ECB at 20 Can't Shake Existential Angst Amid Italian Crisis

ECB at 20 Can't Shake Existential Angst as Italian Crisis Flares

(Bloomberg) -- The European Central Bank’s 20th anniversary arrives on Friday as another financial scare -- this time in Mario Draghi’s Italian homeland -- shows that the euro area still hasn’t grown up.

It’s a chance for the ECB president to remind governments that their political project, to create a monetary union out of economically and culturally disparate sovereign nations, is far from finished. As anti-establishment populists gain ground across the bloc, the risk is that the single currency’s weaknesses could allow it to be ripped apart.

Italy highlighted that tension this week when a euro-skeptic finance minister nominated by democratically elected politicians was vetoed by the nation’s president, putting the country on course for new polls. Bond yields soared in the country, but also in neighboring Spain and Greece, awakening memories of 2012 when investors bet the euro zone would splinter.

“The euro keeps catching up with the effects of the last crisis and then another one breaks,” said David Marsh, head of OMFIF, a think-tank for central banking, and author of books on the history of the euro. “Either you move to some kind of political union with genuine pooling of sovereignty -- a genuine sharing of risks including necessary debt restructuring, which is pretty large step -- or a danger of some catastrophic crisis or a breakup becomes more acute.”

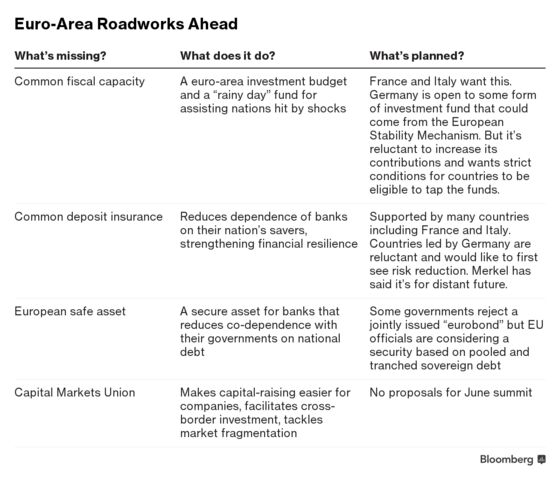

Some of those concerns will be addressed by European Union leaders at a summit on June 28-29, where German Chancellor Angela Merkel and French President Emmanuel Macron have pledged to present a joint initiative to boost the union’s resilience.

Major progress might be hard to agree on though, as Merkel faces resistance from among her allies and parts of the opposition. She’s unlikely to loosen her stance given that Italy’s election earned victories for parties promising big spending in the country that already has the euro area’s largest debt burden.

“The main issue is that participation in the euro requires countries to respect certain conditions and rules,” said Francesco Papadia, who was head of the ECB’s market operations from 1998 to 2012 and is now a senior fellow at the Bruegel think-tank in Brussels. “If these conditions and rules are not respected, the construction is shaken.”

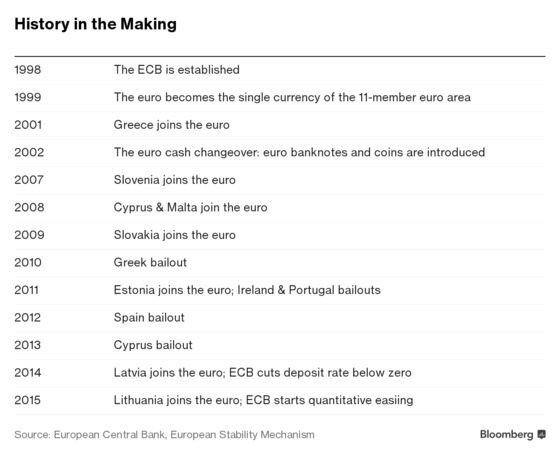

The ECB itself is certainly is stronger than on June 1, 1998, when it was formed out of the European Monetary Institute and set up in a rented tower block in downtown Frankfurt. That was seven months before the euro was introduced.

“European Monetary Union was an hubristic endeavor from the start, full of unprecedented ambition in historical terms. The initial minimalist design didn’t do justice to the wide-ranging implications of the project. The framework is not yet complete and is still risking existential threats.”

-- ECB Vice President Vitor Constancio, May 17

The central bank has taken on responsibility for banking supervision, and developed powerful new tools such as quantitative easing, negative interest rates and free bank loans to guide the euro zone through two financial crises and avert the risk of deflation. Euro-zone membership has jumped to 19 countries from 11.

Read more

|

Yet it also became a lightning rod for public discontent. Its new 1.3 billion-euro ($1.5 billion) headquarters was a focal point for riots in 2015, and the institution was in the crossfire the same year as Greece was forced to impose capital controls. Core countries Germany, France, the Netherlands and Austria have all seen the rise of political groups opposed to the euro and to deeper integration.

Sweden’s Riksbank, the world’s oldest central bank, is celebrating its 350th anniversary this year. Speakers at a conference last week to mark the occasion included the heads of the 324-year-old Bank of England, Mark Carney, and the 105-year-old Federal Reserve, Jerome Powell.

The ECB is a newborn in comparison, but one tasked with being the custodian for the world’s second-biggest currency.

“Can a currency survive without a political union, a monetary union without a political union?” Otmar Issing, the institution’s first chief economist, said at the event. “How must the monetary union be reformed to make it less fragile in the context of crises? These are the challenges which the ECB will be confronted with for, I am afraid, some time to come.”

Outgoing ECB Vice President Constancio echoed that sentiment in more granular form in a video posted on Twitter on Thursday, the day of his retirement.

“The crisis itself showed that the initial design of the monetary union was insufficient,” he said, highlighting flaws from a lack of common deposit insurance to the need for a region-wide capital market. “Monetary union, being a collective endeavor, needs at the center a macro stabilization function -- and that has to be done by introducing a stronger coordination of fiscal policies.”

--With assistance from Viktoria Dendrinou and Zoe Schneeweiss.

To contact the reporters on this story: Paul Gordon in Frankfurt at pgordon6@bloomberg.net;Piotr Skolimowski in Frankfurt at pskolimowski@bloomberg.net

To contact the editors responsible for this story: Paul Gordon at pgordon6@bloomberg.net, Brian Swint, Jana Randow

©2018 Bloomberg L.P.