Unilever CEO Misreads his Shareholders, to Their Cost

The consumer giant needs to find another way to simplify its structure if it’s to embark on a big deal.

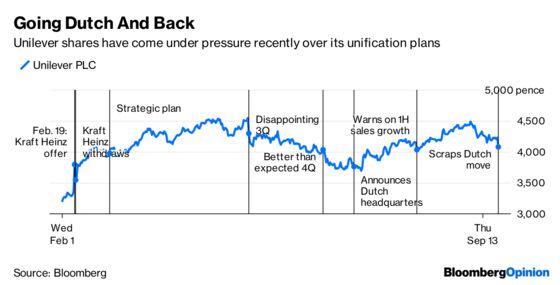

(Bloomberg Opinion) -- Paul Polman's parting gift to his successor as CEO of Unilever has been smashed by his U.K. shareholders.

On Friday, the Anglo-Dutch consumer goods group scrapped its plan to simplify into a single company in the Netherlands. There is immediate damage in terms of management credibility, and a potential long-term opportunity cost.

The proposal would have seen the current U.K. arm of Unilever being bought out by a new Dutch entity. The move would have hurt funds whose mandates limit them to investing only in U.K. or FTSE-100 stocks. They would have to sell, or drift from their terms of reference, to hold shares in the new all-Dutch Unilever. It was in their interest to vote down the plan.

Unilever's other U.K. shareholders aren't so encumbered. But they faced tax uncertainties, and trading the new London-listed Dutch share may have come with additional friction.

Some individual investors may have been offended by the impression that Unilever was trying to quit Britain after Brexit.

The naysayers had influence: The plan needed to be approved by a simple majority of Unilever Plc shareholders by number, with at least 75 percent of the U.K. shares being voted in favor.

Polman clearly misread the situation. He should have at least offered the U.K. shareholders a premium, or a special dividend.

Instead, Unilever's ethics were crudely utilitarian. Its attitude was that while a minority was being disadvantaged, their sacrifice was worth it for the good of the majority. If a premium was due in theory, it wasn't necessary in practice. That was wrong and tactically flawed.

Options always have value, and Unilever's plan would have given it more M&A options that would benefit shareholders.

The company will still find it tricky to do really big corporate moves. It may be at a competitive disadvantage in bid situations. Some M&A experts reckon its joint-venture structure exposes shareholders of potential U.S. targets to taxes they wouldn't otherwise pay.

The interconnected nature of Unilever's current British and Dutch companies means a de-merger of its food business – as often speculated – wouldn't be easy. Coupling that with a transformational deal, like buying Estee Lauder Cos or Colgate-Palmolive Co., to become a dominant personal care business would be tough.

Could Unilever come back with a reworked plan? To propose collapsing its structure into an all-U.K. company would just create a political row in the Netherlands that would match the shareholder row on the British side. Euro-zone funds would be similarly disadvantaged.

The Royal Dutch Shell Plc structure – U.K. company with Dutch tax domicile – looks like the only viable alternative. Sure, the oil company has two classes of shares so that U.K. shareholders can receive payouts exempt of Dutch dividend tax. But the Netherlands is due to scrap the levy by 2020, so it might be possible to copy Shell without re-creating another dual-class structure.

This is hardly the swan song Polman wanted. He has stayed away from all the communications around the plan – but it is his legacy that is tarnished. He could just leave the question of Unilever’s structure to his successor. But the company has made such a song and dance about the benefits of simplification that it owes it to shareholders to come back with a new proposal that even the recalcitrant minority can accept.

--With assistance from Andrea Felsted.

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Hughes is a Bloomberg Opinion columnist covering deals. He previously worked for Reuters Breakingviews, as well as the Financial Times and the Independent newspaper.

©2018 Bloomberg L.P.