Panic Buying Looks Like the Last Hope of Bond Bulls

Panic Buying Looks Like the Last Hope of Bond Bulls

(Bloomberg Opinion) -- It’s been lonely of late to be bullish on bonds. Except, of course, when financial markets become hysterical that a full-blown European crisis is just around the corner.

Benchmark 10-year Treasury yields reacted as they usually do during times of panic, tumbling 15 basis points on Tuesday as the prospect of nationalist parties seizing control in Italy prompted billionaire George Soros to raise the specter of an “existential threat” to the European Union. Traders began questioning the Federal Reserve’s resolve to raise interest rates in June — a foregone conclusion for months. Bond bulls, if only for a moment, were the in-crowd once again.

Of course, the momentum didn’t last. Yields rose about 8 basis points on Wednesday to 2.86 percent, in part because Italy successfully auctioned five- and 10-year bonds (though, as my colleague Marcus Ashworth points out, the bid-to-cover ratio comes with some caveats).

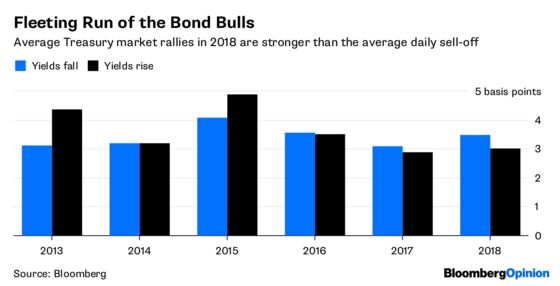

But the magnitude of the initial gains reinforces an unusual trend: The average rally for 10-year Treasuries this year is much larger than the average sell-off. In other words, when yields decline, it’s swifter and more violent.

That isn’t necessarily what you’d expect during a year of rising interest rates. In 2013, during the taper tantrum, the 10-year yield rose 4.4 basis points on average during sell-offs while falling only 3.1 basis points in advances. That’s the exact opposite of what’s happened so far this year, with yields rising just 3 basis points when they go up while dropping 3.5 basis points when headed down.

In some ways, it’s the flip side of the phenomenon gripping the U.S. stock market. As Bloomberg News reports, not since 1948 have equities tumbled so severely relative to their up days. Yet it’s not quite the same. In a handful of instances this year (Feb. 2, Feb. 8, March 23 and April 2), the S&P 500 Index dropped more than 2 percent and Treasury yields fell just a basis point, if not increased outright. It takes a certain kind of market frenzy, it seems, to knock the world’s biggest bond market off course.

Increasingly, it looks as if pure flight-to-quality, risk-off demand is the last pillar of support for the remaining Treasury bulls. And it’s comforting, at least, to know that the market still serves that haven function when the federal budget deficit is swelling and the Fed pretty much stands alone in tightening monetary policy.

Strategists at BMO Capital Markets cheered the bullish move by saying yields “take the stairs up and the elevator down.” It takes just “a simple failure anywhere” to send them down, they said, while they face a slow grind higher because positive economic forces need to line up just right.

But in all likelihood, this episode is merely a speed bump on the way to higher yields. Just two weeks ago, the 10-year Treasury yield hit its highest point in nearly seven years. That peak came just days after Citigroup’s economic surprise index, which measures U.S. data relative to market expectations, fell to its lowest level since October. It has since retreated even further.

That throws cold water on the argument that everything has to go right for the market to stay at 3 percent. On the contrary, Treasury yields climbed to these lofty levels in the face of data that appeared to be just good enough to keep the Fed on its rate-hike path.

For now, the Treasury market is settling into its new range as the political situations in Italy, Spain and elsewhere remain fragile. If recent history is any guide, it’s not going to reverse all those gains in a day. At the same time, these bouts of risk-off demand are almost fleeting by definition. Unless a crisis is truly starting to simmer, bond bulls can’t count on one good day to carry over to the next.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

©2018 Bloomberg L.P.