WeWork and SoftBank Need Each Other

(Bloomberg Opinion) -- Billionaire Masayoshi Son seems ready to bet big on a majority stake in WeWork, the $20 billion shared-office-space provider that masquerades as a “physical social network.”

This makes sense. WeWork needs cash to fund its breakneck growth; Son and his SoftBank investment fund need fast-growing startups to generate returns on their cash pile. Whether the next five years will prove them right is another matter entirely.

The idea of SoftBank pouring more money into WeWork at a valuation of $35 billion just a year after it invested at a $20 billion valuation will no doubt bring to mind the image of a bubble.

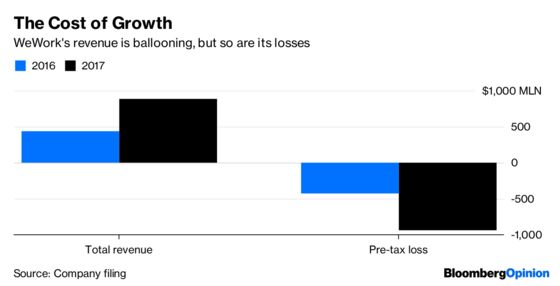

WeWork posted a pretax loss of $939 million in 2017 after a $430 million loss in 2016. Its move to raise financing from the bond market this year didn’t go smoothly. The company’s fondness for metrics like “community-adjusted Ebitda” — unique in the world of regular commercial real estate — was mocked. Why would SoftBank ignore these red flags, and even re-invest at a higher price?

While WeWork’s delusions of grandeur deserve criticism, it’s unfair to say that these valuations are completely off-the-wall.

Revenue growth is the key factor: Sales doubled last year to $886 million and, according to a memo to employees seen by Reuters, growth looks set to exceed that this year. WeWork’s properties are centrally located, its trendy decor and drinks on tap appear to pull in punters, and it enjoys a strong brand. It is now London’s biggest office tenant, according to Bloomberg.

The $20 billion valuation begins to make some sense if you assume WeWork continues to grow at the same clip — which is a big if.

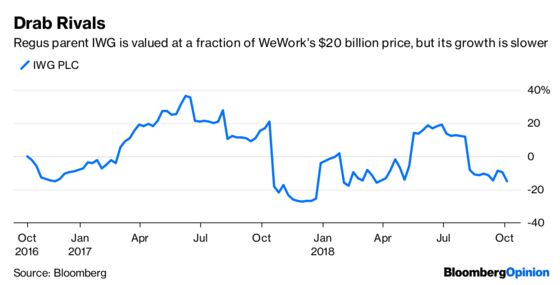

WeWork’s valuation certainly looks stratospheric when compared with IWG Plc, owner of the rather more drab Regus chain of serviced offices. That’s valued at 2 billion pounds ($2.6 billion), or a mere 0.9 times last year’s sales. But it’s a mature business whose annual revenue growth trails that of WeWork.

If you assume that WeWork’s revenue growth can slow down without falling off a cliff over the next five years — from 100 percent annually to, say, 50 percent — that would theoretically lead to revenue of about $13 billion. A price tag of $20 billion would be about 1.5 times that future figure, bringing it much closer to IWG’s forward revenue multiple.

Obviously, WeWork is unlikely to realistically get to $13 billion in sales as a pure office-space provider — the top five U.S. office real-estate developers collectively make only $7 billion in sales between them, according to Bloomberg data. To keep growing at its current rate, WeWork would have to squeeze more money out of the services it offers tenants and employers as well as monetize the value of the data it collects about its hipster inhabitants.

The bigger hitch is the cost of WeWork’s rapid expansion in a cyclical and leveraged industry like property. Making offices cozy costs money: between 2016 and 2017 WeWork’s expenses more than doubled to $1.8 billion from $832 million. It is paying top-of-the-cycle prices for real estate: As of April 2018, it had committed to pay at least $18 billion in rent for its 14 million square feet of space. And with many competitors on the horizon, under-cutting or out-spending them requires cash.

This is surely music to the ears of SoftBank. Son aims to raise a new $100 billion fund every two to three years, and invest about $50 billion each year. Only the biggest bets with the highest risk-reward profile are going to fit the bill.

If the WeWork deal goes ahead using SoftBank’s Vision Fund (which has stakes in Uber and U.K. chip-maker ARM Holdings) it would be the fund’s biggest single investment. Their fates would be intertwined — appropriately so, given their growth ambitions.

If breakneck growth fails to materialize, or if the funding spigots are turned off by an economic crisis, both WeWork and SoftBank would have a nasty wake-up call. At least Son would have more office space to himself.

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Lionel Laurent is a Bloomberg Opinion columnist covering finance and markets. He previously worked at Reuters and Forbes.

Alex Webb is a Bloomberg Opinion columnist covering Europe's technology, media and communications industries. He previously covered Apple and other technology companies for Bloomberg News in San Francisco.

©2018 Bloomberg L.P.