Knocked-Down Euro May Yet Deliver a Comeback Hook Against Dollar

Knocked-Down Euro May Yet Deliver a Comeback Hook Against Dollar

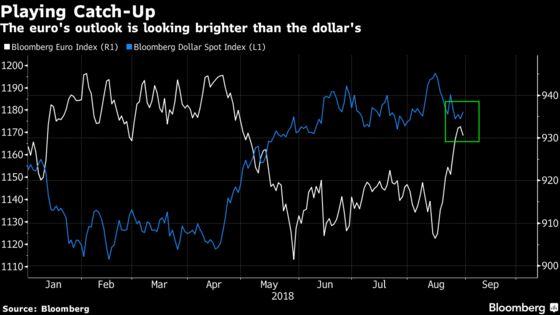

(Bloomberg) -- After a stellar start to the year, the euro was steamrolled by a resurgent dollar. Now, the tables may be turning yet again.

Monetary-policy expectations may favor the common currency more from here on, according to Commerzbank AG, which sees the European Central Bank raising interest rates earlier than markets are pricing in. For fund managers at Aviva Investors, the euro’s recent losses look overdone and it should gain on prospects of improved growth and reduced political risks in the region.

At the same time, the dollar’s outlook is less bright than before, not least due to growing skepticism over the Federal Reserve’s ability to maintain the pace of rate increases. Pacific Investment Management Co.’s Mark Kiesel sees the U.S. economy slowing, pressuring the Fed to moderate its tightening pace.

“We expect the Fed to slow down its rate hiking cycle while the ECB starts,” said Esther Reichelt, a strategist in Frankfurt at Commerzbank. “The important question for the euro will be whether the ECB will indeed start a meaningful normalization and will this be priced in in advance depending on the inflation dynamics in the next months and quarters.”

Reichelt and colleagues forecast the euro to climb 8 percent from current levels to end 2019 at $1.26. The shared currency has slumped more than 5 percent since the end of March, after rallying 2.7 percent in the first quarter. The slide has probably “bottomed out” now, according to ABN Amro Bank NV.

ECB Outlook

The ECB is planning to phase out its asset-purchase program by December and possibly raise rates late next year. Earlier in August, it said accelerating euro-area wage growth is a harbinger of higher future inflation.

Commerzbank predicts 10-year bund yields to climb more than 60 basis points to 1 percent by end-2019, dwarfing an estimated increase of less than 40 basis points in benchmark Treasury yields. This would tighten the yield spreads between the two markets in favor of the euro.

Across the Atlantic, the dollar faces headwinds amid growing signs that U.S. economic strength may have peaked. The persistent flattening of the Treasury yield curve, often seen as a recession signal, is also prompting investors to question the Fed’s policy path. That makes the greenback “less attractive” in the medium term for Commerzbank’s Reichelt.

Fed Dynamics

While setting the stage for a September rate hike, Fed Chairman Jerome Powell said last week that “there does not seem to be an elevated risk of overheating.” The gap between the 10- and two-year Treasury yield shrank to its narrowest since 2007, as his comments were perceived as dovish.

Not everyone is convinced on this. Goldman Sachs Group Inc. has cautioned that interpreting Powell’s comments as dovish for the rate outlook might be a mistake, sticking to its call for two more hikes this year followed by four in 2019. For ING Groep NV’s Martin van Vliet, any slowdown in Fed policy would have ramifications on the ECB.

“The Fed would only under-deliver if something unexpected or bad happens to the U.S. economic outlook and I doubt the euro-zone outlook would not be affected accordingly,” said Amsterdam-based van Vliet, senior interest-rate strategist at ING. “That’s why we are happily expecting the widening trend in 10-year Treasuries-bund spreads to persist in the remainder of this year.”

Still, the euro could be in for an upswing given the region’s improving economic outlook. While there is a risk of the currency slipping to $1.15 in the near term, it is likely to rebound and strengthen to $1.25 by the end of 2019, according to ABN Amro strategists including Georgette Boele.

“We expect that the weakness in the euro-zone economy is behind us,”’ they wrote in a research note. “It is likely that expectations will be adjusted upward, supporting euro-dollar.”

To contact the reporter on this story: Anooja Debnath in London at adebnath@bloomberg.net

To contact the editors responsible for this story: Ven Ram at vram1@bloomberg.net, Anil Varma, Neil Chatterjee

©2018 Bloomberg L.P.