(Bloomberg Opinion) -- Uber Technologies Inc.’s initial public offering next week will be a bittersweet moment for private equity giant Carlyle Group and its London minicab firm Addison Lee Holdings Ltd.

Uber will almost certainly join its fellow ride-hailing company Lyft Inc. in securing a nosebleed market value, despite making heavy losses. The investor buzz could benefit Carlyle as it looks to exit from its own unprofitable taxi operator. Unfortunately, fierce competition from Uber is also a big reason why Addison Lee has been such a difficult investment for Carlyle’s 5.4 billion euro ($6 billion) European buyout fund.

Media reports suggest that the U.S. private equity firm hopes to sell Addison Lee for between 300 million pounds and 500 million pounds ($390 million to $650 million, though estimates vary widely) and that Jaguar Land Rover Automotive Plc, the luxury British carmaker, might be among the interested parties.

However, Carlyle’s previous attempts to sell Addison Lee came to naught, and it’s not certain whether recent efforts to strengthen the business by expanding internationally will deliver sustainable profit growth. Legal questions about Addison Lee’s employment of casual drivers are unresolved. When potential bidders look under the hood, they may not like what they find. Addison Lee’s revenues have grown, but so have its losses.

Carlyle bought Addison Lee in 2013 for about 300 million pounds, including debt, but it was a poor moment to acquire a fleet of more than 4,500 London minicabs just as Uber had launched in in the city.

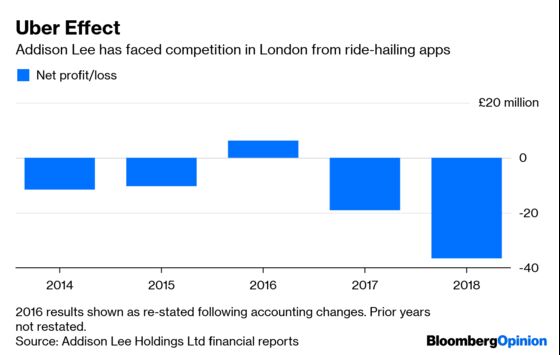

Addison Lee’s latest accounts show the scars from Uber’s arrival remain unhealed. Net losses almost doubled to 37 million pounds in the 12 months to August 2018. While that was due partly to one-off restructuring costs, this was hardly the first time the company has lost money under Carlyle’s ownership.

Wisely, Addison Lee responded to Uber by investing heavily in technology and a premium car service (unlike Uber, it rents many of its cars to drivers), but that has taken its toll on the balance sheet. Liabilities due in the next 12 months far exceed current assets and shareholder funds are negative, usually not a good sign. Net borrowings, excluding preference shares and finance leases, are about five times adjusted earnings by my calculation.

In fairness, Addison Lee does at least have positive Ebitda, unlike Uber. But thanks in part to those hefty investments and rising overhead costs, its cash had dwindled to just 8 million pounds at the end of August. The company initially pursued a comprehensive refinancing of its debts, but opted eventually to extend repayment terms on some of them. It also received additional loans of 30.5 million pounds from related parties, presumably Carlyle, to fund its working capital requirements.

Of course, losses have been no barrier to Uber amassing billions of dollars of venture capital, nor to the company seeking a stock market value that’s an eye-watering seven times its yearly revenue.

Addison Lee’s nascent driverless car project and various U.S. acquisitions seem designed to help it benefit from the Uber halo effect and to re-position a plain-vanilla taxi fleet operator as a growth company. Revenue has jumped by almost half since 2016 to near 400 million pounds and the U.S. now accounts for about one-quarter of those sales.

Corporate clients provide about three-quarters of the car service’s revenue, offering some protection from Uber’s price war in consumer ride-hailing. Potential buyers may worry, though, about Addison Lee’s still predominantly British business, especially given the recent pushback against gig economy employment practices by the country’s judges.

Along with Uber, Addison Lee has faced legal challenges over its classification of drivers and couriers as self-employed contractors. If its appeals are unsuccessful, the company might have to offer worker benefits such as holiday pay, inflating its operating costs.

Addison Lee was a relatively small investment for Carlyle, which has put about 125 million pounds of equity and debt into the company and shouldn’t have trouble recouping at least some of that. Yet one wonders why a loss-making carmaker like Jaguar Land Rover would want to add a minicab firm’s challenges to its own.

The risk section of Uber’s IPO prospectus says plenty about the difficulties of making money from selling car rides. Addison Lee could no doubt tell you the same.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Bryant is a Bloomberg Opinion columnist covering industrial companies. He previously worked for the Financial Times.

©2019 Bloomberg L.P.