What Africa Needs Now Is Its Own Singapore

Southeast Asia’s sustained enrichment will transform the world, and carry important lessons for struggling countries in Africa.

(Bloomberg Opinion) -- When it comes to economic development, China’s amazing success soaks up much of the attention. But another huge region has quietly begun what looks like a new phase of exponential growth: Southeast Asia. The sustained enrichment of this region will transform the world, and carry important lessons for struggling countries like those in Africa.

Southeast Asia was once almost completely colonized by European powers, and much of it was devastated by a series of wars and internal strife in the mid-20th century. It remains largely poor, with notable exceptions including the wealthy city-state of Singapore, middle-income Thailand and Malaysia, an electronics manufacturing powerhouse that is approaching developed-country status.

The 1970s and 1980s saw very uneven growth throughout the region, and the 1997 Asian Financial Crisis was a brutal, long-lasting setback. In the 2000s, China surged ahead while Southeast Asia seemed like an also-ran.

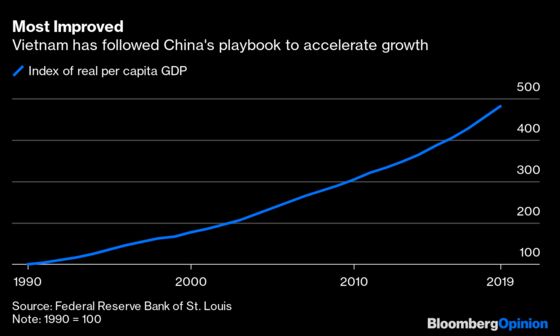

But in the 2010s, growth accelerated all across the region. The standout is Vietnam, whose living standards have now almost quintupled since 1990. It barely stumbled at all after 1997, and has accelerated again in recent years:

Vietnam has gained notoriety for following much of the same playbook as China -- liberalizing its economy, privatizing state-owned enterprises, promoting manufacturing and exports, holding down the value of its currency, and so on. It has benefitted from companies looking to diversify operations out of China, especially during the recent trade war.

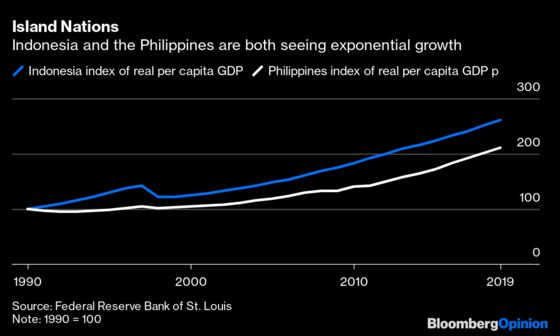

But Vietnam is only the best of a very solid bunch. Indonesia and the Philippines, two archipelagic nations with large populations, now also appear to be entering a phase of explosive growth, with incomes that have doubled since the turn of the century.

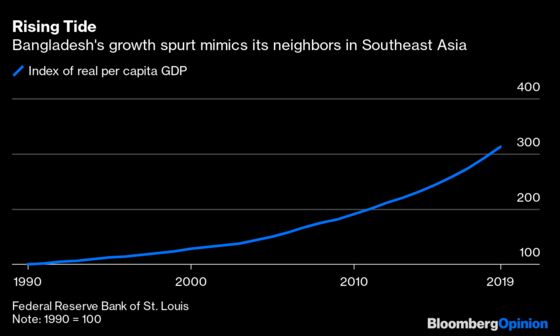

Laos, Cambodia, and Myanmar are growing strongly as well. And another success story is nearby Bangladesh; though typically counted as part of South Asia, it’s enjoying a growth spurt that looks very similar to that of its neighbors to the southeast.

By some measures, Bangladesh is now richer than its giant neighbor India, whose economy has stumbled in the last few years.

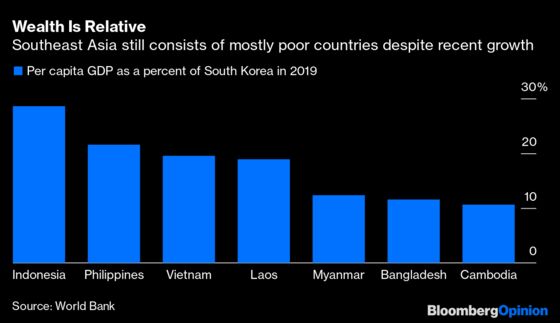

It’s important to remember that all of these are still poor countries. Even after adjusting for local prices, they're nowhere near as rich as a developed country like South Korea.

Even if they can sustain their current robust rates of growth, these countries won’t reach developed-country status until around mid-century. And that will entail other huge challenges, especially environmental ones; in addition to rising carbon emissions, Southeast Asia is already a major source of oceanic plastic waste.

Still, an entire region growing like gangbusters is an incredible accomplishment, and demonstrates the success of decolonization and globalization. That leads to the next big question: How did they do it?

The simple answer is that Southeast Asian countries are developing in much the same way other countries did decades or centuries earlier -- by making stuff. The basic pattern is now well-known. First a country shifts people from farms to cities, in order to make cheap items like clothing, toys, furniture and fabric. Then it moves up the value chain to electronics, auto parts and so on.

Indonesia, whose industrialization stalled after the Asian financial crisis in the late 1990s, is the exception, though it still does a fair amount of manufacturing.

But that simple answer is unsatisfying. Which policies allowed these countries to jump into the global manufacturing chain? Someday, economic historians might offer in-depth studies that reveal that all the Southeast Asian countries enacted very similar measures all at once. Or maybe they were all just in the right place at the right time.

As China’s wages and other costs have soared, multinational companies have gone looking for newer, cheaper sources of manufactured goods. Southeast Asian countries had cheap wages and were located near China, requiring minimal geographic relocation of shipping routes and personnel. Rich countries like Japan, Taiwan and South Korea already had strong ties to many of these countries, and could act as both sources of investment and markets for Southeast Asian goods. Like the proverbial flock of geese, manufacturers and retailers simply moved to where it made sense to move. This also fits with the theory of economic agglomeration, which suggests that regions develop one by one instead of all at the same time. As Asia has become the economic center of the world, the entire region has eventually reaped the benefits.

And that’s a frustrating thing for Africa to hear. Located far from booming Asia, Africa may have to wait its turn to be the next manufacturing hotspot. And there are no industrialized rich nations in Africa to help kickstart its development -- no equivalent of Japan or Singapore. That’s not to say no manufacturing will be done in Africa; investment there is growing, especially from China. But it’s still a trickle instead of a flood.

What Africa might need is its own Japan -- a pioneering country that can industrialize first, and then invest in the rest of the continent. That country might be Ghana, which has strong institutions, political stability, and good education and literacy. While Africa might have to wait a while to follow in Southeast Asia’s footsteps, that shouldn’t prevent individual African countries from trying hard to industrialize on their own.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Noah Smith is a Bloomberg Opinion columnist. He was an assistant professor of finance at Stony Brook University, and he blogs at Noahpinion.

©2020 Bloomberg L.P.