Bond Buyers Back Italy on Hope Political Risks Are Just Noise

Bond Buyers Back Italy on Hope Political Risks Are Just Noise

(Bloomberg) -- The euro area’s highest investment-grade bond yields are simply too good to pass for some investors even as another round of dust-up between Italy and European Union looms large this week.

M&G Investments is dipping back into Italian short-dated debt, while BlueBay Asset Management LLP has a long position in the securities known as BTPs. The near doubling of yields since the start of the year has also tempted retail investors back into the market, who tend to hold the bonds until maturity, according to the nation’s debt agency head Davide Iacovoni.

That’s despite an ongoing standoff with the EU, which saw the bloc dismiss Rome’s budget targets as overly optimistic. While Italy has until Tuesday to submit a revised version of its spending plans, the government has signaled it won’t bow to pressure from Brussels.

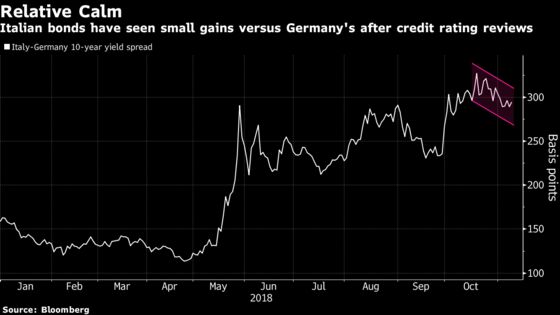

A pullback in Italy’s yield premium over Germany suggests the market is soft-pedaling the risk of populist politics in Rome destabilizing the EU, not least because similar fears have already played out from France to Greece in recent years with little long-term consequence. Past episodes of euro-breakup anxiety were typically resolved by last-minute compromises, and that may be fueling market expectations for a similar outcome to the ongoing Italian imbroglio.

While there’s no sign yet of an end to tensions with the bloc, that still doesn’t justify yields as high as they are, according to BlueBay.

“It’s been quite a rough and at times painful ride, but we still do think that we have the mispricing of Italian EU-exit risk,” David Riley, chief investment office at BlueBay, told Bloomberg TV last week.

‘More Attractive’

Investors are also looking to take advantage of a rare period of stability in Italian bonds, which have been rocked this year after euroskeptic political parties rose to power. S&P Global Ratings and Moody’s Investors Service both stopped short of downgrading the nation to junk last month, supporting investor confidence for the time being.

Wolfgang Bauer, who co-manages the M&G Absolute Return Bond Fund for the U.K. investment house that oversees 286 billion pounds ($368 billion), sold most of his Italian bond holdings in February and March this year and has only just started to re-enter the market. His colleague Richard Woolnough has recently invested 1 percent of his M&G Optimal Income Fund portfolio in short-term BTPs after exiting peripheral euro-area debt in May.

“The risk-reward profile is now more attractive,” Bauer said at a presentation in Milan, Italy. “Even in the worst case scenario -- a euro exit -- it’s very unlikely that will be done in two years.”

Rising Costs

Italian 10-year bond yields rose one basis point to 3.41 percent Monday, little changed this month. That compares with similar rates of 0.39 percent in Germany, 0.77 percent in France, 0.12 percent in Japan and 1.45 percent in the U.K. The spread over bunds was 302 basis points, down from as wide as 341 basis points on Oct. 19. Still, the gap has almost doubled from the end of last year.

This year’s surge in yields is boosting borrowing costs for Italy, one of euro zone’s most indebted economies. Debt-funding expenses for next year will rise by about 5 billion euros compared with the end of 2017, based on the seven-year weighted average maturity of its debt and the 175 basis point increase in seven-year yields in the secondary market this year.

Italy will auction bonds maturing in 2021, 2025 and 2038 Tuesday as well.

‘Big Problem’

Other investors are still more skeptical. OppenheimerFunds Inc. money manager Alessio de Longis is positioning for European political risk by buying the Japanese yen versus the euro. Alongside Italy, he cited the withdrawal of European Central Bank stimulus and slowing economic growth in the region as other reasons to be bearish.

“This is a way we are expressing euro-specific discomfort with respect to some of the developments that could occur with Italy,” said de Longis, who helps oversee $2 billion in New York. He is targeting 124 yen per euro, from around 130 currently. “Italy is a big problem - that is not going to go away.”

While Italian bonds may seen more volatility due to simmering Rome-Brussels tensions, both sides are eventually likely to reach a compromise in the longer run, according to HSBC Holdings Plc.

Further disagreement between the two sides is already “widely expected” by the market and there is still scope for improvement in sentiment toward Italian bonds, according to Mizuho International Plc.

“We’re not expecting much of a sell-off in BTPs beyond a short term ‘knee-jerk’ reaction,” strategists Peter Chatwell and Antoine Bouvet wrote in a note to clients last week. They recommended buying five-year bonds versus their two- and eight-year peers.

--With assistance from Liz Capo McCormick, Francine Lacqua and David Powell (Economist).

To contact the reporters on this story: John Ainger in London at jainger@bloomberg.net;Marco Bertacche in Milan at mbertacche@bloomberg.net

To contact the editors responsible for this story: Ven Ram at vram1@bloomberg.net, Anil Varma, Keith Jenkins

©2018 Bloomberg L.P.