Vodafone's $4.5 Billion Happy Meal for Hedge Funds

(Bloomberg Opinion) -- Vodafone Group Plc’s new boss needed some luck. The financing markets appear to be favoring Nick Read as the U.K. mobile phone giant prepares to splash out on buying a huge chunk of John Malone’s European cable empire.

On Tuesday, Read unveiled a 4 billion-euro ($4.5 billion) financing package for the purchase, which should help the company create a converged mobile, broadband and television empire across Europe.

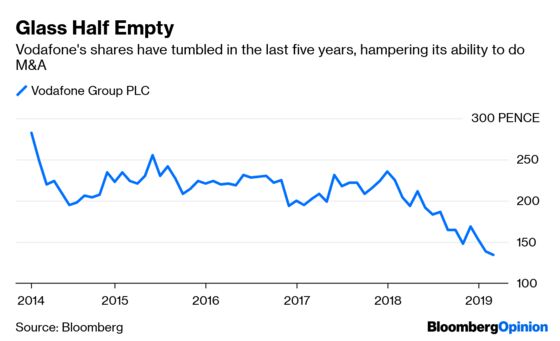

The snag is that Vodafone’s financial health is already weak: The shares are trading at levels last seen in 2010, so a big share sale is impossible. Net debt is 30 billion euros, against a market capitalization of 37 billion pounds ($49 billion). Heaping on more borrowings would strain the credit rating.

The markets are offering Vodafone a magic solution: bonds that will be repaid in stock instead of cash a few years’ time. Because they aren’t really debt, they won’t damage Vodafone’s credit metrics. The also let Read spare his shareholders the immediate dilution of a mega share sale at a knock-down price.

Indeed, Vodafone is trying to spare investors this pain entirely. It plans to buy back the new shares it will have to issue to settle the bonds when the securities mature in 2021 and 2022. The company expects to fund the purchase by raising debt nearer the time – by which point its finances should be healthier.

The risk is that Vodafone’s share price shoots up in the intervening period, making the buyback painfully expensive. So Read is using derivatives to hedge that risk and so cap the cost.

The net effect of all this is that Vodafone rents some equity for a few years and then raises debt when it’s in better shape.

This corporate finance magic doesn’t come for free – but it's hardly hostage pricing.

The two sets of bonds are being marketed with coupons of roughly 1.6 percent and 1.9 percent, and strong demand could see them price even lower. (By comparison, Vodafone pays less than 0.5 percent to borrow for the same period in the European bond market.)

These mandatory bonds usually offer much higher premiums. That's because investors typically get lower capital gains than they would from simply buying the shares, and a higher yield is needed to compensate for that. Here, Vodafone is opting for a structure that gives investors all the upside if the shares skyrocket simply to reduce the costs for itself.

The lowish yield should still be attractive to hedge funds who will gobble it up and fund their purchases of the bonds by selling Vodafone shares short. That latter position gets covered with the stock issued in settlement at maturity. Nice work if you can get it – no wonder the package is known as the happy meal for hedgies.

The black box is the price-capped share buyback that Vodafone is setting up to prevent the dilution that would normally happen when these mandatory bonds convert into new stock. The cost of this needs to be added to the yield premium on the bond.

The investment banks arranging the transaction are ready to help with that hedge. In the first instance they mopping up roughly half of the bonds. Given the amount of activity this generates with their clients, the lenders may be willing to provide the hedge themselves at a cheaper price than in the options market.

It’s clever and facilitates the Malone deal, an acquisition that will diversify Vodafone’s business, boost cash flow and allow for cost cuts. But Read is pulling every lever. He would surely prefer to have funded the deal with equity. If he is ever to do that, he will need to boost the stock price.

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Hughes is a Bloomberg Opinion columnist covering deals. He previously worked for Reuters Breakingviews, as well as the Financial Times and the Independent newspaper.

©2019 Bloomberg L.P.