Greek Bonds Emerge From the Fire of 2011 Stronger Than Ever

Bond Investors Crying Out for Yield Are Finding Riches in Greece

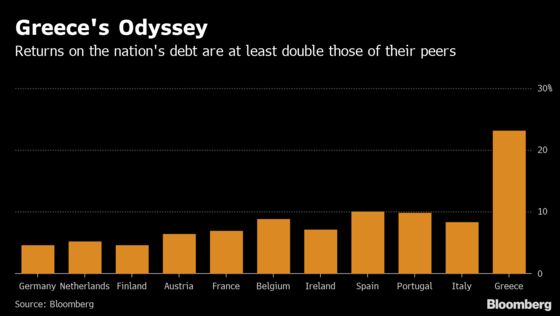

(Bloomberg) -- In all the market milestones breached in recent weeks, the performance of Europe’s most-indebted nation has been remarkable.

Greek bonds have returned over 20% this year to those willing to take the risk of holding the junk-rated and illiquid debt, the best in the euro area. And Athens stocks are world beaters. The rally may have room to run as this weekend’s elections look set to to bring a more market-friendly government to power, and beyond that there’s the prospect of European Central Bank stimulus.

“The Greek economy has turned the corner and elections could pave the way for a more pro-reform government,” said Alberto Gallo, a money manager in London at Algebris Investments, which favors bonds maturing in five years or longer.

Investors are no longer just confined to those who specialize in distressed debt. More conventional funds are either betting on the Greek recovery from years of crisis, or are just hungry for anything that has a positive rate as more and more of Europe’s bonds join a record global pile of negative-yielding debt.

Post-Crisis Caution

Fund manager Charles Diebel is not joining the rush. He spent some time in Athens during Greece’s financial crisis and it was enough to stop him ever buying the country’s bonds.

“Yield is yield,” said Diebel, the Ireland-based head of fixed income at Mediolanum S.p.A. “But I was in Athens during the crisis and stayed in the same hotel as European Union members of the troika -- talking to them put me off forever.”

The troika was used to describe the trio of institutions -- the European Commission, European Central Bank and the International Monetary Fund -- that imposed stringent austerity on Greece in return for bailouts.

At the height of the euro-area financial crisis, yields sky-rocketed amid fears that the Mediterranean nation would become bankrupt and tumble out of the EU. General strikes paralyzed central Athens and crowds of thousands clashed with police in 2011, in protests against austerity measures. The country has had to rely on about 300 billion euros ($338 billion) in foreign aid since 2010.

Those days now seem far away for many. Ten-year yields are hovering at record lows around 2%, compared with a crisis high of 44%. Greece’s stock of debt currently amounts to around 180% of economic output, compared with 132% in Italy.

After ending its bailout program last summer, Greece tapped the market for 2.5 billion euros of five-year bonds in January. The success of that sale paved the way for a syndication in March of 10-year debt for the first time in nine years.

Political Change

Now, center-right party New Democracy is topping the polls ahead of Sunday’s election and is expected to garner nearly 40% of the vote. Prime Minister Alexis Tsipras’ Syriza party is trailing, with support at around 28%.

Bank of America Merrill Lynch forecasts economic growth of around 2% this year and in 2020, and recommends that investors position for Greek bonds to rally further relative to their German peers.

“We would expect a New Democracy government to be more positive for markets than a government coalition,” wrote Bank of America strategists led by Ruben Segura-Cayuela. “We see more potential ahead as the search for yield extends.”

Even though Greece is not currently eligible for the ECB’s asset-purchase program, given its junk status, the prospect of further quantitative easing is another potential boon. Since IMF Chairman Christine Lagarde is lined up to succeed Mario Draghi as ECB President, that makes it more likely Greece could join in coming years, according to Diebel.

“Lagarde is a pragmatic dove,” he said. “That rule can easily be amended.”

--With assistance from Tanvir Sandhu, Ksenia Galouchko and Vassilis Karamanis.

To contact the reporter on this story: John Ainger in London at jainger@bloomberg.net

To contact the editors responsible for this story: Ven Ram at vram1@bloomberg.net, Neil Chatterjee, Anil Varma

©2019 Bloomberg L.P.