguel Angel Pichetto also told local media that the government had taken the decision to ensure that volatility and short-term lack of liquidity did not impact Argentines. “When the dollar rises, supermarket prices go up,” he said.

The campaign has taken a backseat role as the government focuses on reassuring Argentines, according to an official from the presidency who declined to speak on record. While it’s worse to campaign with currency controls in place, it’s even worse with the exchange rate spiraling out of control, the person added.

Deepening Crisis

Sunday’s move shows how the crisis has moved beyond international bond investors to affect ordinary Argentines, who may choose to save in dollar bank accounts.

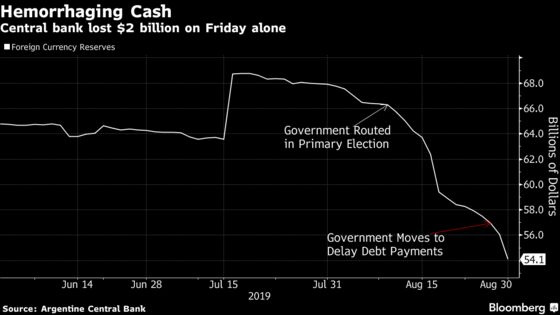

In the aftermath of the Aug. 11 primary elections that showed Fernandez on course for victory in October, Argentine depositors withdrew hundreds of millions of dollars from their accounts -- cash the central bank counts as part of its gross foreign reserves. These withdrawals, coupled with policy makers’ sale of dollars to shore up the peso, has led to a dramatic fall in the country’s stock of reserves.

Around $3 billion drained out of the foreign-currency reserves on Thursday and Friday alone after the government changed the terms for its short-term debt. The country risks exhausting its net reserves, which stand at under $15 billion, within weeks if it keeps losing money at this pace.

The return of populism in Argentina is scaring the “dickens out of emerging-market investors,” said Stephen Innes, an Asia-Pacific market strategist at AxiTrader in Bangkok. Bonds due 2022 declined about 6 cents on the euro to 35.31, according to prices compiled by Bloomberg.

Read More: Argentina Capital Controls Unlikely to Halt Peso Drop: Analysts

Currency Collapse

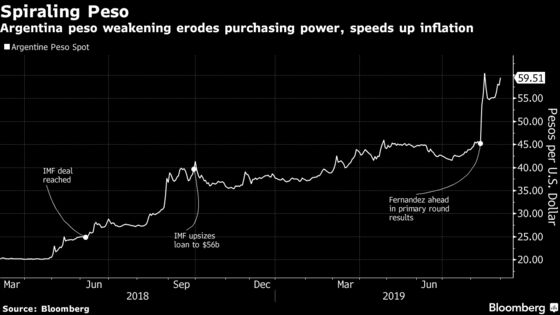

The peso depreciated more than 25% last month after primary election results showed the market-friendly government has little chance of retaining power. Interest rates soared as the central bank tried to roll over debt, culminating Wednesday in a decision to delay payments on $7 billion of bills coming due this year.

Opposition advisers had called for currency controls. Fernandez himself said the government was in “virtual default” but added that he was unwilling to support the emergency measures designed to control rising volatility. Total central bank reserves have slumped to $54.1 billion, from $66.4 billion the day before primary.

As well as pushing back maturities on local short-term debt on Aug. 28, Argentina also said it will ask holders of $50 billion of longer-term debt to accept a “voluntary re-profiling.”

Fitch Ratings now classifies Argentine debt as RD, or restricted default; Standard and Poor’s as CCC-; and Moody’s as Caa2. Credit default swaps are pricing in a more than 90% chance of a fully-fledged default within five years.

For Juan Diaz Cruz, the director of political risk advisory firm Cefeidas, the economy minister and the central bank will have to adopt further measures in the days to come.

“Today the objective seems to be to contain the economic and financial deterioration,” he said. “To generate greater credibility in the ability of the government to make it to the elections at least minimally competitive.”

--With assistance from Jonathan Gilbert.

To contact the reporters on this story: Jorgelina do Rosario in Buenos Aires at jdorosario@bloomberg.net;Philip Sanders in Santiago at psanders@bloomberg.net

To contact the editors responsible for this story: Juan Pablo Spinetto at jspinetto@bloomberg.net, Bruce Douglas, Carolina Millan

©2019 Bloomberg L.P.