MMT Has a Big Hurdle to Overcome to Succeed in Europe

MMT Has a Big Hurdle to Overcome to Succeed in Europe

(Bloomberg) --

In Europe, by and large, the countries that want to spend more money can’t –- and the ones that can, won’t.

That’s a huge hurdle for Modern Monetary Theory, the emerging school of thought that says governments should use their budgets to steer economies.

Not Sovereign

The core idea of MMT is that governments with their own currencies can spend without worrying about going broke (the real constraint is inflation).

That doesn’t apply to the euro’s 19 member nations though. Lacking their own currencies, none of them has that kind of sovereignty, and so monetary and fiscal policy are firmly separated.

Interest rates are set by the European Central Bank for the entire region, while budgets are managed by member states. They’re supposed to stay within strict limits set by the European Union, and can’t print euros to cover deficits.

“The chartalist dimension, the fact a currency is issued by a state, is not fully present in the EU,” says economic historian Emmanuel Mourlon-Druol from the University of Glasgow. “It is in the U.S. Hence, perhaps, the difference in the debate about MMT.”

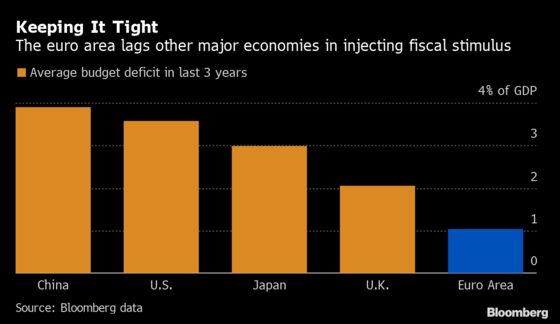

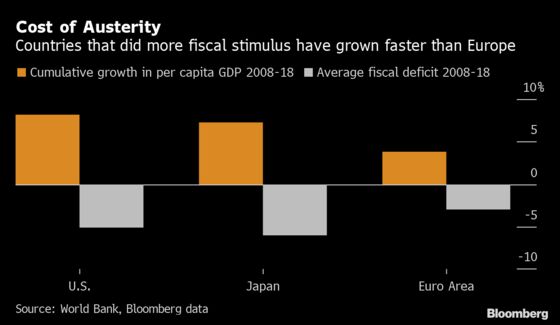

There’s also been a divergence in economic performance. Budget deficits helped the U.S. (and Japan) recover faster after 2008, while Europe focused on austerity to cut debt.

Target: Germany

The calls for fiscal stimulus are getting louder because a decade of unconventional monetary policy might have exhausted the ability of the ECB -- whose benchmark interest rate is already below zero -- to respond to shocks.

The bank’s current president, Mario Draghi, and his designated successor, Christine Lagarde, have both urged governments to help out with more spending. They don’t explicitly say so, but their main target is Germany.

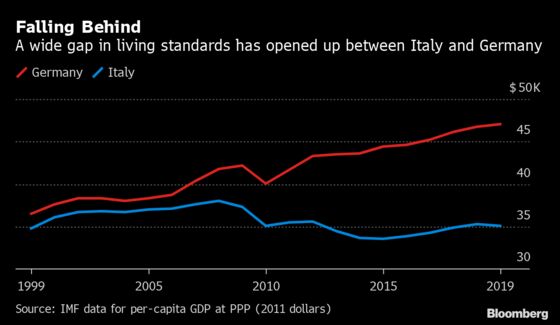

Europe’s economic powerhouse has run budget surpluses for the past five years, and despite a slowdown in growth, crumbling infrastructure, and waning support for mainstream politicians, has shown little enthusiasm for loosening the purse strings.

By contrast, Italy –- whose economy has been stagnant since it joined the euro -– has pushed up against EU budget limits, and clashed with the rule-enforcers in Brussels.

‘Stateless Currency’

MMTers -- along with many conventional economists -- have criticized the set-up of the euro area since its inception. Randall Wray, a leading MMT scholar, wrote in his 1998 book “Understanding Modern Money” that countries effectively agreed to “operate fiscal policy in a foreign currency” when they joined the euro.

It’s not surprising, then, that many MMT economists say the monetary union is fatally flawed and should be disbanded.

Dirk Ehnts, a rare German economist who’s also an MMT enthusiast, disagrees. Ehnts, who wrote one of the first textbooks based on the new theory, says a better way forward would be a continent-wide Treasury to balance the central bank and solve the problem of a “stateless currency.”

The ECB itself backs the idea of a “fiscal capacity” and the idea has plenty of history. But the practical challenge is daunting, and there’s little public appetite for closer integration.

Yet Europe demonstrated its ability to act flexibly in 2012 when Draghi promised to do “whatever it takes” to save the euro, a step that effectively put a backstop behind government debt. Many observers hope that Lagarde, who’ll take over in November, will encourage a fiscal rethink.

‘We Can Win’

“In a perfect world, she should put a lot of pressure on politicians to increase spending,” says Ehnts. “The central bank isn’t supposed to educate the government about macroeconomic policy. But I think in this case it can’t be avoided.”

Ehnts describes conversations with a wide range of German economists from academia, business and the Bundesbank -- where he says young staffers tend to grasp MMT thinking better than most professors.

He points out that Peter Bofinger, one of Germany’s best-known economists and a former government adviser, recently addressed the topic of whether central banks can directly finance government deficits. The question, he concluded, “should not be if but how much?”

Germany has “a lot of respect for intellectual ideas,” Ehnts says. “I hope, and think, that we can win.”

A debate in Hamburg next month, featuring heavyweights from both camps, may be one place to keep score.

Due to appear in one corner: Stephanie Kelton, the highest-profile MMT economist. And in the other: Jens Weidmann, head of what may be the world’s least MMT-friendly institution, the Bundesbank.

To contact the reporter on this story: Carolynn Look in Frankfurt at clook4@bloomberg.net

To contact the editors responsible for this story: Paul Gordon at pgordon6@bloomberg.net, Ben Holland, Jana Randow

©2019 Bloomberg L.P.