Bank of Thailand Head Says Virus Fight May Need $30 Billion More

Bank of Thailand Head Says Virus Fight May Need $30 Billion More

(Bloomberg) -- Thailand’s central bank governor called for an additional 1 trillion baht ($30 billion) in government spending to counter coronavirus, saying the blow to the economy from the pandemic is greater than from the Asian financial crisis in 1997.

The government can fund additional spending by borrowing more, Bank of Thailand Governor Sethaput Suthiwartnarueput said Monday at a briefing in Bangkok. Even if public debt tops 70% of gross domestic product by 2024, that would be manageable given high domestic liquidity, low borrowing costs and the country’s current-account surplus, he said.

“Additional state borrowing will help support GDP’s growth potential to revive at a faster rate, and will lower the debt-to-GDP ratio in the long run,” Sethaput said. “If the government doesn’t quickly provide additional economic support during a time of high uncertainty and to shield against a prolonged crisis,” public debt will remain at a high level and will be difficult to lower in the long run.

Thailand is reeling under its worst wave of Covid cases yet, forcing Prime Minister Prayuth Chan-Ocha to impose near-lockdown measures in large swathes of the country and triggering near-daily protests demanding the government’s ouster. Sethaput’s call for more stimulus comes hours after Thailand’s main economic planning body slashed its economic growth forecast for this year to 0.7%-1.2%, down from 1.5%-2.5% predicted in May.

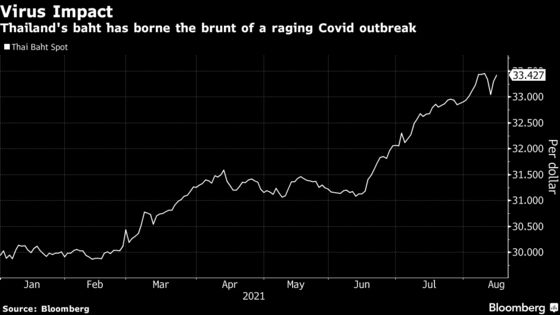

The baht fell as much as 0.5% against the dollar to trade near a three-year low. The currency has lost 10.4% this year, the worst performer among major currencies in Asia.

Cabinet Decision

The government already has announced 1.5 trillion baht in borrowing to fund Covid stimulus steps, including 1 trillion baht last year and 500 billion baht this year. Any decision on fresh stimulus would have to come from Prayuth’s cabinet, which might need to raise a legal cap that currently limits public debt to 60% of GDP.

If fresh borrowing is needed, it may be better now than later, Sethaput said, as waiting could affect the growth potential of Southeast Asia’s second-largest economy. Thai households may lose an estimated 2.6 trillion baht between 2020 and 2022 because of the pandemic, he said.

Earlier this month, the central bank’s rate setting committee voted four to two to hold the key rate at a record-low 0.5% for a 10th straight meeting, while lowering its own forecast for 2021 GDP growth to 0.7%. The two dissenters called for a 25-basis point rate cut, the committee’s first split vote since May 2020.

Covid containment measures are crippling businesses, as well as the livelihoods of more than 40% of the population. The central bank estimates there will be 3.4 million unemployed or nearly unemployed persons in Thailand by year-end, up from 3 million in the second quarter and more than 1 million above pre-Covid levels.

“We do not rule out a further rate cut, as the economic and pandemic situation remains unclear,” Tim Leelahaphan, an economist at Standard Chartered Plc in Bangkok, said in a note. The Bank of Thailand “is prioritizing economic growth over inflation, financial stability and capital flows, in our view.”

Sethaput said the central bank remains “flexible and pragmatic” in its relief measures, adding that the “blunt tool” of the benchmark interest rate alone isn’t enough on its own to help Thailand’s recovery.

©2021 Bloomberg L.P.