Italy's Bonds Lure Investors Into Risky Marriage of Convenience

Italy's Bonds Lure Investors Into Risky Marriage of Convenience

(Bloomberg) --

Investors are being pulled into a loveless fling with Italian bonds, tempted by the prospect of some of the highest yields in Europe.

Italian debt offers 11 times as much as Portugal over five years, while investors get zero for holding the equivalent Spanish bonds. That is leading fund managers to pile in despite a technical recession, the risks from regional elections and the government projecting this year’s fiscal deficit will widen to a level that roiled European markets last year.

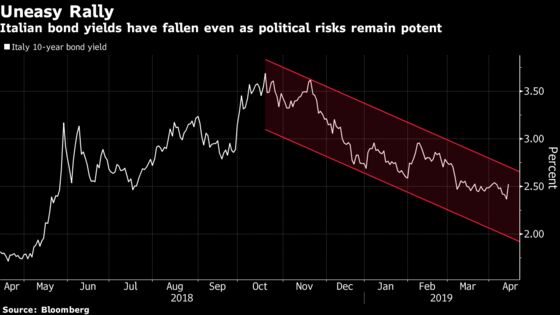

Axa Investment Managers chief investment officer Alessandro Tentori is one of those who have taken advantage of relative market calm to buy the nation’s bonds, known as BTPs, at up to five years of maturity. A gauge of price swings for benchmark debt is at the lowest since a populist coalition came to power in June last year.

“The Italian situation is really scary, don’t get me wrong,” said Tentori, chief investment officer at Axa Investment, which oversees 730 billion euros ($825 billion). “Gun to my head, I would probably dare to stay long BTPs until mid-May.”

That’s when European parliamentary elections are due, which could threaten the stability of the coalition government. Investors have been given the green light to re-enter one of the euro-area’s riskiest markets for now by a global economic slowdown that has led central banks to turn dovish and money to pour into the safest assets, sapping returns elsewhere.

Italian 10-year bond yields touched 2.35 percent last week, an 11-month low, yet were still more than double Spain and Portugal. Five-year yields were at 1.42 percent as of 8:45 a.m. in London, compared to 0.13 percent for Portuguese securities, while Spanish rates dipped into negative territory last week.

Still, the factors that saw Italian bonds slide last year loom large. The ruling pact is a fractious one and the prospect of fresh elections are never far away, while the economy has missed government forecasts. That has forced the Five Star Movement-League coalition to raise its deficit projection to 2.4 percent from 2.04 percent, putting it at the threshold the European Union rejected five months ago.

Traders also have to face two large hurdles in the immediate future: a credit review from S&P Global Ratings on April 26 and the European elections in May. For Citigroup Inc. strategists Aman Bansal and Matteo Regesta, investors should “resist temptation” and avoid buying Italian bonds, with the events likely to boost volatility and erode the returns offered.

S&P currently has Italy two notches above junk, but with a negative outlook.

Many investors are wary but taking the risk. Charles Diebel, a money manger at Mediolanum Asset Management, has a long position on Italian bonds, though has moved further out on the curve to hedge against the politics. A strong performance for Deputy Prime Minister Matteo Salvini’s League in the European elections could create further friction in the coalition, he said.

“It’s a very fragile equilibrium on the market right now,” said Axa’s Tentori.

To contact the reporter on this story: John Ainger in London at jainger@bloomberg.net

To contact the editors responsible for this story: Ven Ram at vram1@bloomberg.net, Neil Chatterjee, Anil Varma

©2019 Bloomberg L.P.