Why Treasuries Can’t Be a Weapon in the Trade War

(Bloomberg Opinion) -- As far as ideas go, the notion that Beijing has bargaining power over Washington by virtue of being America’s largest creditor is an old chestnut.

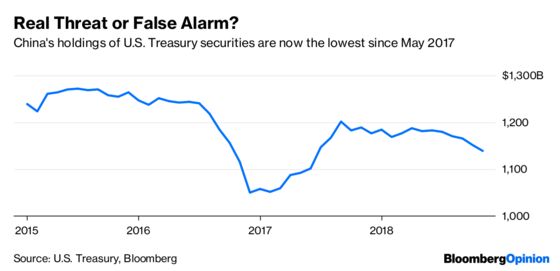

However, the current U.S.-China trade conflict has revived interest in the drop in Chinese holdings of U.S. Treasuries to their lowest level in a year and a half. The fifth straight decline took the stock of bills, bonds and notes to $1.14 trillion in October, down from $1.15 trillion the previous month. Is this a sign Beijing is retaliating?

Knowing how much President Donald Trump hates high U. S. interest rates, the threat of a spike in long-term bond yields could very well force him to replace the current truce in the tariff war with a durable peace – or ratchet up the confrontation. Don’t get your hopes (or fears) up, though.

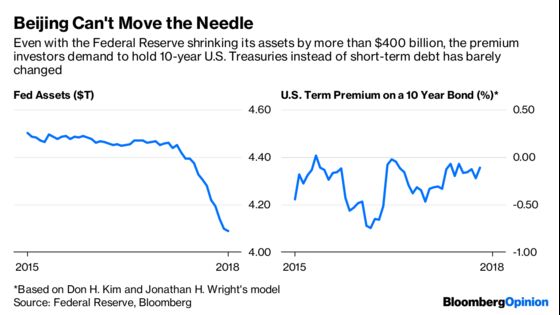

The reality is more mundane. The view that Treasuries are some kind of a nuclear weapon in a war of financial terror predates the 2008 subprime crisis and unprecedented bond-buying by the Federal Reserve that followed. That experiment has, among other things, punctured the argument that Chinese buying calls the shots.

Nor would Chinese selling make a big difference. Even if Beijing decided to sell its entire $1-trillion-plus holdings, Brad Setser, a senior fellow at the Council on Foreign Relations in New York, estimates the increase in long-term U.S. yields to be in the ballpark of 30 basis points. Slap on another 30 basis points as a safety margin, and Fed Chair Jerome Powell’s headache may be no more than a “painful but ultimately bearable” 60 basis points, he says.

If the Fed was convinced this is what Beijing hoped to accomplish, all it would need to do is stop raising short-term rates after this Wednesday. Given the nervousness in the stock market, a pause wouldn’t exactly be surprising. Yes, investors might read the Fed’s hesitance as a sign that a U.S. recession is closer than they thought. It might be a little inconvenient for Powell to forgo the three rate increases currently penciled in for 2019: Meeting a slowing economy without having jacked up rates to a point where they could be cut boldly could ignite expectations of a resumption of quantitative easing.

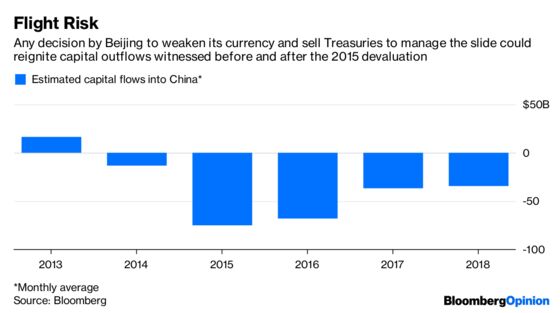

However, China will be in a bigger mess. Non-U.S. assets would get too bubbly if Beijing decided to buy them by swapping out of Treasuries. Instead, the authorities will have to signal a devaluation so that the market sells yuan, and Beijing buys them by offloading dollars (and Treasuries). An acceleration of capital flight from China would be the most logical consequence. Would China want to grapple with a trade war – and the aftermath of the arrest in Canada of a high-profile Huawei Technologies Co. executive – while it battles destabilizing capital outflows?

Powell can simply stop, or reverse, the reduction of more than $400 billion in the Fed’s balance sheet over the past four years to blunt the edge of China’s Treasury sales. Beijing, though, will struggle to sustain growth if capital outflows, which averaged just $34 billion a month this year, surge again to the $68 billion level seen in 2016.

There are ways President Xi Jinping can retaliate against the Trump administration. Cutting off the nose to spite the face isn’t one of them.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andy Mukherjee is a Bloomberg Opinion columnist covering industrial companies and financial services. He previously was a columnist for Reuters Breakingviews. He has also worked for the Straits Times, ET NOW and Bloomberg News.

©2018 Bloomberg L.P.