Biden’s Stimulus Risks Giving Money to People Who Won’t Spend It

Biden’s Stimulus Risks Giving Money to People Who Won’t Spend It

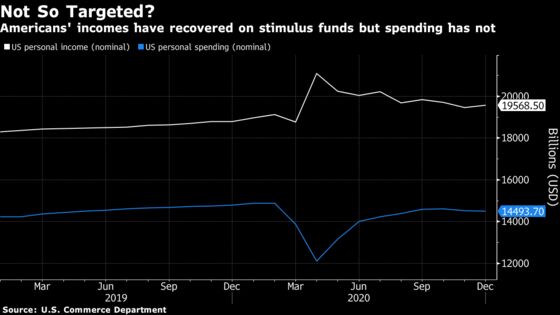

(Bloomberg) -- President Joe Biden faces an economic dilemma as his $1.9 trillion stimulus plan runs into congressional opposition: keep his promise to deliver $2,000 payments to help a battered economy, or target funds to jobless and low-income Americans.

Biden said this week he’s open to discussing more-targeted payments after some key Republicans and Democrats raised concerns that funds may go to people who don’t need them. Households in greater need are much more likely to spend the money immediately, giving the economy a quicker boost than if the payments were used to boost savings or pay down debt.

The administration has proposed sending $1,400 checks to individuals hard-hit by the pandemic and Biden signaled he’s open to negotiating on eligibility. The previous round of $600 checks in December sent funds to individuals earning up to $75,000, or $150,000 for a household.

While a wide body of research shows that direct payments help boost economic growth, two recent studies indicate the previous income threshold might be too high to promote the most spending for the cost. Also, policy makers want consumers to stay home and limit the spread of the coronavirus, rather than spend on things like dining out and travel.

At the same time, targeting checks could miss some households in genuine distress.

“The question that should be forefront in people’s minds in crafting this stimulus package is: Are we still in a position where the economy needs to stay shut down until the vaccines have rolled out, or are we trying to stimulate the economy now?” said Jonathan Parker, a finance professor at the MIT Sloan School of Management who’s researched government stimulus for more than two decades. “I think it’s still the former.”

Biggest Boost

That argues for targeting the lowest-income people by beefing up unemployment benefits and the food-stamps program, while providing a more robust earned-income tax credit, according to Parker. Stimulus payments would be beneficial to boost growth if spending still hasn’t returned following widespread vaccinations, he said.

Brookings Institution researchers, in a report Thursday analyzing Biden’s stimulus plan, said aid to financially vulnerable households provides the biggest boost to gross domestic product.

In a December report, the JPMorgan Chase Institute examined 1.8 million of the bank’s customer checking accounts, often the first place households receive and spend funds. Researchers found that the lowest-income earners had the biggest gains and also the fastest depletion.

Top earners, or households making more than about $68,800, held assets and built on them. In other words, the poorest Americans were more likely to spend their checks.

Save or Spend

Recent data from Opportunity Insights, a non-profit group spearheaded by Harvard University professor Raj Chetty, showed a similar finding for the December 2020 stimulus payments. Chetty’s team found that households earning below $46,000 increased spending 7.9% in a two-week period following the stimulus bill passing, compared to just 0.2% for those making above $78,000.

Surveys are mixed on whether people would spend immediately. When the Federal Reserve Bank of New York in December asked what people would do with an unexpected 10% income boost, only 19% said they’d spend or donate, while the rest said they’d save, invest or pay down debt. Meanwhile, a Bureau of Labor Statistics survey in August showed that most people would spend stimulus payments and two-thirds of people would use it for food, indicating the checks are going to the most vulnerable.

Claudia Sahm, an economist who studied the impact of financial-crisis stimulus payments at the Federal Reserve, said a major issue with narrowing the checks is that the government doesn’t have all the necessary information. People who have just lost their job or seen a pay cut might not qualify because their circumstances changed too recently to meet the eligibility qualifications.

And some higher earners may still be living paycheck-to-paycheck with limited savings. So while recipients may use the funds to pay down debt rather than save, the net effect is still to put those people in a better financial position, something economists refer to as “financial resilience” and important to the broader economy in times of stress.

“If you want to get the biggest bang for the buck, you would want to give it to people who have low balances in their bank accounts -- but the federal government doesn’t have that information,” said Sahm, who’s found automatic stimulus payments and one-time checks are beneficial. “If you get too fancy with targeting, you’re going to miss people who really are in need.”

©2021 Bloomberg L.P.