Bond Traders Start Panic Buying in New Yield Order

Bond Traders Start Panic Buying in New Yield Order

(Bloomberg Opinion) -- Why are U.S. Treasury yields so low?

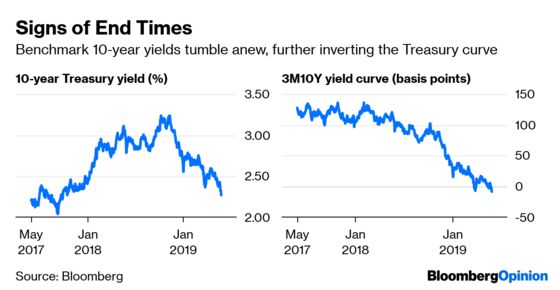

This is probably the single most pressing question facing Wall Street after the benchmark 10-year yield touched 2.26% on Tuesday, down about 100 basis points from October. Because of that rally, a key portion of the U.S. curve inverted further. Yes, there’s a U.S.-China trade war going on. But those levels still boggle the mind when considering the S&P 500 Index remains close to a record, the Federal Reserve has said it’ll be patient with interest rates and Americans feel as good about current economic conditions as they have in 18 years.

So, how to justify these yields? Bloomberg News’s Cameron Crise says it’s worth remembering that the bond market isn’t infallible, even given the yield curve’s strong track record, while Richard K. Breslow feels the move makes investors wonder whether something is seriously wrong in the world. BMO Capital Markets strategists noted that the Fed’s 2.25% to 2.5% target range for short-term rates clearly “isn’t the inhibition it once was,” which “offers context for just how willing investors are to price in an easing campaign of sorts in the upcoming 24 months.”

Here’s a thought: Perhaps bond traders realize that the endgame is a world in which yields must be lower for longer. And there’s enough potential bad news now that they’re panic buying rather than waiting for a fleeting uptick in rates that may never come.

To be clear, this rush to Treasuries might be a bit too early, and the world’s biggest bond market could very well be stuck in a range for the next few months. Part of the rally can be traced to Germany, where 10-year yields are -0.17% and close to a record low. All the while, it’s impossible to rule out a U.S.-China trade deal coming together, even though President Donald Trump said he wasn’t ready just yet.

In terms of the bigger picture, though, and to BMO’s point, can anyone say with conviction that buying a 10-year note at 2.26% is an outright bad long-term investment? Sure, there may be somewhat better opportunities, but absent a surprise surge in inflation, it’s hard to see 10-year yields climbing back to 3% this cycle. By contrast, it’s easier to envision the Fed cutting rates in the near future and causing the entire Treasury curve to lurch lower in anticipation of further easing. That might be why a measure called the term premium just reached its lowest level on record — investors simply see minuscule risk in owning longer-dated securities.

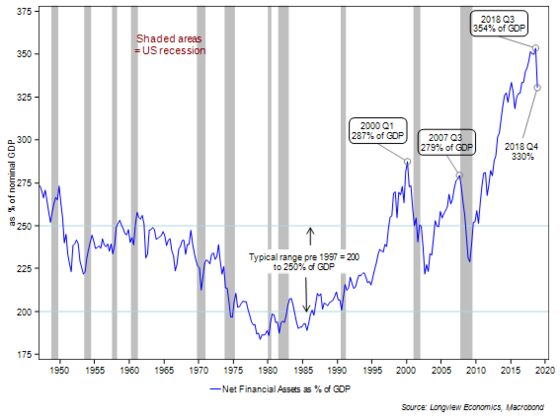

I wrote in early April that the huge increase in global debt over the past decade has most likely capped how high U.S. yields can climb before causing serious damage to U.S. companies and the economy. The importance of lower-for-longer interest rates is even clearer after observing this chart from Longview Economics, spotted by my Bloomberg Opinion colleague John Authers:

Basically, cheap money has made Americans as a whole “wealthy,” at least on paper. Higher interest rates threaten that. If U.S. consumers no longer feel confident about their financial position, say, because a sharp drop in equities cuts into their retirement savings, that shows up in the real economy and government data. In turn, Treasury yields fall. Some investors called this feedback loop a “tug of war” in recent years, but truly, the outcome was hardly ever in doubt. No one has any incentive to push yields higher and higher and see what happens. That scenario played out late last year, and it wasn’t pretty.

If this feels like a dangerous game, that’s because it kind of is. The U.S. economy has become increasingly “financialized” over the past two decades, as seen in the previous chart, while the federal government and American companies have taken on massive debt loads. There’s no unwinding that. The only way to possibly avoid serious pain is to keep interest rates in check, which supports stock valuations and gives businesses the chance to borrow on the cheap or refinance their existing obligations. It’s not as if this is some sort of silver bullet — just see how negative rates are working for Europe and Japan — but lower yields at least push off any sort of reckoning.

JPMorgan Chase & Co. Chief Executive Officer Jamie Dimon had this to say about credit losses across the bank’s products on Tuesday, though it could be applied similarly to markets: “On average, things will get worse over time, not because they’re going to get bad, but because it’s been so good for so long.” Along the same lines, some strategists noted that lofty consumer confidence numbers have historically signaled an economic peak. The yield curve, of course, is sending a similar message.

The most surefire way to prevent things from becoming truly “bad,” at least imminently, is to keep interest rates low and the cheap money flowing. The Fed knows this, as reluctant as officials may be to acknowledge it. Bond traders know the Fed knows this. That’s probably why they’re willing to buy 30-year bonds at a yield less than real economic growth, or five-year Treasuries at a yield that may soon be less than 2%.

Perhaps traders sensed a chink in the Fed’s armor when James Bullard said last week that policy makers “may have slightly overdone it with our December rate hike.” No matter the exact reason, it’s becoming increasingly clear that markets have decided yields need to be lower. This was always the endgame for Treasuries, though few expected it to come so soon. The question now is whether risky assets will falter or flourish with cheaper money back on the table.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2019 Bloomberg L.P.