Barclays Credit Strategists Warn on Nonchalance Over Le Pin Win

Barclays Credit Strategists Warn on Nonchalance Over Le Pin Win

(Bloomberg) -- Corporate bond investors shouldn’t get too blasé about the risk that nationalist candidate Marine Le Pen becomes France’s next president, an outcome that could trigger doubts about the European Union’s future, Barclays Plc strategists cautioned.

“Markets appear unconcerned and no meaningful premium has been priced into French credit thus far,” strategist Zoso Davies and credit research analysts wrote in a note on Wednesday. “This suggests risks are skewed to the downside should Le Pen be victorious.”

Up to now, French bank bonds have held their ground against the general index as they did in the previous election five years ago, while their premium versus foreign peers has remained steady compared to the spike seen ahead of the 2017 vote, according to Barclays.

That’s setting the stage for a losses-only scenario, with victory for incumbent Emmanuel Macron just maintaining the status quo in credit, while a Le Pen upset would spark sudden declines, the analysts wrote. It also adds to warnings that markets are underestimating the risk of a shock result that could, in an extreme scenario, raise major concerns about the whole euro project.

All the polls at the moment show Macron remains the front-runner to win a second term in Sunday’s vote.

Even so, “it would only take one poll indicating a tighter race to trigger an underperformance of French credits,” the Barclays analysts wrote. “Given the lack of any risk premium in these credits, we remain wary.”

Calm Market

Le Pen has toned down policies that spooked debt investors going in to the last elections in 2017.

But while she no longer seeks an exit from the EU, she’s still calling for a referendum on changing the constitution to make French law superior to the bloc’s rules. She also wants to reduce financial contributions to the EU and contradict its laws on border controls.

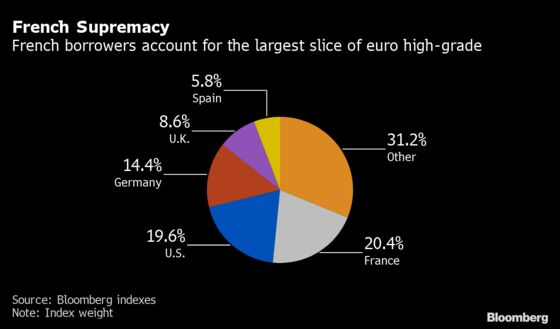

While French borrowers represent more than 20% of the euro-denominated high-grade index, the biggest slice of the pie, risk premiums in the broader market also attest to the general calm this time around.

Credit spreads stand at 135 basis points, well below highs of about 160 basis points recorded in early March, following Russia’s invasion of Ukraine. They tightened right after the first round of the election on April 10 and have widened less than 5 basis points since.

The cost of default insurance in the senior debt of French banking majors Credit Agricole SA, Societe Generale SA and BNP Paribas SA has retreated from March highs and now marginally underperforms the iTraxx Senior Financial index since the start of the year.

Some corporate bond investors see the election result having more of an impact over the longer term. More immediate risks could stem from the war in Ukraine and any further toughening in the stance of central banks as they attempt to tackle runaway inflation.

“We are not complacent as a Le Pen victory would be a significant event for the EU structurally,” said Neil Mehta, a portfolio manager at BlueBay Asset Management, in an interview. “She has changed her tone to some extent and it’s difficult to see an immediate impact rather than structurally slow deterioration, which makes it complicated to trade.”

©2022 Bloomberg L.P.