Goldman Sees More Bond Pain for Italy Given Portugal's History

Goldman Sees More Bond Pain for Italy Given Portugal's History

(Bloomberg) -- For a template on how to trade Italy 2018, investors should look back to Portugal in 2015.

That’s the advice of Goldman Sachs Group Inc. The lesson is Italian bond yields have further to rise as a coalition of populist parties is poised to form a government, but that a Greece-style threat to the euro area isn’t looming.

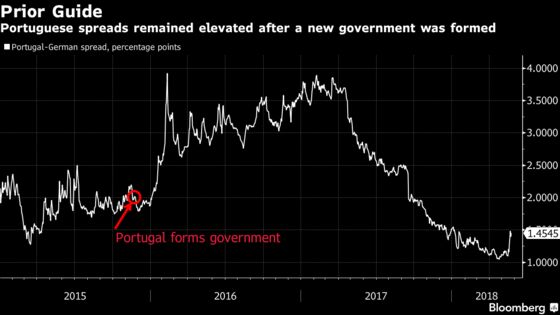

The Portuguese example after the formation of a socialist government in 2015 suggests yield spreads over equivalent German benchmarks can be “significant and persistent” for some time, Goldman economist Huw Pill wrote in a note to clients on Wednesday.

“The Portuguese experience shows the election of a more populist government embodying euroskeptical elements in Italy need not create the existential crisis and domestic financial meltdown that we observed in Greece,” Pill said. “That said, we continue to view current market pricing as reflecting a somewhat complacent view of political developments in Italy.”

Italy’s 10-year yield spread over comparable German bunds widened to 193 basis points Wednesday, the most on a closing basis since June. That compares with more than 550 basis points at the height of the euro-area debt crisis in 2011.

Italian President Sergio Mattarella summoned premiership candidate Giuseppe Conte, a Florence law professor, for talks on Wednesday afternoon, the head of state’s office said in a statement.

Italian Outlook

Greece, where spreads ballooned to 1,800 basis points in 2015, has always been seen as a “special case” by European authorities, according to Pill.

That leaves the Italian outlook for spreads resembling the Portuguese example, able to go wider without triggering an existential crisis of the euro, he said. In the Portuguese case, spreads widened 150 basis points for more than a year, according to Pill.

“We see the ‘search-for-yield’ dynamic prompted by the ECB’s non-standard monetary policy measures as sufficient to avoid a return to the extreme tensions of 2011-12,” Pill said. Still, Italy’s public finances remain vulnerable, and the European Central Bank’s policy “relies on governments taking a cooperative approach to addressing market tensions,” he said.

--With assistance from Joao Lima.

To contact the reporter on this story: Marcus Bensasson in Athens at mbensasson@bloomberg.net

To contact the editors responsible for this story: Fergal O'Brien at fobrien@bloomberg.net, Keith Jenkins, Neil Chatterjee

©2018 Bloomberg L.P.