Uber Is Too Mature and Immature

It has the hallmarks of a slowing, established company and the unprofitable economics of an upstart.

(Bloomberg Opinion) -- Uber Technologies Inc. and Lyft Inc. are both infants as public companies. And they're already showing signs of middle age.

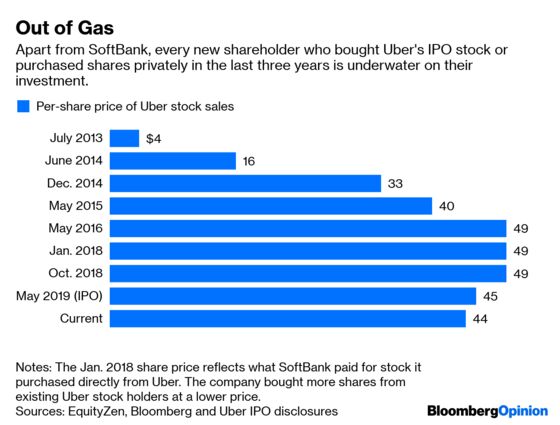

On Friday, Uber started selling its shares widely for the first time, and it wasn't a great start. Uber sold an initial batch of $8.1 billion in stock to the public on Thursday at $45 each, which was lower than the price paid over the last three years of stock sales to private investors such as Saudi Arabia's government investment fund. Uber's share price as of this writing was lower still than the IPO price.

Uber has sold $17 billion in stock since December 2015, according to its IPO documents, including the shares sold in Thursday’s offering. Each new stock buyer in that time – apart from SoftBank Group Corp. – is now staring at a loss on their investment. Ouch.

If Uber and Lyft, whose stock price has fallen more than 25% from its late March IPO, continue to trade down in coming months, it underscores doubts about the viability of facilitating the transportation of people and goods with ersatz workers. It’s also not great for other richly valued tech companies seeking to tap the public market this year.

All of them will find that going public comes with tough questions. The common one for Uber and Lyft is, will they ever turn a profit? But my pressing question is, how much bigger will they ever get?

Uber recently forecast that the total value of vehicle rides on its service in the first quarter may have declined slightly from three months earlier. The average monthly number of "trips" per Uber customer – that may be a ride in an Uber car, an Uber bicycle rental or an Uber Eats food order – has stayed relatively flat for more than a year, even as Uber expands its newer offerings such as Uber Eats and rentals of bikes and scooters. To be fair, the number of people using one of Uber's services has continued to increase, including at a rate of 33% in the first quarter from a year earlier.

But Uber's revenue from vehicle fares after its drivers are paid only increased about 9% in the first quarter from the same period in 2018, based on the midpoint of the company’s forecast. The growth from the prior quarter was 1.5%. That's not great, and Uber isn’t alone.

Lyft recently told investors to expect its net revenue – what the company keeps after subtracting the pay to drivers – would increase by 52% this year from 2018, based on the midpoint of the company's forecast. That's an impressive growth rate until you realize Lyft's revenue more than doubled in 2018 from the prior year.

Optimists point to the enormous potential of Uber and Lyft, which have created genuinely useful ways to move people and goods in the physical world and account for a tiny fraction of all vehicle trips in their world. If the size of the opportunity is so vast, why aren't Uber and Lyft growing faster?

It’s true that Lyft and particularly Uber – which recorded $50 billion worth of vehicle fares, restaurant orders and other transactions last year – can’t grow like a weed forever. But investors buying shares of a company that generated an operating loss of $3 billion last year, as Uber did, surely expect heady growth.

This all means that Lyft and Uber will need to find fresh sources of growth and demand. Uber is stressing its Uber Eats business, which is expanding fast, and barely talking about the rides business that generates 80% of its revenue. Both Lyft and Uber are trying to get more people onto scooters and bicycles, which may have better economics for the companies and bring down the cost of a trip to potentially get more people using their services regularly. Uber and Lyft are trying, too, to expand transportation services into cities or countries where they haven’t operated for financial or regulatory reasons.

None of this is easy, and the stakes are particularly high for Uber given its $75 billion stock market value. At the moment, the combination of the hallmarks of slowing, mature companies and the unprofitable economics of youngster companies make Uber and Lyft hard for investors to love.

Those investors purchased preferred stock,which tend to come with more rights than common stock. But all the preferred shares converted into common shares at the IPO on a one-to-one basis.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shira Ovide is a Bloomberg Opinion columnist covering technology. She previously was a reporter for the Wall Street Journal.

©2019 Bloomberg L.P.