(Bloomberg Opinion) -- Risk and return go together, as any good investment manager will tell you. That’s the dilemma facing overseas private bankers serving China: Household wealth of $29 trillion presents an unmissable opportunity, but the hazards of tapping it may also be unusually high.

Banks including Julius Baer Group Ltd. and Citigroup Inc. have told relationship managers to delay or reconsider travel to China after a UBS AG employee was asked by authorities to remain in the country to answer questions about an unspecified matter, according to reports by Bloomberg News and other news outlets since Friday. UBS itself removed travel restrictions on its private bankers, a spokesman said Tuesday.

The circumstances surrounding the Singapore-based UBS banker’s situation are unclear. Still, the cautious response of other global wealth managers highlights the tension of overseas-based staff operating in a country that maintains capital controls and where an expanding pool of ultra-rich clients is frequently anxious to move money offshore.

China’s wealth has risen 1,300 percent this century, more than double the rate of any other nation, Credit Suisse Group AG said last week. UBS estimates a new billionaire is minted in China every two days.

At the same time, China’s economic growth has been slowing, stocks have slid into a bear market, real estate prices are cooling and the yuan has weakened — all giving investors more of an incentive to shift wealth offshore. The prospect of capital outflows fueling further weakness has, in turn, prompted authorities to tighten restrictions. Rules restrict individuals to taking out $50,000 out of China per year.

Private bankers are in a tricky spot. Often, they already manage offshore assets for China-based clients. In an industry where relationships are paramount, visiting such clients on their home turf may be deemed necessary.

Rule No. 1 among foreign wealth managers with licenses in Hong Kong and Singapore is that offshore private bankers can meet with clients onshore but not solicit business from them. They can probably pick up documentation, for instance, though signing a contract wouldn’t be allowed.

That’s a lesson Crown Resorts Ltd. learned the hard way two years ago when 18 of its staff in China were detained for encouraging clients to visit its casino in Australia.

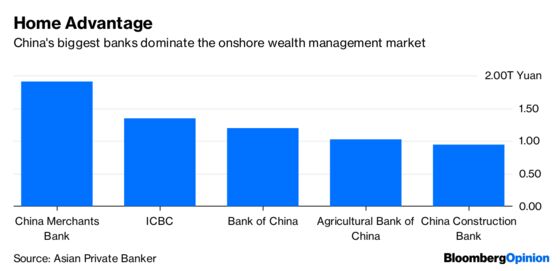

The easy answer is to stay home. Beyond avoiding red tape or legal jeopardy, there’s far less competition from the large Chinese banks that dominate the onshore private-banking industry. In China, these institutions can offer the kind of wealth management products that Western firms’ compliance departments wouldn’t approve.

Asia’s offshore hubs are far from a small market. Hong Kong’s offshore wealth has been rising 11 percent annually and reached $1.1 trillion last year, according to Boston Consulting Group. Growth in Singapore has been running at 10 percent. That compares with 3 percent in Switzerland, which remains the world’s biggest offshore wealth market.

For all the swelling ranks of China’s super-rich, UBS is preparing to diversify by putting ultra-high-net-worth Americans at the center of its growth strategy, almost a decade after it was fined by the U.S. for helping thousands of clients evade taxes, the Financial Times reported Monday.

All the same, China may remain too lucrative a prize to ignore. Private bankers that operate there will continue to walk a fine line. They should tread carefully.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Nisha Gopalan is a Bloomberg Opinion columnist covering deals and banking. She previously worked for the Wall Street Journal and Dow Jones as an editor and a reporter.

©2018 Bloomberg L.P.