(Bloomberg Opinion) -- Judging from Valero Energy Corp.’s latest results, oil refiners have it pretty good right now. So it might be worth not judging solely from those results.

To say Valero exceeded earnings forecasts would be an understatement; the figure for the fourth quarter came in at almost double the consensus estimate, the company’s biggest beat since early 2011, according to data compiled by Bloomberg. Tumbling crude oil prices — an input cost for refiners — pushed average margins-per-barrel way above expectations.

So much for the fourth quarter. Things look less rosy right now. That’s partly the usual new-year blues hitting refiners. But some things have clearly changed. Oil prices have stabilized as OPEC+ cuts kick in, Venezuela’s situation worsens and Iranian sanctions re-emerge as a threat to supply. The new U.S. sanctions on Venezuela compound this, by removing a big slug of cheaper, heavy barrels from U.S. Gulf Coast refineries, Valero’s included. It’s notable that the discount on Canada’s heavy oil relative to West Texas Intermediate has tightened to less than $10 a barrel, from almost $50 in late October, and Albertan authorities are easing production caps there more quickly than expected.

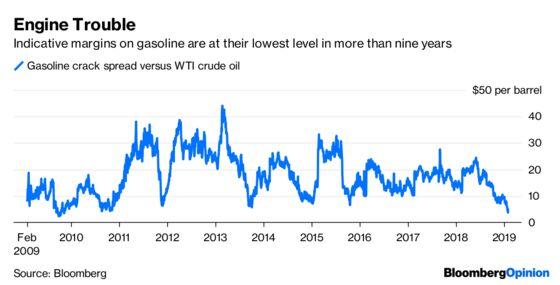

Perhaps the biggest concern, and one which featured prominently on Valero’s earnings call Thursday morning, pertains to gasoline. Refining margins for this fuel are extraordinarily weak. After crawling back above $5 a barrel on Wednesday on the back of official U.S. data showing a surprise drop in inventories, the gasoline crack-spread versus WTI slipped below $4 Thursday.

The Midwest’s current brush with Plutonian temperatures is temporarily piling on pressure (people drive less when they can’t feel their own hands). But the bigger issue is that there’s a glut of gasoline that last week’s draw on inventory only just began to address. Refiners have been running flat out as they chase healthy margins on distillate fuel, which includes diesel and heating oil (these markets, incidentally, love the cold). Refining a barrel of WTI into diesel yields a simple margin of more than $25 a barrel.

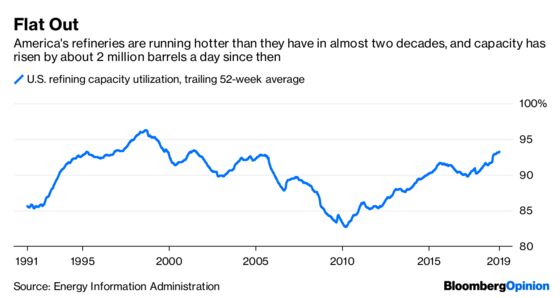

On a trailing 52-week basis, the U.S. refining system has been running at more than 93 percent of capacity, the highest since the summer of 2001. Moreover, as capacity has expanded considerably since then, actual throughput is the highest it’s ever been in official data going back to 1990, averaging 17.3 million barrels a day over the past year.

As I wrote here, the combination of strong refining runs and a lightening slate of crude oil (due to rising shale output) means more gasoline is being churned out as a byproduct of companies chasing those distillate margins. Sanctions on Venezuela potentially exacerbate this, by pushing refiners to replace heavy barrels with lighter ones (see this). Valero indicated it could take perhaps another 100,000-150,000 barrels a day of light crude oil.

Ultimately, demand will have to take up the slack if margins on gasoline are to be restored. Valero was hopeful about this on Thursday’s call, citing low prices and low unemployment helping in the U.S. and strong exports. The latter have been increasing in recent years, but also face rising competition from new facilities in China geared toward producing lighter fuels (gasoline included), as well as European refiners who are finding their traditional foreign markets (the U.S. and China, for example) already well-supplied.

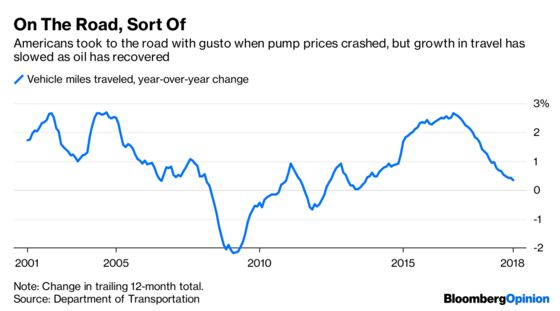

On the domestic front, Valero is right about favorable pricing and the economy. And America’s love affair with thirstier trucks and SUVs continues. Even so, these factors appear to be stabilizing rather than increasing gasoline demand. After big gains in 2015 and 2016 when the oil crash kept pump prices exceptionally low, trailing 52-week consumption now bobs around the level of 9.3 – 9.4 million barrels a day. Similarly, growth in vehicle-miles traveled, while still positive, has slowed:

As long as diesel margins remain high — and there’s little reason to see them falling, given low inventories — then refiners can live with weakness in gasoline. Valero, in particular, has demonstrated its ability to capture opportunities on margins where it can find them, and pay out any windfalls to shareholders. Conversely, such financial strength means gasoline supply could stay strong as the year progresses. There must be some hope on Valero’s part that the less-favorable environment for crude oil price-spreads pushes some of its rivals to rein themselves in.

Absent that, and if demand doesn’t rise to absorb those extra gallons, then gasoline will remain a persistent topic of concern, and conversation, on those quarterly calls.

To contact the editor responsible for this story: Mark Gongloff at mgongloff1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2019 Bloomberg L.P.