Yep, Bitcoin Was a Bubble. And It Popped.

(Bloomberg Opinion) -- It seems like every asset bubble has a famous anecdote of someone claiming, right at the top, that a crash is impossible. In the stock-market bubble leading up to the Great Depression, it was economist Irving Fisher, who declared in the New York Times that stocks “have reached what looks like a permanently high plateau” a few days before a collapse that would see stocks lose 89 percent of their value. In 2007 and 2008, many optimistic pronouncements by current National Economic Council Director Larry Kudlow turned out to be disastrously wrong.

In the great Bitcoin bubble of late 2017, the honor goes to John McAfee, founder of computer security company McAfee LLC, and passionate cryptocurrency evangelist. On Dec 7, 2017, he wrote:

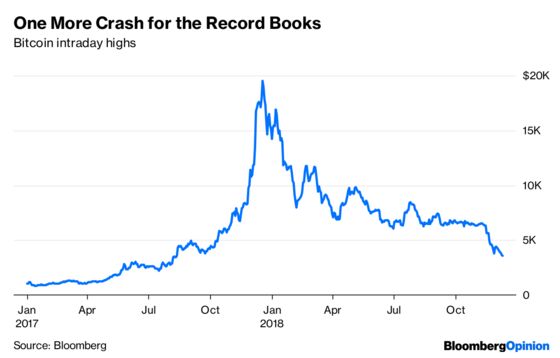

A few days later, Bitcoin’s price briefly peaked at $19,511, before it began an epic plunge that would see the original cryptocurrency lose approximately 82 percent of that value as of the writing of this column:

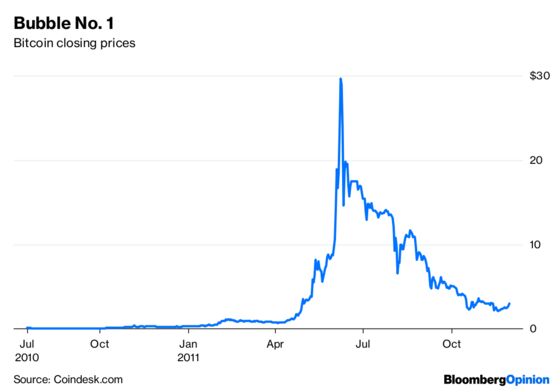

Does that mean Bitcoin is dead? Not necessarily — the cryptocurrency has recovered from several previous bubbles and crashes, including one in 2011 that was just about as devastating:

Also, it’s worth noting that even if they’ve held on to all of their Bitcoin (or HODLed, as many call it), early investors have still come out ahead in the latest bubble — the current price, though down spectacularly from the peak, is still more than triple what it was when 2017 began. And if they sold some of their holdings at or near the peak, as many are reported to have done, they’re in even better financial shape.

But for ordinary investors, who don’t tend to get in early on potentially revolutionary new technologies or to have the savvy or luck to time the market, the Bitcoin bubble should serve as a learning experience. The most important lesson is: Financial bubbles are real, and they will make your life’s savings vanish if you aren’t careful.

Formally, an asset bubble is just a rapid rise and abrupt crash in prices. Defenders of the efficient-market theory argue that these price movements are based on changes in investor’s beliefs about an asset’s true value. But it’s hard to identify a reason why any rational investor would have so abruptly revised her assessment of the long-term earnings power of companies in 1929, or the long-term viability of dot-com startups in 2000, or the long-term value of housing in 2007.

Similarly, there was no obvious reason why it made sense for the world to believe that Bitcoin was the currency of the future late December 2017, but to think this was less than one fifth as likely today. Bitcoin wasn’t eclipsed by a competitor — the main alternative cryptocurrencies had even bigger price declines. Nor have regulators cracked down on Bitcoin — in fact, the regulatory structure has generally been quite accommodating to the technology. Nor have critical technological flaws emerged — yes, the Bitcoin network has become congested, but this problem was anticipated well before the crash.

Instead, it seems overwhelmingly likely that Bitcoin’s spectacular rise and fall was due not to rational optimism followed by sensible pessimism, but to some kind of aggregate market irrationality — a combination of herd behavior, cynical speculation and the entry into the market of a large number of new, poorly informed investors.

It was this latter type of investor who got burned. There is no shortage of horror stories about people around the world who poured their modest life’s savings into what looked like a sure bet, only to see it vanish — some of it into the pockets of Bitcoin’s early-investor aristocracy, some of it into thin air.

How can regular, average investors avoid this fate? Bubbles are extremely hard to spot — if it was easy, they wouldn’t exist in the first place. But there are two important strategies investors can use to limit their risk.

First, realize that there’s no such thing as a sure bet. The optimistic Bitcoin story, repeated often by the cryptocurrency’s army of gung-ho online evangelists, was that Bitcoin was going to replace standard fiat money as the main global currency. But that story always had major holes. Assets with high volatility and high long-term expected returns make bad currency, since short-term volatility renders them less useful for making payments — you’ll notice that nobody buys pizzas with ingots of gold or shares of Apple stock. Second, cryptocurrency is an impressive new technology, but there are major technological limitations related to security and usability that have yet to be overcome.

Since nothing is a sure bet, regular investors need to stay diversified. It’s OK to put a bit of your savings into something like Bitcoin, just in case the price goes way up, but just don’t make it a very large piece. The potential pain of a crash should far outweigh the fear of missing out. I myself lost money in the Bitcoin crash (I still have my Bitcoins and have not sold). I just didn’t lose very much, because I only invested a very small portion of my assets.

In the end, the Bitcoin bubble may have been a net good for society. The total amount of wealth involved — a few hundred billion dollars, spread out around the globe — was small compared to the 2000s housing bubble or the 1990s dot-com bubble, meaning the pain will be limited. And the experience of such a classic, perfect financial bubble may be sufficient to teach the millennial generation what their forebears learned much more painfully — if something looks too good to be true, it usually is.

To contact the editor responsible for this story: James Greiff at jgreiff@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Noah Smith is a Bloomberg Opinion columnist. He was an assistant professor of finance at Stony Brook University, and he blogs at Noahpinion.

©2018 Bloomberg L.P.