Why Mario Draghi Should Cut Rates Sooner

(Bloomberg Opinion) -- If Mario Draghi had hoped for a quiet summer before he retires from the European Central Bank in November, his wish hasn’t come true.

The ECB chief will preside over his antepenultimate monetary policy meeting of the Governing Council on Thursday at a disappointing time for the euro-zone economy. Many economists expect the ECB to hold fire until September, perhaps only hinting that more easing is coming soon. But at a time of lackluster growth and weak inflation, the central bank should consider acting immediately rather than waiting for too long.

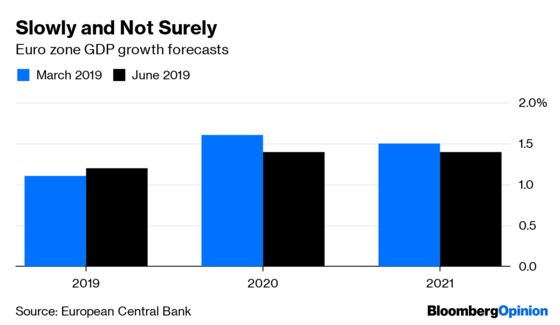

The global economy continues to be a source of bad news for the monetary union. Growth in China dropped to the slowest rate in nearly three decades in the three months through June as trade tensions with the U.S. took a toll on exports. The slowdown in global commerce has severely hurt Germany, which is now expected to grow by a mere 0.5% in 2019 according to the European Commission. Last month, the ECB cut its own forecasts for euro-zone growth in the next two years to 1.4% from 1.6% and 1.5%.

Most importantly for the central bank, there is little sign that inflation will return to the ECB’s target of below but close to 2% any time soon. Prices in the monetary union (excluding volatile items such as energy) were 1.3% higher than a year earlier in June. Inflation expectations, as measured by market participants, are also well below the central bank’s objective. Little wonder Draghi said the ECB stands ready to act unless the situation improves.

Analysts don’t expect policy makers take any significant steps this week, however. The ECB has already moved last month, announcing details of a generous package of cheap loans and telling markets it will keep rates on hold for longer than expected. Draghi also said the central bank is ready to use all its instruments, including restarting asset purchases, a message he reiterated at a later ECB conference in Portugal. Many predict the central bank will perhaps tweak its language a bit, saying rates could also go down, but not much beyond that. Any new package is expected to come in September, when the ECB unveils its latest batch of staff forecasts.

Draghi should consider acting sooner, however. The economy has been weakening since the start of the year, but the central bank has largely preferred to wait and see if the slowdown was real. Meanwhile, other monetary authorities have changed tack: The U.S. Federal Reserve has abandoned plans to raise interest rates further, and could well cut them for the first time in a decade at its next policy meeting planned for the end of July. Last week, two Fed officials stressed the need to act quickly if the economy looks likely to stumble.

The ECB may want to pre-empt the Fed and cut its deposit rates further into negative territory, to -0.5% from -0.4%. This would help to weaken the euro and signal that the ECB isn’t just talk but action.

The argument for waiting longer is two-fold. Benoit Coeure, a member of the executive board, has argued that the ECB should look beyond market-based inflation expectations and take into greater consideration survey-based measures which paint a more encouraging picture. But if the central bank does so, there is a risk it will be seen to be abandoning its preferred indicator when it longer tells the story it wants to hear. Some survey-based metrics are also problematic, since consumers have problems in understanding inflation, let alone predicting it.

The second argument is that the ECB should stay put so as not to run out of ammunition too soon. But this means taking an exceedingly gloomy view of what actions the central bank can take, such as restarting quantitative easing. In fact, if the ECB waits too long, it may need to act more forcefully later if the outlook worsens.

Just months before handing over the ECB presidency, most likely to Christine Lagarde, Draghi is considering innovative steps, including revamping its mandate to give the central bank more leeway to keep inflation elevated for a while after such a long period of weakness. These are useful discussions, but they will likely take time to be put into action. Throughout his term in office, Draghi has shown plenty of resolve to act. A rate cut in July could be the best way to consolidate this legacy.

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Ferdinando Giugliano writes columns on European economics for Bloomberg Opinion. He is also an economics columnist for La Repubblica and was a member of the editorial board of the Financial Times.

©2019 Bloomberg L.P.