Unicorns Backing Their Own VCs? Welcome to Peak Tech

(Bloomberg Opinion) -- When unicorns start setting up their own venture-capital funds, you know the tech world is getting frothy.

In June, Singapore-based ride-hailing app GrabTaxi Holdings Pte launched Grab Ventures, shortly after its Indonesian rival Go-Jek Indonesia PT set up its own Go-Ventures. Onetime unicorn Meituan Dianping — the Chinese food-delivery firm that just completed its $4.2 billion IPO in Hong Kong — raised a $302 million fund in July for its DragonBall Capital fund.

What are unicorns doing in the venture-capital world when they still need plenty of their own financing? Just in the past few months, Grab has raised $2 billion to double down on its expansion into Indonesia and Go-Jek is close to adding another $1.5 billion to its war chest. As for Meituan, its loss-making service helped burn through $1.2 billion for the year ending June.

Blame liquidity.

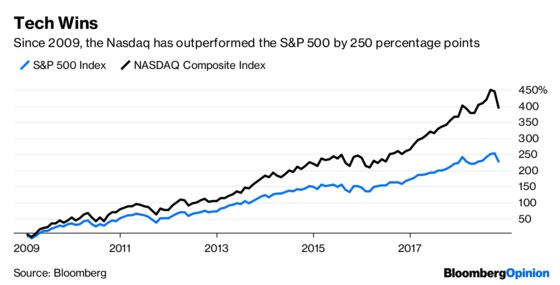

These days, even private equity funds, fearful of missing out, have emerged in the venture world. KKR & Co. is co-investing with SoftBank Group Corp. in Beijing Bytedance Technology Co., a deal that would value the parent of news aggregator Toutiao and video sensation Tik Tok at $75 billion. If there’s one lesson from the past decade it’s that tech investors win: Since 2009, the Nasdaq Composite Index outperformed the S&P 500 Index by 250 percentage points.

These generous checks are pushing back IPO timelines — and as they mature, unicorns are being forced to buy growth.

For young startups, having Meituan or Grab as an early investor is a prestigious talking point. But it doesn’t mean these stakes come cheap — in China, at least.

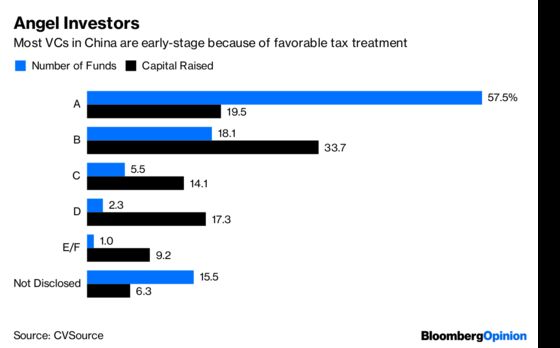

As liquidity in China’s private-funds industry starts to dry up, there are still plenty of angel investors out there. To encourage innovation, the Ministry of Finance stipulated in May that early-stage venture-capital firms can deduct up to 70 percent of their investment for future capital-gains taxes. As a result, more than 50 percent of VCs in China are A- and pre-A rounds, and these funds account for almost 20 percent of capital raised.

In the past, strategic buyers like Tencent Holdings Ltd. and Alibaba Group Holding Ltd. were often aggressive, wanting 30 percent to 40 percent ownership. That pressured young startups to cede control of business decisions, even forcing them to fight for market share at the expense of profitability. If unicorns take a page out of the blue chips’ playbooks, they better pay up.

“We do not want strategic buyers to come in too early,” said Yipin Ng of Yunqi Partners, an early-stage venture capital fund, at the 31st Annual AVCJ Private Equity & Venture Forum in Hong Kong this week.

There’s a note of caution in all this. Despite its glamorous $100 billion Vision Fund, SoftBank — loaded up with a tangle of investment arms and non-core businesses — famously suffers from a deep conglomerate discount. So when (if?) the world’s most-valued unicorns go public, they risk coming across as a bit bloated, too.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shuli Ren is a Bloomberg Opinion columnist covering Asian markets. She previously wrote on markets for Barron's, following a career as an investment banker, and is a CFA charterholder.

©2018 Bloomberg L.P.