S&P 500's Run at Record Lacks Animal Spirits

S&P 500's Run at Record Lacks Animal Spirits

(Bloomberg Opinion) -- The S&P 500 Index is almost back to its all-time high reached in January despite a litany of adverse shocks on the domestic and international fronts. It's not that these shocks don't matter. It's just that they pale in significance against the market’s cheap valuation.

Many investors cite complacency for the ability of the market to rebound from the late January and early February correction despite escalating global trade tensions, political dysfunction in assorted countries, the inability of the U.K. to work out a Brexit deal with the European Union, a new populist government in Italy, slower economic growth in China and the ongoing probe by special counsel Robert Mueller into Russia’s efforts to infiltrate and undermine the 2016 presidential election.

Each of these developments is a negative for the market, but even when taken all together are not more important, as yet, than the rise in corporate profits that renders stocks on the cheap side. The U.S. economy is performing well with no signs of imbalances or recession on the horizon, while corporate profits are beating forecasts and 2019 projections are being revised higher. Share prices are below average historically when compared with expected earnings and well below average when adjusted for interest rates.

The other thing to consider is that much of the rebound in the S&P 500 to 2,858.45 on Tuesday, just shy of the record closing high of 2,872.87 on Jan. 26, is due to a very short list of names. Three companies, Amazon.com Inc., Netflix Inc. and Microsoft Corp. accounted for 71 percent of the S&P 500's increase through early July. Add in three more companies -- Apple Inc., Google parent Alphabet Inc. and Facebook Inc. -- and just six stocks accounted for an incredible 98 percent of the market's advance. The rest of the market was essentially flat.

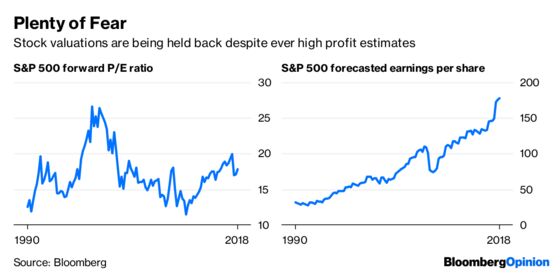

In the meantime, corporate profits are rising very strongly. With more than 80 percent of the S&P 500 having already reported for the second quarter, earnings increased by about 25 percent from a year earlier, topping expectations of a 20 percent gain that many dismissed as unduly optimistic. Estimates for 2019 are rising. According to data compiled by Bloomberg, the latest estimate suggests S&P 500 profits will be about $178 a share in 2019, which implies that the forward price earnings multiple for the market is right at 16 times, compared with an average of well more than 16 over the last 50 years.

Moreover, market multiples are inversely related to inflation and interest rates. So with the benchmark 10-year Treasury note still yielding less than 3 percent, market multiples should be about 19.5 based on historical averages. Taken at face value, this implies the S&P 500, which is currently at about 2,850, would need to hit 3,470 by the end of this year to be priced on par with other historical periods when inflation and interest rates were comparable to today. The difference of about 22 percent can be taken as the discount -- or risk premium -- demanded by the market for the all the uncertainty faced by investors.

Symmetrically, this discount is also reflected in the premium investors pay to own bonds. Investors buying 10-year Treasuries today know they will earn a negative real after tax return locked in for that entire period. A 3 percent yield subjected to a top tax rate of 37 percent and an inflation rate of 2 percent implies a negative return of 11 basis points annually. If inflation averages more than 2 percent over this 10-year horizon, the net return declines basis point for basis point.

Stock and bond valuations suggest investors are fearful, not complacent. That fear is reinforced by the many warning against an impending market decline or suggestions of a market top, which encourages many investors to move into cash, which leads to regret as the market moves up. This is especially the case for professional money managers, who then fall behind their benchmarks. The result is a market climbing the proverbial wall of worry.

It's impossible to say how far the market can run up from here, although bear markets simply don’t occur until economic expansions weaken into recessions. But there are simply no signs of a recession on the horizon. Inflation and rates are low, even though both are likely to rise further. Economic growth is strong, and so are corporate profits. And there is enough nonsense going on in domestic and international politics to keep investors from becoming overly exuberant. The biggest risk is the growing scarcity of labor, which should fuel inflation and, eventually, rates. But this may take a while and any deceleration in growth would push the next recession even further into the future.

To contact the editor responsible for this story: Robert Burgess at bburgess@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Charles Lieberman is chief investment officer and founding member at Advisors Capital Management LLC. He may have a stake in the areas he writes about.

©2018 Bloomberg L.P.