Italy's New Rulers Don't Come for Free

Italy's New Rulers Don't Come for Free

(Bloomberg Opinion) -- After a summer of shadow-boxing over Italian fiscal policy, autumn will deliver the main event. By the end of September, finance minister Giovanni Tria is expected to finalize a medium-term budgetary plan. The entree, however, will be the 2019 Budget Law, due in October.

Over this period, rating agencies will complete their reviews of the country’s credit-worthiness. Another downgrade would put Italian government bonds dangerously close to falling below investment grade, with potentially far-reaching consequences. These include forced selling by institutional investors and restrictions on their use as collateral with the European Central Bank.

The background is troubling. Italy stands out among advanced economies for its high stock of public debt. About 20 percent of it sits with the Bank of Italy and 50 percent is in private Italian hands, mostly financial institutions. Yet this isn’t just a local problem. Non-residents own $800 billion of Italian government securities – not far below the amount of German government debt held outside Germany.

In view of the size of the debt, Italian macro policy has been driven by the need to maintain a surplus in the primary fiscal balance – the difference between tax receipts and public spending net of interest payments. Apart from a brief spell in 2009, Italy’s primary budget has been in the black since the early 1990s. Tria wants to stick to this approach.

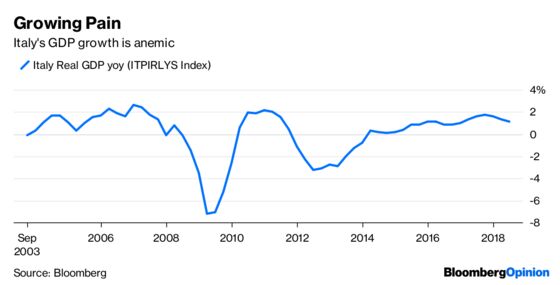

His biggest problem is anemic growth. Per capita income has been falling for decades, which is often blamed on being in the euro zone. But it primarily reflects rigid labor and product markets, administrative and legislative inefficiencies, and high taxation.

Reforms and austerity haven’t helped, probably because they weren’t followed through entirely nor accompanied by a stricter cleanup of domestic banks. Five years after the “technocrat” governments of the early 1990s administered their bitter fiscal medicine, per capita GDP stood 12 percent above pre-crisis levels at constant prices. By contrast, six years after Europe’s 2011-2012 sovereign debt crisis, real income per head is still 2 percent lower – a much worse performance than Spain and Portugal.

Predictably, stagnation has left voters disenchanted with the liberal, European policy consensus. The malaise has found expression in the motley coalition government formed by the League and Five Star Movement.

Given the social backdrop, a fiscal relaxation was on the cards whichever party took the helm. Still, institutional constraints and market pressure make it difficult to see the populist coalition veering away from a primary fiscal surplus above 1 percent of GDP. Goldman Sachs economists expect Tria to project a primary surplus of about 1.4 percent for 2019, resulting in a deficit of about 2.1 percent – similar to the average between 2015 and 2017. If correct, fears about a spike in public sector funding seem overdone, and largely priced in.

A more pressing question is whether the budget measures will support growth. Italy’s GDP expansion, expected to be about 1 percent this year in real terms, has slowed more than in other large euro zone countries. That’s been driven by weak domestic demand, suggesting political unease is taking a toll.

In theory, the League and Five Star might be more economically daring than their predecessors. Possibilities include a broad reform of unemployment insurance and a corporate tax cut. In practice, their desire for quick – and often conflicting – political gains may push them in too many directions. Both parties say they will run separately in future elections and the mix of policy initiatives risks being spread too thinly.

The tragic Genoa bridge collapse also shows the poor state of the nation’s infrastructure. Net public infrastructure spending is just 60 percent of what it was before the 2008 crisis and Tria plans to increase it. But hostility toward big public works, especially within Five Star, coupled with procurement risks and local political resistance, makes it hard to see a big take-off in investment.

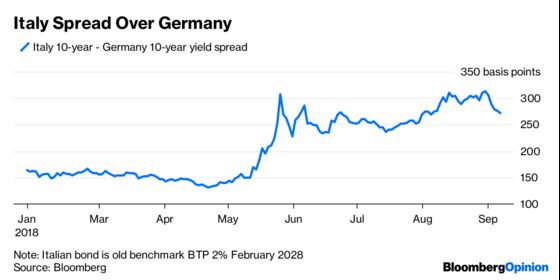

All the anxiety has crystallized in Italy’s borrowing costs. These have shot up since the coalition agreement emerged in mid-May and ministers attacked the EU fiscal framework and made ambivalent noises about staying in the monetary union. In the seven-to-10-year maturity area, Italian government bonds trade between 250 and 300 basis points above their German counterparts, compared to an average of 150 basis points in the six months before the March election.

Goldman Sachs research indicates that the “fair value” 10-year spread should really still be in that pre-election ballpark, when taking into account macroeconomic and systemic risks, weak growth and the deteriorating fiscal outlook. That’s similar to Portuguese bonds, which already implies a penalty given that Italian bonds are usually more liquid.

So, using these estimates as a gauge, an Italian/German spread of 250-300 basis points puts a price on the doubts around Rome’s fiscal plans of at least 1 percentage point. Such additional funding costs mean a lot to a heavily indebted country. If the extra spread persists over the next year, Italy would spend about 4-5 billion euros more than if it were at 150 basis points. That could pay for a 10-15 percent increase in public works.

Should the government ease fiscal policy without compromising debt sustainability, the spread could pull back toward a 200-250 basis point range. That would offer respite to Tria, but wouldn’t fix the medium-term problem. With German Bund yields set to rise toward 1 percent in 2019, a spread above 200 basis points would mean Italian 10-year bonds yielding more than 3 percent.

Yet higher funding costs, without a tougher approach to debt, will be manageable only if growth is sustained. As such, the recent squeeze on the Italian banks’ funding terms – caused by pressure on the sovereign rating – bears close watching. It could be another brake on GDP.

So greater fiscal clarity alone won’t be enough. The coalition needs to improve the fundamental growth outlook, and this doesn’t appear to be in store.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Francesco Garzarelli is an advisory director to Goldman Sachs International.

©2018 Bloomberg L.P.