With Citi’s $47 Fee Sparking Rage, Banks Brace for AMLO Reaction

High bank fees are a problem for Mexico’s economy, as well as for individual customers.

(Bloomberg) -- “Mama, why did they take my money?’’

Tatiana Clouthier had put the peso equivalent of about $80 in a savings account for her daughter Maria a few months earlier. Then a statement arrived showing the new balance: zero. She recalls answering her ten-year-old’s plaintive question as best she could: “Because they charged you fees for I don’t even know what.’’

Mexican banks might have upset the wrong mother. Almost a decade later, Clouthier is among the most powerful lawmakers in President Andres Manuel Lopez Obrador’s party. And she’s backing a campaign that’s spread jitters through financial markets, to make the banks charge less.

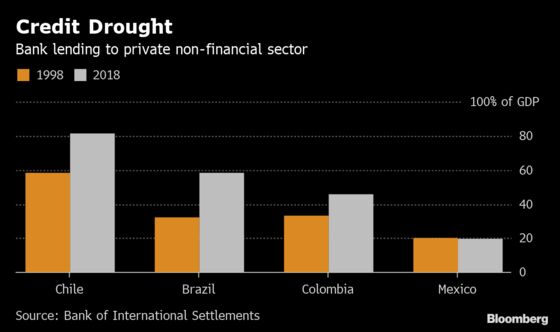

High fees are a problem for Mexico’s economy, as well as for individual customers. Because their flip-side is an unusually low level of lending to households and businesses -– the kind that finances growth.

Lending has been subdued since the Tequila Crisis of 1994, when a peso devaluation spurred capital flight. International banks operating in Mexico typically earn about one-third of local revenue from fees and commissions, according to financial consumer-protection agency Condusef, compared with one-fifth in their home markets where there’s more interest income from loans.

‘Comfort Zone’

“Banks are simply acting in their comfort zone,’’ says Jose de la Cruz Gallegos, director of the Industrial Development and Economic Growth Institute in Mexico City. “They don’t carry out the function of other banks in the world, of being intermediaries between savings and the needs of an economy.’’

What the comfort-zone looks like to a bank customer is, for example, a $47 fee for a bounced check.

That’s what Citigroup Inc.’s Mexican unit charges. It’s equivalent to more than two days’ wages -- while in the U.S., where average earnings are four times higher, Citi would charge $34. Citi does about 4 percent of its lending in Mexico, but earns anywhere from 15 to 30 percent of consumer-banking revenue there.

In a written response to questions, Citibanamex said the fee comparison isn’t fair. It said the $47 bounced-check charge is a maximum, while lower U.S. fees in some cases reflect better legal protections. It said it’s eliminated at least five fees in Mexico in recent years.

By Decree?

Citi wasn’t singled out by Condusef, which slammed lenders across the board. It found HSBC charges Mexico’s highest commissions for mortgage appraisals, though it reportedly scrapped them altogether in the U.K. HSBC also charges about $50 to the writer of a bounced check. Like Citibanamex, HSBC says Condusef made erroneous revenue comparisons between global banks and their Mexico units. It says bank commissions in Mexico generally declined last year.

The banks’ own websites tell the story too. BBVA Bancomer charges clients to print transactions at their own ATMs, whereas there’s no such fee listed in Spain. Grupo Financiero Banorte, where Clouthier’s savings for her daughter got eaten up, can charge customers for the accounts it markets for children when they query transactions that were accurately posted.

The question for Mexico’s government is how to bring the charges down -- by law, regulation or political pressure -– and also get more credit flowing. When plans for legislation were floated in November, they triggered a market slump. Many analysts say doing it by decree could backfire.

Banks could shutter branches in response, says Ernesto Revilla, an analyst at Citibanamex who was chief economist at the Finance Ministry under the previous administration. They’d probably raise credit-card rates to cover losses, says Marta Bastoni at Bloomberg Intelligence.

The government’s strategy isn’t clear. Lopez Obrador came out against legislation -– but also said he wouldn’t interfere in Congress, where his Morena coalition controls both houses. The Senate bill that upset investors, drafted by majority leader Ricardo Monreal, would abolish or reduce 15 categories of fees.

Rule of Law

Monreal says he’s holding it over the lenders’ heads as he waits for their “counter-proposal’’ next month. “We want banks to charge here what they do in their own countries,’’ he says. Clouthier, who’s deputy chief of the lower house, says she’s now leaning toward a fix via bank regulators rather than Congress.

Lopez Obrador has a wider plan to revamp Mexican finance, and he wants the banks on board. Marcos Martinez, head of the Mexican Association of Banks, pledged last month to bring 30 million people into the banking system and turbocharge lending to consumers and small business. He said mobile-phone banking, which would be free of charge, may help.

It’s not the first attempt to juice bank lending, but there are some peculiarly Mexican obstacles.

One is the shaky rule of law. Measures passed under AMLO’s predecessor Enrique Pena Nieto had some success in boosting loans, by allowing development banks to offer more guarantees. But a key component -- the creation of special courts to ease the lengthy, high-risk process of recouping collateral -- never happened, according to Revilla. He says quicker recovery procedures will cut costs for banks, who’ll pass the savings on to customers.

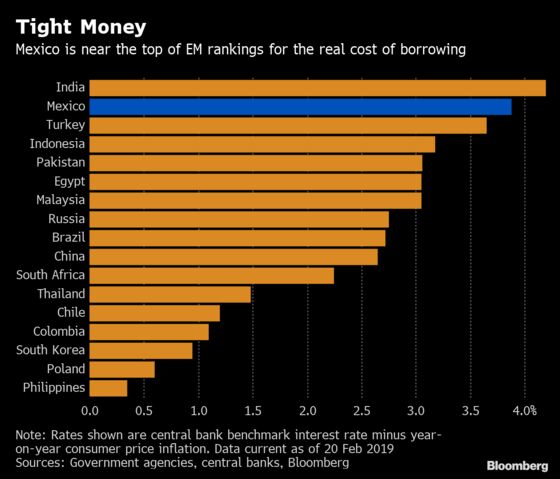

Mexico also has a central bank that’s veered hawkish since the Tequila Crisis. Its current 8.25 percent benchmark translates into some of the highest real interest rates in emerging markets.

That makes it more profitable for banks to buy government debt instruments than “allocate credit to investments where there’s more risk,’’ says Mario Di Constanzo, who recently stepped down as Condusef chief.

Whatever the ultimate reason, broad swaths of Mexico’s population wouldn’t be caught dead in a bank.

Jorge Osvaldo has never had an account. “Banks are difficult to deal with,’’ says the 36-year-old office assistant, who’s worried he doesn’t earn enough to avoid the low-balance fees they typically charge. “I don’t want to pay extra.’’

--With assistance from Michelle Jamrisko, Jenny Surane and Rafael Gayol.

To contact the reporter on this story: Nacha Cattan in Mexico City at ncattan@bloomberg.net

To contact the editors responsible for this story: Carlos Manuel Rodriguez at carlosmr@bloomberg.net, Ben Holland

©2019 Bloomberg L.P.