Who Wouldn’t Want a Hefty Private Equity Pay Package?

(Bloomberg Opinion) -- The private equity merry-go-round is picking up speed. Buyout firms are weighing up bids for the German classified advertising group Scout24 AG, according to the Financial Times. A deal would return the group to private-equity ownership after three years on the stock market. It’s not cheap. That just goes to show the peculiar attractions of taking a second bite of the leveraged buyout cherry.

Cash has been pouring into private equity funds and flowing out of the public markets. So buyout shops are under pressure to spend. And many listed targets are more affordable than they were at the start of 2018. Moreover, management teams of once closely-held firms are likely to be open to negotiations. Who wouldn’t want to trade the grind of investor roadshows for a lucrative leveraged buyout remuneration package?

Factors like these help explain why CVC Capital Partners is trying to take Ahlsell AB private barely two years after the Swedish building materials group’s initial public offering, and why Esure Group Plc has embraced an offer from Bain Capital five years after going public.

It’s nevertheless a stretch to say that Scout24 is unappreciated by the market. The stock was 24 percent below its 47.66 euros July high at Thursday’s close, yet was still trading at roughly 15 times next year’s estimated Ebitda.

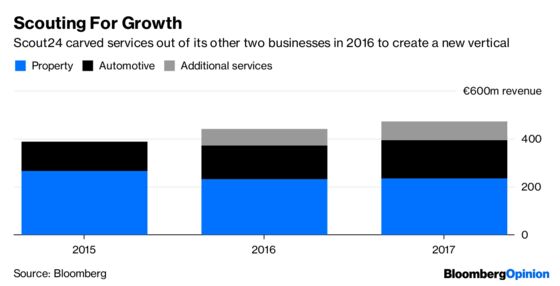

The Munich-based company has been reducing its dependence on property and car listings, mainly by connecting customers directly to mortgage and auto-financing providers. A buyout would capture the opportunity to take this further by adding utilities and car maintenance offerings.

Silver Lake, the tech buyout group that’s reportedly interested, might have an advantage among suitors. Its ownership of U.K. property site ZPG Ltd. and large investment in Red Ventures, a California startup specializing in big-data analytics, provides plausible scope for synergies by improving the rate at which Scout24’s users become customers. It’s easier to get more out of the data scientists you already have than to hire new ones right now.

The obstacle is price. An offer at 48 euros would get all shareholders out with a profit and contain a hard-to-ignore 33 percent takeover premium. The transaction would then cost about 6 billion euros ($6.8 billion) including assumed net debt, or some 18 times prospective Ebitda. That’s punchy, but a bit below the ZPG take-out multiple. The new owners would be lucky to finance this with borrowings of 7 times Ebitda, implying the need to find about 3.7 billion euros of equity, nearly two-thirds of the purchase price.

The relatively low leverage would put more pressure on the company’s management to deliver gains through growth and operational improvements. To make the 20 percent returns sought by private equity would require a doubling of Ebitda or thereabouts and selling at the same high multiple after five years. Not easy.

The alternative would be a break-up. Liberum analysts reckon the group is worth 56 euros a share on a sum-of-the-parts basis, given that media groups such as Axel Springer SE may covet pieces of the business but not the whole.

Scout24 may be loath to support a deal below where the shares traded as recently as July. Still, for private equity, a pricey stock market target may be the best opportunity around right now.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Hughes is a Bloomberg Opinion columnist covering deals. He previously worked for Reuters Breakingviews, as well as the Financial Times and the Independent newspaper.

Alex Webb is a Bloomberg Opinion columnist covering Europe's technology, media and communications industries. He previously covered Apple and other technology companies for Bloomberg News in San Francisco.

©2018 Bloomberg L.P.