Goldman, Morgan Stanley Say Test Scores May Not Curb Payouts

Goldman, Morgan Stanley had lowest leverage ratios in annual stress test.

(Bloomberg) -- Goldman Sachs Group Inc. and Morgan Stanley are imploring investors not to get spooked.

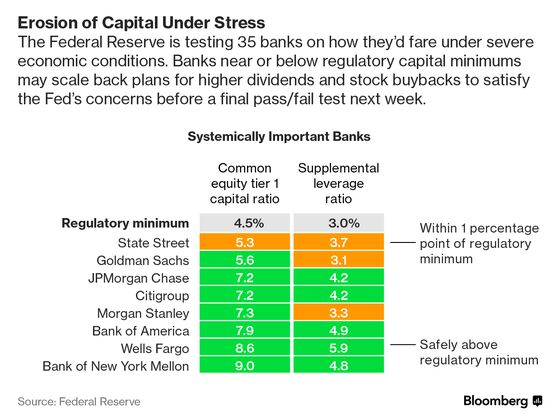

The investment banks had the two lowest capital levels by one key measure in stress test results released Thursday by the Federal Reserve, threatening to limit how much cash they’ll be able to return to shareholders through dividends and stock buybacks. But both firms say they may be able to return more than Thursday’s figures would suggest.

The “ratios that are published today may not represent our firm’s actual capital return capacity, which may be higher than this year’s test would otherwise indicate,” Goldman Sachs said in a statement. “Our models and the Federal Reserve’s models diverge, which we expect to discuss with the Federal Reserve.”

While all 35 of the lenders in the opening round of the central bank’s stress test showed they could withstand a severe economic downturn, not every one cleared the bar by a comfortable margin. Goldman Sachs’s supplementary leverage ratio fell to 3.1 percent in the test, while Morgan Stanley’s hit 3.3 percent, barely above the minimum 3 percent they must clear in next week’s second part of the annual exam.

Both banks said their own models show the ratios should have remained above 4 percent. Morgan Stanley said the Fed’s results “may not be indicative of the capital distributions that we will be permitted to make” after next week’s test.

Shares of Goldman Sachs and Morgan Stanley were little changed in early trading in New York, suggesting investors are taking comfort in the two companies’ comments about their payout expectations. James Mitchell, an analyst at Buckingham Research Group, said the recent tax-law changes might be responsible for the discrepancy between the Fed’s calculations and the firms’ views.

“It would be very unlikely that GS and MS would release such forceful statements without first discussing it with the Fed, and so we can only conclude that there may be errors in the Fed’s models for taxes,” Mitchell wrote in a note, referring to the companies by their stock symbols. “We would view any material selloff as a potential buying opportunity.”

Fed officials routinely warn that the first test differs from the one next week, known as CCAR, which determines whether the regulator approves a bank’s capital plan. Still, investors often look to this round to determine whose capital plan might be in danger of being scaled back.

Gerard Cassidy, a bank analyst at RBC Capital Markets, said he expects the two firms to have lower payouts than last year while rivals increase their buybacks and dividends.

Read more about the stress tests’ impact on bank stocks

Banks have long complained that the Fed’s models don’t match their own internal formulas on the losses that would be incurred during adverse economic conditions. The industry has lobbied for more transparency on the Fed’s formulas, but has only gotten limited disclosures in return.

In 2016, Morgan Stanley passed the test conditionally, with the Fed saying the firm exhibited “material weaknesses” in its capital planning and requiring a resubmission of the plan by the end of that year. Morgan Stanley didn’t fight the findings, but said it would resubmit to fix the issues. In 2014, Goldman Sachs had to lower its request for capital return after its models differed from the Fed’s.

The Fed started using the annual tests after the 2008 financial crisis to force lenders to bulk up their ability to weather losses. Each year, the agency hatches different hypothetical crises, and the process has become the most important supervisory effort to emerge from the meltdown a decade ago.

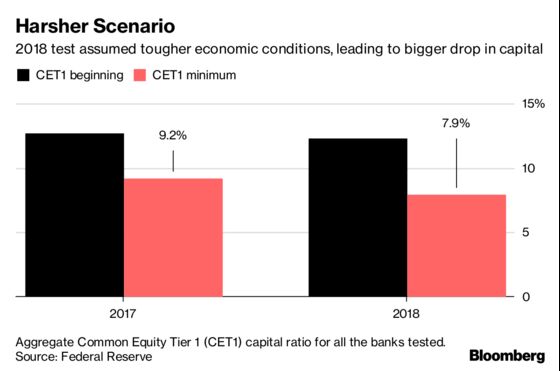

The Fed has designed the tests to get tougher as the economy improves, so this year’s hypothetical scenarios were seen as particularly hard and would have caused an estimated $578 billion in losses across the industry. Both Goldman and Morgan Stanley were expected to be snared in the tests because their earnings are more closely linked to capital markets, which suffer more under the tougher macroeconomic scenario in this year’s test.

The Fed also added the U.S. operations of some foreign banks, including Barclays Plc, Credit Suisse Group AG and a wider swath of Deutsche Bank AG’s American business. The foreign lenders turned in some of the highest capital scores.

--With assistance from Sridhar Natarajan.

To contact the reporters on this story: Yalman Onaran in New York at yonaran@bloomberg.net;Jesse Hamilton in Washington at jhamilton33@bloomberg.net;William Mathis in New York at wmathis2@bloomberg.net

To contact the editors responsible for this story: Michael J. Moore at mmoore55@bloomberg.net, ;Jesse Westbrook at jwestbrook1@bloomberg.net, Steve Dickson

©2018 Bloomberg L.P.