(Bloomberg Opinion) -- There’s always been something grimly appropriate about the world’s most unequal rich society being home to one of its least affordable aviation sectors.

Hong Kong’s Cathay Pacific Airways Ltd. has historically been so resistant to the idea of budget airlines that the city’s dominant carrier once fought (and won) a three-year regulatory battle to stop Qantas Airways Ltd. from setting one up in the territory.

That era seems over, with the company saying last week that it was in talks to buy a stake in Hong Kong Express Airways Ltd., the discount carrier owned by cash-strapped HNA Group Co.

It’s a course that we’ve long urged on Cathay’s management. Asked what had prompted the shift after annual results Wednesday, Chairman John Slosar seemed to be paraphrasing a remark attributed to John Maynard Keynes : “You have to be willing to change when events change, when opportunities present themselves,” he told reporters.

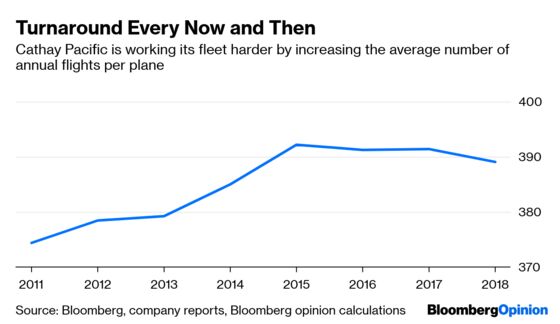

So what facts have changed? For one thing, Cathay’s business model is already looking more and more like that of a budget carrier (perpetually disgruntled passengers often say the same of the flying experience, though this columnist has no complaints). It’s working its fleet harder, with each plane in 2018 carrying out an average of 386 flights, compared with 366 in 2012. That’s still not close to the productivity achieved by the likes of Ryanair Holdings Plc and AirAsia Group Bhd., but it’s heading in the right direction.

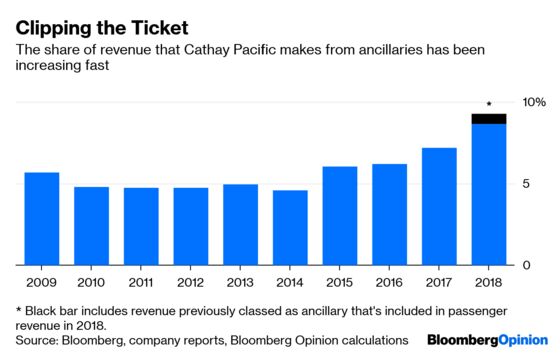

More to the point, the company is making an ever-growing share of its money from selling things other than passenger and cargo tickets, a turn in the direction of the likes of AirAsia, which regularly makes up to 20 percent of its revenue from ancillaries like baggage fees and in-flight meals.

Catering and services revenue came to HK$9.6 billion ($1.2 billion) in 2018, Cathay said Wednesday. That’s about 8.7 percent of revenue, almost double the share four years earlier, and if anything that still understates it. When you include the HK$727 million of ancillaries that was reclassified as passenger revenue for accounting reasons this year, the proportion is more like 9.3 percent.

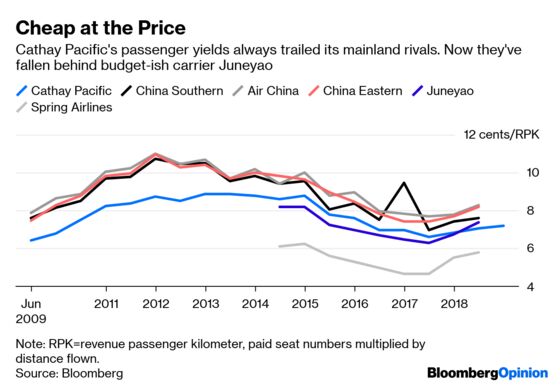

That’s a necessary adjustment, because plane tickets just aren’t worth what they once were. While passenger yields (a measure of revenue per seat, per kilometer) have picked up over the past year, they’ve not escaped the undertow of competition from mainland Chinese carriers. Indeed, since the June half of last year, Cathay’s yields have underperformed even Juneyao Airlines Co., a Shanghai-based operator that tries to straddle the line between budget and full-service airline.

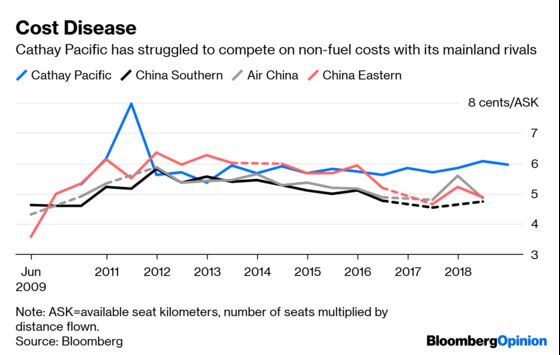

Considering Cathay’s costs are still higher than the competition’s, that’s a problem. Reducing that bill is a lot easier if you start afresh with a new carrier, as Qantas, Singapore Airlines Ltd. and ANA Holdings Inc. found in setting up their own budget divisions.

Cathay Pacific isn’t likely to change overnight. Its cargo operation – the world’s second-biggest at a passenger airline, after Emirates – will still be the main factor underwriting what savings are made in the passenger cabin. But the once-staunch opposition to having a discount arm now seems a relic of an earlier era – along with the pretensions of an airline being a “flag carrier” in the first place, as my colleague Adam Minter has written.

For all that Hong Kong managed to lock out Qantas’s Jetstar, plenty of discount airlines from across Asia are flying to and from Hong Kong’s Chek Lap Kok every day. If Cathay Pacific doesn’t join them, it risks being left behind.

In fact, it seems like Keynes never used the oft-quoted phrase "When the facts change, I change my mind. What do you do, sir?"

Freight operations don't easily mix with discount aviation, since they work best with the ample hold space available in the wide-bodied, twin-aisle planes that budget operators tend not to use.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering commodities, as well as industrial and consumer companies. He has been a reporter for Bloomberg News, Dow Jones, the Wall Street Journal, the Financial Times and the Guardian.

©2019 Bloomberg L.P.